The One Big Beautiful Bill Act (OBBBA), formally signed into law in July 2025, represents the most substantial legislative overhaul of federal tax policy since the landmark 2017 Tax Cuts and Jobs Act (TCJA). This comprehensive legislation introduces a multifaceted array of changes designed to reshape the American tax landscape for individuals and businesses alike, with profound economic ramifications extending through the next decade.

In February, the Tax Foundation released an updated modeling analysis of the OBBBA, incorporating revised economic estimates and refined guidance regarding the senior deduction phaseout. These adjustments collectively led to an increase in the average national tax cut by $60.61 for 2026. Concurrently, state-level full-time equivalent (FTE) jobs numbers presented in the accompanying data were revised to align with the latest economic projections, offering an even more precise understanding of the Act’s expected influence.

A Sweeping Overhaul: Key Provisions of the OBBBA

The OBBBA’s core tenets are built upon and expand significantly from the foundation laid by the TCJA. A pivotal aspect of the new law is the permanent establishment of the individual tax changes originally introduced by the TCJA. This crucial move averts an anticipated tax increase for an estimated 62 percent of tax filers that would have occurred in 2026 had the TCJA provisions been allowed to expire. This permanence provides much-needed stability and predictability for millions of American households.

Beyond these extensions, the OBBBA introduces a suite of additional tax reductions for both individuals and businesses. For individuals, these include novel deductions for tipped income and overtime income, aiming to provide relief to specific segments of the workforce. The Act also features an expanded Child Tax Credit (CTC), a measure designed to bolster financial support for families, and an enlarged standard deduction, which reduces a taxpayer’s taxable income by a set amount determined by the government, offering an alternative to itemizing deductions.

On the business front, the OBBBA makes permanent several key provisions that were previously temporary. This includes 100 percent bonus depreciation, which allows businesses to immediately deduct the full cost of certain qualified investments, rather than depreciating them over time. This incentivizes capital expenditure and modernization. Furthermore, the Act ensures the permanence of domestic research and development (R&D) expensing, allowing companies to deduct R&D costs in the year they are incurred, fostering innovation and competitiveness.

The Genesis of the OBBBA: A Legislative Chronology

The journey to the OBBBA’s enactment was shaped by years of evolving tax policy and political dynamics. The 2017 TCJA, championed by the previous administration, marked a significant shift in tax philosophy, emphasizing lower corporate and individual rates, alongside various deductions and incentives. However, many of its individual provisions were set with expiration dates, primarily at the end of 2025, creating a fiscal cliff that threatened to raise taxes for a substantial portion of the population.

As these expiration dates loomed, a renewed legislative effort gained momentum to address the impending changes. Proponents argued that allowing the TCJA’s individual tax cuts to lapse would undermine economic stability, increase the tax burden on middle-class families, and create uncertainty for businesses. The debate surrounding these expiring provisions became a central theme in fiscal policy discussions leading up to the 2024 elections and into 2025.

The "One Big Beautiful Bill Act" emerged from these discussions, crafted as a comprehensive package to not only make permanent the popular individual tax cuts but also to introduce new incentives and deductions. The Act’s title itself, evocative of a political rallying cry, signaled an ambitious legislative agenda. After months of deliberation, negotiation, and amendments, the OBBBA was successfully shepherded through Congress and signed into law in July 2025. Its provisions began to take effect, with many of the critical individual tax changes preventing scheduled increases from 2026 onward, while business tax cuts, previously set to diminish, were cemented. The Act’s structured phase-ins and phase-outs, such as the evolution of the State and Local Tax (SALT) deduction cap and the temporary nature of certain new deductions like those for tips and overtime, reflect the compromises and long-term fiscal planning embedded within the legislation.

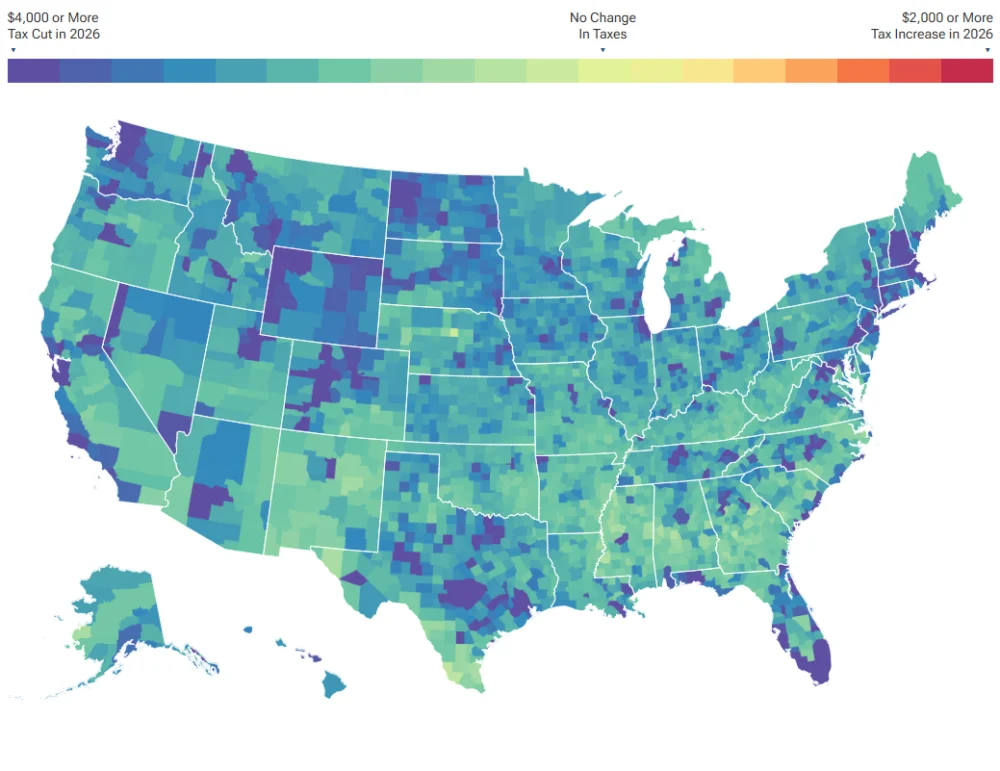

Geographic Variation in Tax Benefits: A Detailed Look

To illustrate the intricate impact of the OBBBA, the Tax Foundation meticulously estimated the average change in taxes paid per individual taxpayer across every state and county, covering the period from 2026 through 2035. This analysis starkly reveals the considerable geographic disparities in the tax benefits derived from the OBBBA, particularly when juxtaposed against a hypothetical scenario where TCJA individual tax provisions expire and business taxes revert to previously scheduled increases starting in 2026.

The good news for taxpayers across the nation is that the OBBBA is projected to reduce federal taxes, on average, for individual taxpayers in every single state. However, the magnitude of these reductions varies significantly. In 2026, taxpayers in Wyoming are anticipated to experience the largest average tax cuts, amounting to $5,478. They are closely followed by Washington, with an average cut of $5,445, and Massachusetts, where taxpayers are expected to see an average reduction of $5,259. These states, often characterized by higher incomes or significant capital gains activity, are positioned to benefit substantially from the Act’s provisions. Conversely, taxpayers in West Virginia ($2,448) and Mississippi ($2,386) are projected to see the smallest average tax cuts in the same year, reflecting different economic structures and income distributions.

Zooming in to the county level reveals even more pronounced disparities. The most substantial average tax cuts are predominantly concentrated in affluent mountain resort towns, indicative of high-net-worth individuals and business owners. Teton County, Wyoming, for instance, is estimated to receive an extraordinary average tax cut of $39,316 per taxpayer in 2026, making it the highest in the entire U.S. Pitkin County, Colorado, follows with an average of $22,717, and Summit County, Utah, secures the third spot with $15,477. These figures underscore how the Act’s benefits, particularly those related to capital income, pass-through business income, and certain deductions, disproportionately favor regions with higher concentrations of wealth. In stark contrast, rural counties, such as Loup County, Nebraska, are expected to see the smallest average tax cuts, with an average reduction of $731 in 2026, highlighting the varying economic impact across different demographics and geographic areas.

Average Tax Cut Dynamics: A National and Temporal Perspective

Across all individual tax filers nationwide, the average tax cut per taxpayer is estimated to be $3,813 in 2026. This figure is a composite of individual tax changes, which reduce tax liability by an average of $2,272, and business tax cuts, which contribute an additional $1,541 on average.

However, this average tax cut is not static over time. It is projected to decrease to $2,590 in 2030. This decline is primarily attributed to the expiration of certain individual changes, such as the deductions for tipped and overtime income, which are not permanently enshrined in the legislation. After this dip, the average tax cut is expected to rebound, rising to $3,163 by 2035. This subsequent increase is driven by the effects of inflation, where inflation refers to when the general price of goods and services increases across the economy, reducing the purchasing power of a currency. As inflation increases the nominal value of the permanent tax cuts, their real impact, though diminished, results in a higher nominal tax reduction over time.

Specific Provisions and Their Targeted Impacts

The OBBBA’s intricate design means that specific tax changes have distinct geographic and demographic impacts. One notable example is the State and Local Tax (SALT) deduction cap. Initially set at $40,000, this cap is scheduled to decrease to $10,000 after 2029, and includes certain income limits. This provision is expected to have the most significant impact on taxpayers residing in higher-tax localities, predominantly found on the U.S. coasts. These areas often have higher property values and local income taxes, meaning more taxpayers will feel the constraint of the deduction cap, potentially leading to a higher effective tax burden for them. The debate around the SALT cap has been politically charged, with many lawmakers from high-tax states advocating for its repeal or significant increase, arguing it unfairly targets their constituents.

Conversely, the expanded Child Tax Credit and standard deduction are designed to provide broader relief, particularly benefiting middle- and lower-income families across all regions. The permanence of 100 percent bonus depreciation and domestic R&D expensing for businesses will likely spur investment in states with robust manufacturing, technology, and innovation sectors, potentially leading to job growth and economic expansion in those areas. The new deductions for tipped and overtime income, while temporary, are targeted to benefit service industry workers and hourly wage earners, providing a direct financial boost to these critical segments of the labor force.

Economic Growth and Job Creation

Beyond direct tax savings, a primary objective of the OBBBA is to stimulate economic growth and job creation. The Tax Foundation estimates that the Act will lead to an increase of approximately 828,000 full-time equivalent (FTE) jobs over the long run. This projected growth is a direct consequence of the business tax cuts, which are expected to incentivize increased investment, expanded operations, and heightened R&D activities, thereby creating demand for additional labor. Individual tax cuts also contribute by boosting consumer spending and savings, further fueling economic activity.

The distribution of these new jobs will also exhibit geographic variation. California, with its vast economy and diverse industries, is projected to see the largest increase, with over 116,000 new jobs. Texas, another economic powerhouse, is expected to add about 72,000 jobs. These states, characterized by large populations, significant business activity, and diverse economic bases, are well-positioned to capitalize on the investment incentives. On the other end of the spectrum, smaller states like Vermont are estimated to gain approximately 1,500 new jobs. These figures underscore how the Act’s economic stimulus is broadly distributed but scaled by the size and composition of state economies.

Methodology and Analytical Framework

The comprehensive analysis of the OBBBA’s impact is rooted in robust methodological frameworks employed by the Tax Foundation. The estimates for the geographic distribution of tax changes under the OBBBA’s individual and business provisions are derived from conventional revenue estimates at the national level, which are generated by the Tax Foundation’s sophisticated General Equilibrium Model. It’s important to note that, within this specific map-based analysis, the impact of the OBBBA’s estate tax changes – an estate tax is imposed on the net value of an individual’s taxable estate at the time of death – is not included.

To allocate national revenue estimates to individual tax filers within specific counties, the analysis leverages data from the IRS Statistics of Income for individual tax returns from 2022. This IRS data provides granular detail on various tax characteristics broken down by county. These characteristics are then used to proportionally distribute the conventional national revenue estimates for each of the OBBBA’s provisions, as outlined in Table 2 (not provided here, but inferred from the original text). The county-level figures are subsequently averaged by the number of filers in each respective county. The accuracy of this county-level analysis is, however, subject to the limitations of the IRS data, particularly for newer and more narrowly targeted OBBBA provisions, such as the deduction for tipped income, where granular data may be less comprehensive.

For the OBBBA’s business provisions, the analysis adopts an economic incidence framework. It assumes that the burden and benefit of corporate taxes are borne partly by capital income and partly by labor income, a conclusion supported by several economic studies. Specifically, the model posits that the corporate tax is initially borne predominantly by capital income (90 percent in the first year), with the burden gradually shifting to labor income over time until it is evenly split between capital and labor income in the long run (50 percent capital income and 50 percent labor income in the fifth year and beyond). This dynamic incidence assumption provides a more realistic depiction of the long-term effects of corporate tax changes. The state-level job impacts are allocated based on the national jobs estimated by the Tax Foundation’s General Equilibrium Model and the existing distribution of labor and capital income across the states.

Broader Implications and Future Outlook

The OBBBA’s passage marks a critical juncture in U.S. fiscal policy. The permanence of key TCJA provisions and the introduction of new tax cuts carry significant implications for the national debt and future budget projections. While proponents argue that the economic growth stimulated by the Act will partially offset revenue losses, critics often point to the potential for increased deficits if growth targets are not met or if other spending priorities are not curtailed.

The Act’s impact on business investment and international competitiveness is expected to be substantial. By making bonus depreciation and R&D expensing permanent, the U.S. aims to solidify its position as an attractive destination for capital investment and innovation. This could lead to a long-term boost in productivity and technological advancement. For individual taxpayers, the enhanced disposable income from tax cuts, even with the temporal fluctuations, could foster increased savings, consumption, or investment, depending on individual economic circumstances.

Looking ahead, the OBBBA is likely to remain a subject of intense political and economic debate. As certain provisions phase out or evolve, particularly the SALT cap and temporary deductions, future legislative sessions may revisit these elements. The Act’s legacy will be continually assessed through its measurable effects on economic growth, job creation, income distribution, and the nation’s fiscal health. The detailed modeling and ongoing analysis provided by organizations like the Tax Foundation will be instrumental in understanding these complex and evolving impacts, ensuring an informed public discourse on the future of American tax policy.