Business owners face an ever-growing list of responsibilities, and among the most critical, yet often overlooked, is the meticulous management and retention of payroll records, a requirement enshrined in federal law and subject to varying state-specific mandates, with retention periods sometimes extending up to five years or more. This essential compliance task is not merely administrative; it forms the bedrock of financial accountability, employee protection, and defense against potential audits and legal challenges from multiple governmental agencies. Understanding the specific requirements, timelines, and best practices for payroll recordkeeping is paramount for any enterprise aiming to maintain legal standing and operational integrity.

The landscape of payroll record retention is multifaceted, involving a complex interplay of regulations from agencies such as the Internal Revenue Service (IRS), the Department of Labor (DOL) under the Fair Labor Standards Act (FLSA), and the Equal Employment Opportunity Commission (EEOC), alongside a patchwork of state-level statutes. Each agency possesses distinct mandates concerning the types of records to be kept, the duration of their retention, and the rationale behind these requirements. For instance, while the IRS focuses on employment tax documentation for a period of four years, the FLSA prioritizes wage and hour records for three years, with a shorter two-year period for wage computation data. The EEOC, conversely, mandates the retention of personnel and employment action records for one year, extending indefinitely should a discrimination claim arise. This intricate web necessitates a comprehensive approach to record management, where the longest applicable retention period often dictates the practical benchmark for businesses.

The Foundation of Compliance: Why Payroll Records Matter

The requirement to maintain detailed payroll records stems from several fundamental objectives of government oversight. Primarily, these records serve as the verifiable evidence of an employer’s adherence to tax laws, wage and hour regulations, and anti-discrimination statutes. For the IRS, accurate records ensure the correct assessment and collection of federal income tax withholding, Social Security, Medicare (FICA), and federal unemployment taxes (FUTA). Without these documents, the government’s ability to verify tax liabilities and prevent evasion would be severely hampered.

Similarly, the Department of Labor utilizes payroll records to confirm that employers are compensating their workers in accordance with the FLSA, which governs minimum wage, overtime pay, recordkeeping, and child labor standards. These records provide the basis for investigating wage disputes, ensuring employees receive fair compensation, and preventing exploitation. From the EEOC’s perspective, personnel and employment records are crucial for investigating claims of discrimination based on race, color, religion, sex, national origin, age, disability, or genetic information. They allow the commission to ascertain whether hiring, promotion, termination, or other employment decisions were made on a lawful basis.

Beyond regulatory compliance, robust payroll recordkeeping offers internal benefits to businesses. It provides a clear historical account of employee compensation, benefits, and employment history, which can be vital for internal audits, budgeting, and human resource management. In an era where data integrity and transparency are increasingly valued, well-maintained records contribute to a business’s reputation for ethical practices and good governance.

Defining "Payroll Records": A Comprehensive Overview

The term "payroll records" encompasses a wide array of documents and data points that track an employee’s journey from hire to termination and beyond. It is not limited to mere pay stubs but includes foundational documents, compensation details, tax filings, and employment-related actions. Key categories of records include:

- Employee Identifying Information: Full name, address, Social Security Number (SSN), occupation, sex, and date of birth (especially for employees under 19).

- Compensation Details:

- Regular hourly rate of pay, or the basis on which wages are paid (e.g., salary, piece rate, commission).

- Total daily or weekly straight-time earnings.

- Total overtime earnings for the workweek.

- Additions to or deductions from wages (and their explanations).

- Total wages paid each pay period.

- Date of payment and the pay period covered by the payment.

- Hours Worked: Timecards, timesheets, work schedules, and any other records showing the exact hours worked each workday and total hours worked each workweek. For exempt employees, while daily/weekly hours may not be tracked, basic pay basis and workweek records are still required.

- Tax Documentation:

- Employee’s Form W-4 (Employee’s Withholding Certificate).

- Copies of Forms W-2 (Wage and Tax Statement) and W-3 (Transmittal of Wage and Tax Statements).

- Employer’s federal tax returns, such as Form 941 (Employer’s Quarterly Federal Tax Return), Form 940 (Employer’s Annual Federal Unemployment (FUTA) Tax Return), and Form 944 (Employer’s Annual Federal Tax Return).

- Records of federal tax deposits made.

- Benefit Records: Documentation related to employee benefits, such as health insurance enrollment, retirement plan contributions, and leave accruals.

- Personnel Actions: Applications for employment, resumes, records relating to hiring, promotion, demotion, transfer, layoff, termination, rates of pay, job assignments, awards, training, and disciplinary actions.

- Other Related Documents: Collective bargaining agreements, travel vouchers, expense reimbursement receipts, and correspondence with governmental agencies related to employment or payroll.

The critical distinction between wage computation records (like timesheets) and broader payroll records (like tax forms) often dictates differing retention periods, underscoring the granular detail required for compliance.

Federal Agency Mandates: A Detailed Breakdown

Understanding the specific requirements of each federal agency is crucial for developing a robust record retention strategy.

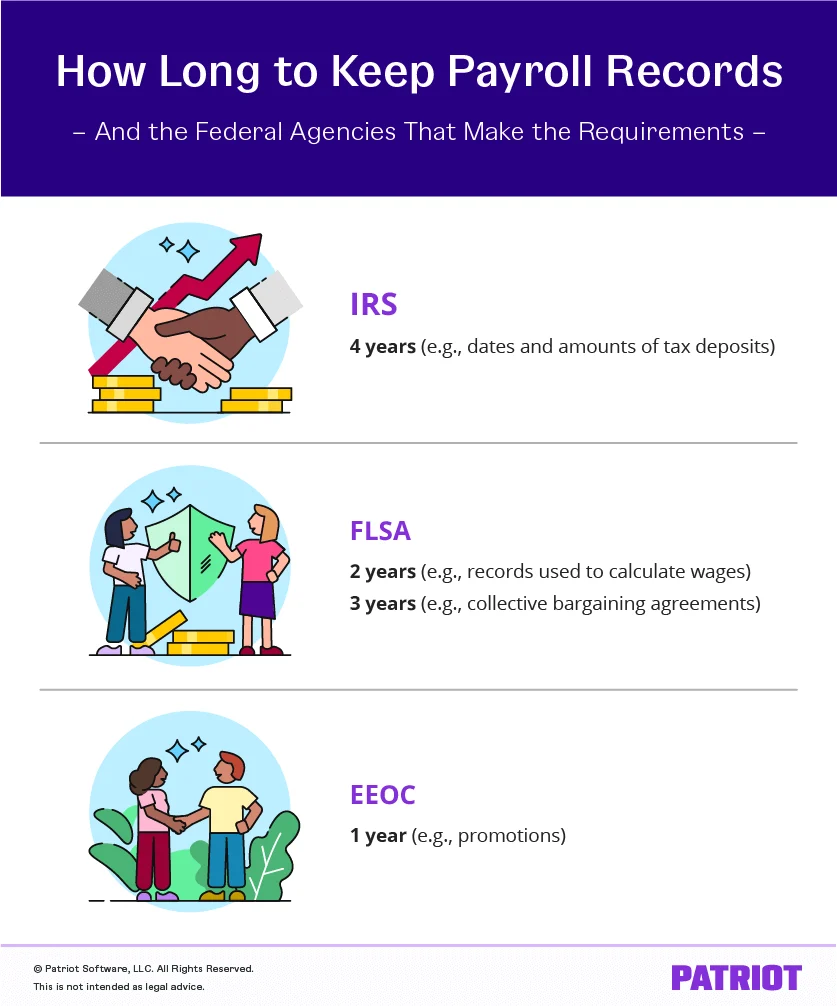

1. Internal Revenue Service (IRS): The Tax Watchdog

The IRS, primarily concerned with the accurate assessment and collection of federal taxes, mandates that employers retain all records pertaining to employment taxes. This includes documentation that supports amounts reported on federal tax returns, substantiates tax deposits, and confirms employee compensation.

- Records Required: Dates and amounts of tax deposits, employer identification number, employee names, addresses, SSNs, dates of employment, dates and amounts of wage payments, tips, fringe benefits, and copies of all filed tax forms (W-4, W-2, 940, 941, etc.).

- Retention Period: Generally, these records must be kept for four years after the due date of the tax return for the period to which the records relate, or the date the tax was paid, whichever is later. This extended period allows the IRS ample time to conduct audits and verify past tax filings.

- Rationale: To ensure the proper calculation and payment of federal income tax withholding, Social Security and Medicare taxes (FICA), and Federal Unemployment Tax (FUTA). These records serve as the primary evidence in case of an audit.

2. Fair Labor Standards Act (FLSA) – Department of Labor (DOL): Ensuring Fair Wages

Administered by the Wage and Hour Division of the DOL, the FLSA sets standards for minimum wage, overtime pay, child labor, and, crucially, recordkeeping. Its focus is on protecting employees from unfair labor practices.

- Records Required: Employee’s full name, address, SSN, occupation, sex, date of birth (if under 19), time and day of week when employee’s workweek begins, regular hourly rate of pay, total daily or weekly straight-time earnings, total overtime earnings for the workweek, all additions to or deductions from wages, total wages paid each pay period, and date of payment and the pay period covered.

- Retention Periods:

- Three years: For basic payroll records, collective bargaining agreements, sales and purchase records. This longer period allows for the investigation of wage disputes and historical compliance checks.

- Two years: For records used to calculate wages, such as time cards, timesheets, work schedules, records of additions/deductions to wages, and records explaining the basis for wage differentials.

- Rationale: To enable the DOL to verify that employers are complying with minimum wage and overtime requirements, particularly in industries where hourly wages and fluctuating schedules are common. These records are fundamental to resolving wage claims.

3. Equal Employment Opportunity Commission (EEOC): Upholding Non-Discrimination

The EEOC enforces federal laws prohibiting employment discrimination. Its recordkeeping requirements are designed to allow the investigation of discrimination charges and ensure fair treatment in the workplace.

- Records Required: Detailed employment records, including job applications, resumes, interview notes, records related to hiring, promotion, demotion, transfer, layoff, termination, rates of pay, job assignments, awards, training, disciplinary actions, and requests for accommodation.

- Retention Period: Generally, records concerning employment (such as hiring, promotion, demotion, or termination) must be kept for one year from the date of the personnel action or the creation of the record, whichever is later. If an employee is involuntarily terminated, these records must be retained for one year from the date of termination.

- Special Circumstance: If an employee files a discrimination charge under Title VII of the Civil Rights Act, the Americans with Disabilities Act (ADA), or the Genetic Information Nondiscrimination Act (GINA), all related records must be preserved until the final disposition of that charge, which can extend retention significantly beyond the standard one-year period.

- Rationale: To provide a verifiable paper trail for all employment decisions, allowing the EEOC to determine if discrimination played a role in an employment outcome.

State-Specific Requirements: Adding Layers of Complexity

While federal mandates provide a baseline, many states impose their own, often more stringent, payroll record retention requirements. These state laws can dictate longer retention periods or require additional types of records to be kept. For example:

- California and Arizona: Both states require employers to retain payroll records for at least four years, aligning with or extending beyond some federal requirements.

- Montana: Employers in Montana are mandated to keep records for five years.

- New York: Generally requires employers to retain payroll records and wage statements for up to six years, significantly longer than most federal provisions.

The variations extend beyond duration, sometimes encompassing specific documentation related to state income tax, unemployment insurance, workers’ compensation, or unique state labor laws. The cardinal rule for businesses operating in multiple jurisdictions, or even within a single state with varying federal and state laws, is to always adhere to the longer retention period. This approach minimizes risk and ensures compliance across all applicable regulations. Consulting state labor departments or legal counsel is highly recommended for precise guidance on state-specific obligations.

Consequences of Non-Compliance: The High Cost of Oversight

Failing to maintain accurate and accessible payroll records can expose businesses to significant financial penalties, legal liabilities, and reputational damage. The implications of non-compliance are severe and multi-faceted:

- Financial Penalties:

- IRS: Penalties for inaccurate or unfiled tax forms, failure to make timely deposits, and record-keeping deficiencies can range from hundreds to thousands of dollars per violation, plus interest. In cases of intentional disregard, penalties can be even more substantial.

- DOL (FLSA): Employers found in violation of FLSA recordkeeping requirements may face civil money penalties, ranging from hundreds to tens of thousands of dollars per violation, especially for repeat or willful infractions. Additionally, they may be liable for unpaid back wages, liquidated damages, and attorney’s fees if an employee sues.

- EEOC: While direct penalties for recordkeeping are less common, the absence of proper records can severely weaken an employer’s defense in a discrimination lawsuit, potentially leading to substantial financial settlements, back pay awards, and court-ordered remedies.

- Legal Action: Employees can initiate private lawsuits against employers for wage and hour violations or discrimination, where the lack of adequate records can be used as evidence against the employer. Government agencies can also pursue legal action.

- Audits and Investigations: Non-compliance often triggers more intensive and prolonged audits from regulatory bodies, consuming significant time and resources. A lack of organized records can exacerbate the audit process, leading to further scrutiny and potential findings of additional violations.

- Reputational Damage: News of regulatory violations or employee lawsuits can severely harm a company’s reputation, making it difficult to attract and retain talent, secure business partnerships, and maintain customer trust.

- Operational Disruption: The scramble to reconstruct missing records during an audit or lawsuit can divert critical resources from core business operations, impacting productivity and profitability.

Reports from organizations like the National Federation of Independent Business (NFIB) often highlight that regulatory compliance, including recordkeeping, is a significant burden for small businesses, and a leading cause of audit-related penalties. It’s estimated that a substantial percentage of IRS employment tax audits uncover discrepancies directly related to insufficient or inaccurate payroll records.

Best Practices for Payroll Recordkeeping and Audit Readiness

Given the stringent requirements and severe consequences, adopting robust recordkeeping practices is not optional but a strategic imperative.

- Centralized and Organized System: Implement a system that allows for easy storage, retrieval, and categorization of all payroll-related documents. This could be a secure cloud-based payroll software or a meticulously organized physical filing system.

- Electronic vs. Paper: Both electronic and paper records are acceptable, provided they are accurate, legible, complete, and readily accessible for the entire retention period.

- Electronic Records: Offer benefits in terms of searchability, security (with proper backups and encryption), and reduced physical storage needs. Ensure scanned paper records are high-quality reproductions of the original.

- Paper Records: Must be stored securely in a fire-safe, locked environment with controlled access.

- Data Security and Privacy: Payroll records contain sensitive employee data (SSNs, financial information). Implement strong security measures, including encryption, access controls (role-based permissions), regular backups, and physical security for paper files, to protect against data breaches and unauthorized access, in compliance with data privacy laws.

- Retention Schedule and Destruction Policy: Develop a clear, written record retention schedule that outlines the specific documents, their required retention periods based on federal and state laws, and a documented process for their secure destruction once those periods expire. Crucially, implement a "litigation hold" policy to pause any destruction if an audit, claim, or lawsuit is pending.

- Accessibility for Audits: Records must be made available to federal agencies (like the DOL) within a reasonable timeframe, often 72 hours of notice, even if stored offsite or centrally. This necessitates an efficient retrieval system.

- Special Cases:

- Terminated Employees: Retain records for terminated employees according to the longest applicable timeline (e.g., IRS four years, FLSA three years, EEOC one year post-termination if involuntary, or indefinitely if a claim is pending).

- Minors and Youth Employment: Include date of birth (if under 19) and adhere strictly to FLSA timekeeping and retention rules, as child labor laws are particularly scrutinized.

- Independent Contractors: While FLSA timekeeping rules don’t apply, IRS requires retention of 1099-NEC forms and payment records for at least four years.

- Regular Review and Updates: Periodically review recordkeeping policies and practices to ensure they remain compliant with evolving federal and state regulations.

Leveraging Technology for Enhanced Compliance

The advent of sophisticated payroll software has revolutionized recordkeeping, transforming it from a manual, error-prone task into an automated, streamlined process. Modern payroll solutions offer:

- Automated Record Generation: Automatically generate and store pay stubs, tax forms (W-2, 941), and other essential payroll reports.

- Centralized Digital Storage: Securely store all payroll data in a cloud-based environment, accessible from anywhere, ensuring business continuity and disaster recovery.

- Compliance Features: Built-in features that help track employee hours, calculate wages and overtime, and apply correct tax withholdings, significantly reducing the risk of errors.

- Audit Trails: Maintain detailed logs of all transactions and changes, providing an immutable audit trail for every payroll event.

- Reporting Capabilities: Generate comprehensive reports on demand, making it easier to respond to auditor requests and analyze payroll data.

- Integration: Seamlessly integrate with HR and time-tracking systems, creating a unified data ecosystem that minimizes manual data entry and ensures consistency.

By adopting such technologies, businesses can not only meet their recordkeeping obligations more efficiently but also gain valuable insights into their labor costs and operational efficiency, mitigating risks and fostering greater financial transparency.

Conclusion: A Proactive Stance on Payroll Compliance

In the complex and ever-evolving regulatory landscape, payroll record retention is far more than a bureaucratic burden; it is a fundamental aspect of responsible business stewardship. From safeguarding against IRS penalties and FLSA wage claims to defending against EEOC discrimination charges, accurate and accessible records are the employer’s primary defense. The varying requirements across federal and state agencies demand a proactive, diligent approach, with a strong emphasis on adhering to the longest applicable retention periods and leveraging technology to streamline processes. By prioritizing robust recordkeeping, businesses not only fulfill their legal obligations but also fortify their operational resilience, protect their financial health, and uphold their commitment to fair and ethical employment practices. Ignoring these mandates is a gamble no responsible business owner can afford to take.