The landscape of retirement savings in the United States has undergone a significant transformation over the last five years, primarily driven by legislative efforts to bridge the "retirement gap" among small business employees. For small business owners, the decision to offer a 401(k) plan is no longer merely an administrative burden but a strategic financial maneuver. By leveraging federal tax credits worth up to $16,500 and enhancing employee retention through robust benefits, small enterprises are now better positioned to compete with large corporations. Understanding the intricacies of setting up these plans, the compliance requirements involved, and the financial incentives provided by the SECURE Act is essential for any business owner looking to optimize their corporate structure and support their workforce’s long-term financial health.

The Legislative Catalyst: The SECURE Act and SECURE 2.0

The primary driver behind the recent surge in small business 401(k) adoption is the Setting Every Community Up for Retirement Enhancement (SECURE) Act, signed into law in late 2019, and its successor, SECURE 2.0, passed in 2022. Prior to this legislation, many small business owners cited high administrative costs and complex regulatory requirements as insurmountable barriers to offering retirement benefits. According to data from the Bureau of Labor Statistics, only about 53% of workers at small private-sector firms had access to retirement benefits in 2020, compared to 90% at larger firms.

The SECURE Act addressed these disparities by significantly increasing the tax credits available to employers. Specifically, the "Credit for Small Employer Plan Start-up Costs" was expanded to cover 50% of qualified startup costs, up to a cap of $5,000 per year for three years. SECURE 2.0 further enhanced this for businesses with 50 or fewer employees, increasing the credit to 100% of startup costs. Additionally, a $500 annual credit is available for three years to employers who implement an automatic enrollment feature in their plans. Collectively, these credits can reach $16,500 over a three-year period, effectively neutralizing the initial cost of establishing a plan for many small businesses.

Strategic Benefits of Employer-Sponsored Retirement Plans

Beyond tax incentives, the implementation of a 401(k) serves as a critical tool for human capital management. In a competitive labor market, retirement benefits are often cited by prospective employees as a top-three priority, alongside salary and health insurance. By offering a 401(k), small businesses can reduce turnover rates, which industry analysts estimate can cost a company 1.5 to 2 times an employee’s annual salary.

From a tax perspective, the benefits are two-fold. Employers can deduct their contributions to employee accounts as a business expense, reducing the company’s overall tax liability. For employees, contributions are typically made on a pre-tax basis (in traditional 401(k) models), which lowers their current taxable income while allowing their investments to grow tax-deferred until retirement. The introduction of Roth 401(k) options also provides flexibility, allowing for after-tax contributions that provide tax-free income in retirement.

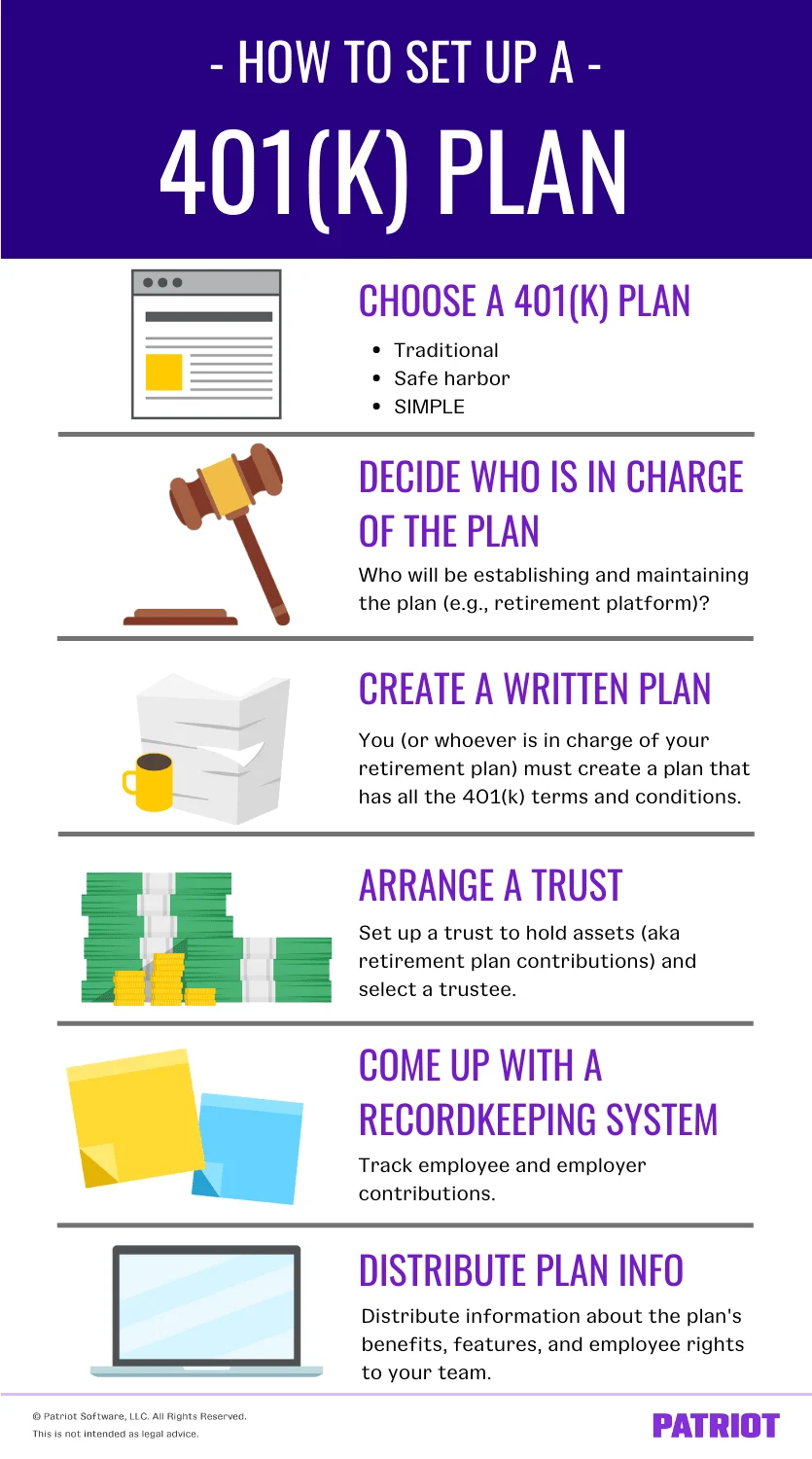

A Chronological Roadmap to Plan Establishment

Setting up a 401(k) requires a structured approach to ensure compliance with the Employee Retirement Income Security Act (ERISA). The following chronology outlines the essential phases of implementation:

Phase 1: Selecting the Plan Structure

The first step involves choosing a plan type that aligns with the business’s size and financial goals.

- Traditional 401(k): Offers the most flexibility but requires annual "nondiscrimination testing" to ensure the plan does not unfairly favor highly compensated employees (HCEs).

- Safe Harbor 401(k): Requires the employer to make fully vested contributions to all employees. In exchange, the plan is exempt from most annual nondiscrimination testing.

- SIMPLE 401(k): Designed for businesses with 100 or fewer employees, this plan has lower contribution limits but simplified reporting requirements.

- Solo 401(k): Ideal for owner-only businesses or those with only a spouse as an employee.

Phase 2: Partnering with Service Providers

Small businesses must decide who will manage the plan. Most owners hire a third-party administrator (TPA) or a financial institution to act as the "recordkeeper." This entity tracks contributions, earnings, and distributions. Additionally, a "Plan Trustee" must be designated to manage the plan’s assets, often a role filled by a professional investment firm to mitigate the employer’s fiduciary liability.

Phase 3: Formalizing the Plan Document

A written plan document serves as the legal foundation of the 401(k). This document outlines eligibility requirements (e.g., age 21 and one year of service), contribution limits, vesting schedules, and whether the plan allows for loans or hardship withdrawals. This document must be formally adopted by the business’s board or owners.

Phase 4: Asset Custody and Recordkeeping

The employer must establish a trust for the plan’s assets to ensure they are held separately from the business’s general assets. A recordkeeping system must then be integrated with the company’s payroll software to ensure that salary deferrals are accurately tracked and deposited into the trust in a timely manner—usually within seven business days for small plans.

Phase 5: Employee Disclosure and Enrollment

Transparency is a legal mandate under ERISA. Employers must distribute a Summary Plan Description (SPD) to all eligible employees. This document explains how the plan works and what their rights are. If the plan includes automatic enrollment, employees must be notified of their right to opt out or change their contribution percentage.

Financial Implications: Costs vs. Credits

While the SECURE Act credits are substantial, business owners must still account for the gross costs of plan maintenance. Setup fees generally range from $1,500 to $3,000, covering the drafting of legal documents and system integration. Ongoing costs include:

- Administrative Fees: Costs for recordkeeping, document updates, and customer service.

- Investment Fees: Often charged as a percentage of assets under management (AUM), these cover the cost of the investment funds themselves.

- Individual Service Fees: Fees for specific actions, such as processing a loan or a Qualified Domestic Relations Order (QDRO).

Industry data suggests that for a plan with $1 million in assets and 50 participants, total annual fees typically hover around 1% to 1.5% of assets. However, many of these costs are now offset by the aforementioned tax credits, making the net cost to the employer historically low.

Compliance and Maintenance Protocols

The establishment of a 401(k) is not a "set it and forget it" endeavor. Ongoing compliance is monitored by the Internal Revenue Service (IRS) and the Department of Labor (DOL).

Nondiscrimination Testing

For traditional plans, the Actual Deferral Percentage (ADP) and Actual Contribution Percentage (ACP) tests must be performed annually. These tests ensure that the average deferral rate of HCEs (those earning more than $155,000 in 2024 or owning more than 5% of the business) does not exceed the average deferral rate of non-HCEs by more than a specified margin. If a plan fails these tests, the employer may be required to refund contributions to HCEs or make additional contributions to non-HCEs.

Reporting and Disclosure

Most 401(k) plans must file Form 5500 annually. This form provides the government with details regarding the plan’s financial condition and operation. For plans with fewer than 100 participants, the simplified Form 5500-SF or 5500-EZ may be used. Furthermore, employers are required to provide participants with an Individual Benefit Statement (IBS) at least quarterly (for participant-directed plans) and a Summary Annual Report (SAR) each year.

Analysis of Broader Economic Impact

The shift toward small business 401(k) adoption reflects a broader economic trend: the decentralization of retirement security. As state governments increasingly mandate that employers provide retirement options (e.g., California’s CalSavers or Illinois’ Secure Choice), many small businesses are choosing to implement their own private 401(k) plans rather than enrolling in state-run programs. Private plans offer higher contribution limits and more investment flexibility than state-mandated IRAs.

Economists suggest that the expansion of these plans could have a stabilizing effect on the long-term economy. By incentivizing private savings through small businesses, the reliance on Social Security may be mitigated for future generations. Furthermore, the "democratization" of investment tools—previously the domain of large corporate employees—allows a wider demographic of the American workforce to participate in capital markets, potentially narrowing the wealth gap over time.

Expert Consensus and Future Outlook

Financial advisors and tax professionals generally agree that the current window for starting a 401(k) is uniquely favorable due to the expiration dates of certain SECURE Act provisions and the rising pressure of state mandates. "The combination of 100% startup cost credits and the ability to attract better talent makes the 401(k) a standard requirement for modern small businesses, not a luxury," notes one industry analyst.

As we move toward 2025, the industry expects further refinements in "starter 401(k)" plans—a new category introduced by SECURE 2.0 that allows for even lower administrative hurdles for very small firms. For the small business owner, the message is clear: the regulatory and financial environment has been optimized to make retirement plan sponsorship a viable, and arguably necessary, component of business operations. Success in this area requires a diligent focus on provider selection, a clear understanding of fiduciary duties, and a proactive approach to employee communication.