The landscape of energy taxation across the European Union and the United Kingdom is poised for a significant snapshot on January 1, 2026, as excise duties on gas and diesel continue to evolve under the dual pressures of fiscal necessity and ambitious climate targets. This date marks a crucial point in the ongoing efforts to balance national revenue generation with environmental sustainability and economic competitiveness. These excise duties, meticulously defined to apply to petroleum and diesel with a sulphur content of less than 10 mg/kg and RON 95 (gas), incorporate various components including bioethanol content and, where applicable, carbon taxes and additional surcharges. For international comparative analysis, these duties are converted into USD using a stipulated exchange rate of 1 EUR to 1.1747 USD, as of January 1, 2026. This intricate system reflects a complex interplay of environmental mandates, economic realities, and sovereign fiscal policies across one of the world’s most economically integrated regions and a key former member state.

The Historical Evolution of Fuel Taxation in Europe

Fuel taxation in Europe is not a recent phenomenon but rather a deeply entrenched fiscal instrument with a history spanning several decades. Initially, excise duties on motor fuels were primarily conceived as a means for national governments to generate substantial revenue, often earmarked for infrastructure development, such as road maintenance and construction. These early taxes were also seen as a lever to manage energy consumption and ensure energy security.

The establishment of the European Union introduced a new layer of complexity and coordination. Recognizing the potential for market distortions and unfair competition arising from disparate national tax rates, the EU sought to harmonize certain aspects of energy taxation. This led to the adoption of the Energy Taxation Directive (ETD) in 2003 (Council Directive 2003/96/EC). The ETD set minimum rates for excise duties on various energy products, including motor fuels, across all Member States. Its primary objectives were to ensure the proper functioning of the internal market, prevent "fuel tourism" (where consumers purchase fuel in countries with lower taxes), and contribute to environmental protection by promoting cleaner fuels. However, the ETD allowed Member States considerable flexibility to set rates above these minimums, leading to significant variations in fuel prices across the bloc, a situation that persists to this day. This directive has been the cornerstone of EU energy taxation policy, albeit one that has faced increasing scrutiny and calls for revision in light of evolving climate challenges.

The EU’s Green Deal and the "Fit for 55" Package: A Catalyst for Change

The urgency of climate change has profoundly reshaped the discourse around energy taxation. With the adoption of the Paris Agreement and the subsequent launch of the European Green Deal in 2019, the EU committed to ambitious targets, including reducing net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels, and achieving climate neutrality by 2050. These targets necessitated a comprehensive overhaul of existing policy instruments, including the ETD.

In July 2021, the European Commission unveiled its "Fit for 55" legislative package, a sweeping set of proposals designed to align EU policies with its climate objectives. A key component of this package was a proposal to revise the ETD. The proposed revisions aim to update the minimum tax rates, which have largely remained unchanged since 2003, and to better reflect the environmental performance of different fuels. This includes taxing polluting fuels more heavily and promoting the uptake of sustainable alternatives. Specifically, the revised ETD seeks to:

- Remove outdated exemptions and reductions: Many fossil fuels currently benefit from tax exemptions, such as those used in aviation and maritime transport, or for certain industrial processes. The revision aims to phase out these exemptions.

- Introduce a more coherent structure: The proposal suggests linking tax rates to the energy content and environmental performance of fuels, ensuring that more polluting fuels face higher taxation.

- Integrate carbon pricing: While the EU Emissions Trading System (ETS) covers some sectors, the revised ETD aims to ensure that carbon costs are more broadly reflected in energy prices, including for road transport and heating fuels, through national excise duties.

- Promote sustainable fuels: Fuels from renewable sources, such as advanced biofuels and hydrogen, would benefit from more favourable tax treatment to encourage their development and adoption.

The January 1, 2026, date is significant in this context as it falls within the expected implementation window for these proposed revisions. While the legislative process for the revised ETD is complex and subject to negotiations among Member States and the European Parliament, the direction of travel is clear: a move towards higher and more environmentally differentiated excise duties on fossil fuels across the EU. This anticipated shift underscores the Commission’s commitment to using fiscal policy as a tool for decarbonization, signaling to industries and consumers alike the increasing cost of carbon-intensive activities.

The United Kingdom’s Independent Trajectory Post-Brexit

Following its departure from the European Union, the United Kingdom has regained full autonomy over its fiscal policies, including fuel duties. However, its approach continues to be shaped by similar economic and environmental considerations. Historically, the UK implemented a "Fuel Duty Escalator" in the 1990s and early 2000s, which saw fuel duty rates increase above inflation annually. This policy was aimed at both revenue generation and discouraging fuel consumption.

However, in response to rising fuel prices and concerns about the cost of living, successive UK governments have largely frozen fuel duty rates for over a decade. This freeze has been a significant fiscal decision, foregoing billions in potential revenue but providing relief to motorists and businesses. As of January 1, 2026, the UK’s fuel duty policy will continue to reflect this balancing act. The Office for Budget Responsibility (OBR), the UK’s independent fiscal watchdog, regularly highlights the implications of the fuel duty freeze for public finances and the broader economy, noting the erosion of the tax base as vehicles become more fuel-efficient and the transition to electric vehicles accelerates.

Despite the freeze, the UK remains committed to its own legally binding net-zero target by 2050. This commitment suggests that while direct excise duty increases might be politically sensitive, the government will need to explore alternative mechanisms to disincentivize fossil fuel use and encourage the shift to sustainable transport. These could include road pricing, vehicle excise duty reforms, or other carbon pricing instruments that align with the UK’s climate ambitions, potentially influencing the effective cost of fuel beyond the nominal excise duty rate. The UK’s strategy will need to navigate the immediate economic pressures faced by households and businesses against its long-term environmental obligations, creating a unique policy path distinct from, yet parallel to, the EU’s evolving framework.

Understanding the Intricate Components of Fuel Duties

The excise duties applicable on January 1, 2026, are not monolithic but rather a composite of several elements, each designed to address specific policy objectives.

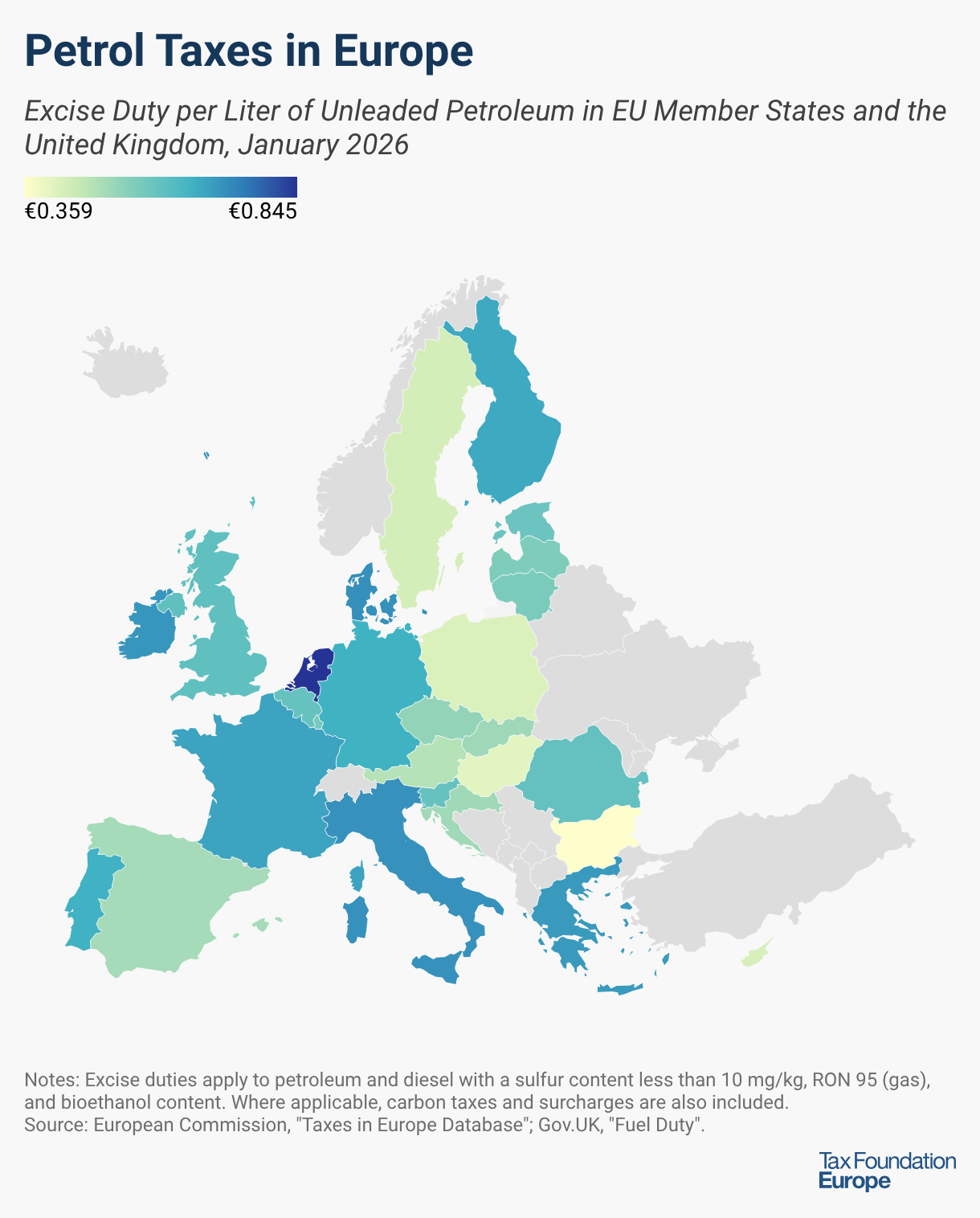

- Base Excise Duty: This is the fundamental tax levied per liter of fuel. Its primary purpose is revenue generation for the national treasury. As noted, the EU’s ETD sets minimums, but national governments are free to impose higher rates. The significant variation across Member States—from some of the lowest rates in countries like Bulgaria and Hungary to some of the highest in the Netherlands and Finland—reflects national economic conditions, fiscal priorities, and environmental ambitions.

- Carbon Taxes and Surcharges: Increasingly, governments are integrating explicit carbon taxes or surcharges into fuel duties. These are designed to internalize the external cost of carbon emissions, making polluting fuels more expensive and incentivizing a shift to lower-carbon alternatives. While some EU countries already have national carbon taxes on fuels, the proposed revision of the ETD aims to harmonize this approach more broadly. These surcharges directly contribute to the "polluter pays" principle, reflecting the environmental impact of fuel consumption.

- Bioethanol Content: The specified inclusion of "bioethanol content" is crucial. Many countries mandate a certain percentage of biofuels (like bioethanol in petrol, or biodiesel in diesel) to be blended with fossil fuels. Biofuels are typically seen as having a lower lifecycle carbon footprint than pure fossil fuels. Tax regimes often differentiate based on this content, sometimes offering reduced duties for fuels with higher sustainable biofuel blends, thereby encouraging their use and supporting agricultural sectors that produce these fuels.

- Technical Specifications (Sulphur Content & RON 95): The mention of "sulphur content of < 10 mg/kg" and "RON 95 (gas)" refers to the quality and type of fuel being taxed. Low-sulphur fuels are standard across Europe due to environmental regulations aimed at reducing air pollution. RON 95 (Research Octane Number 95) is a common grade of unleaded petrol. These specifications ensure that the duties apply consistently to widely used, environmentally compliant fuels, preventing loopholes or ambiguities based on fuel quality.

- Currency Conversion: The stipulated exchange rate of 1 EUR to 1.1747 USD is vital for international comparison. Given the global nature of energy markets and the need for transparent data, converting national excise duties into a common currency like the USD allows analysts, policymakers, and the public to compare the tax burden on fuel across different jurisdictions more effectively. This standardization is critical for assessing competitiveness, trade implications, and the relative cost of energy across diverse economies.

Economic and Fiscal Implications

Excise duties on fuel represent a significant and stable revenue stream for national governments. In many EU Member States and the UK, these taxes contribute billions of euros or pounds annually to public coffers, funding essential services and infrastructure projects. For instance, in 2022, fuel duties constituted a substantial portion of tax revenues for several European nations, demonstrating their importance beyond mere environmental incentives. The stability of this revenue, however, is increasingly challenged by improvements in vehicle fuel efficiency and the accelerating transition to electric vehicles, which do not consume fossil fuels and thus do not contribute to fuel duty receipts.

The imposition of these duties has direct and indirect economic impacts. Directly, they increase the pump price of petrol and diesel, affecting consumers’ disposable income and the operating costs for businesses, particularly those in the transport and logistics sectors. This can lead to inflationary pressures, as higher transport costs filter through supply chains to consumer goods and services. The variations in duty levels across Member States also create dynamics such as "fuel tourism," where drivers near borders may cross into a neighboring country to purchase cheaper fuel, impacting local businesses and tax revenues in the higher-tax jurisdiction.

Furthermore, the economic impact is not uniform. Fuel duties can be regressive, disproportionately affecting lower-income households who may spend a larger percentage of their income on transport, especially in rural areas where public transport options are limited. This raises questions of social equity and the need for compensatory measures or targeted support to mitigate adverse effects on vulnerable populations. For industries, particularly those reliant on road haulage, higher fuel costs can erode competitiveness, potentially leading to calls for exemptions or subsidies, thereby complicating the policy landscape.

Industry and Consumer Perspectives

The implementation and potential increases in excise duties on fuel are met with varied reactions from different stakeholders.

Industry Concerns: The road transport and logistics sectors frequently voice concerns about the impact of high and rising fuel duties. For haulage companies, fuel is a major operating cost. Increases in duties directly translate to higher expenses, which can be difficult to absorb in a competitive market. This often leads to calls for duty freezes, reductions, or targeted relief measures to maintain competitiveness and prevent price increases for goods. Industry bodies argue that excessive duties could stifle economic growth, particularly for small and medium-sized enterprises (SMEs), and might even encourage companies to relocate operations to countries with lower energy costs. They also highlight the need for a predictable policy environment to facilitate long-term investment in greener fleets and infrastructure.

Consumer Impact: For the average motorist, fuel duties are a tangible component of the cost of living. Price fluctuations at the pump due to duty changes or market forces can significantly impact household budgets. Consumer advocacy groups often emphasize the regressive nature of fuel taxes, arguing that they disproportionately burden those with lower incomes, particularly in regions with limited public transport. They advocate for fair pricing, transparency, and consideration of the socio-economic impact of tax policies. While some consumers may be incentivized to reduce driving or consider alternative modes of transport, for many, especially those in rural areas or with specific commuting needs, reducing fuel consumption is not immediately feasible.

Environmental Advocacy: Conversely, environmental groups generally support higher excise duties on fossil fuels, viewing them as an essential tool to discourage consumption and accelerate the transition to a low-carbon economy. They argue that the external costs of pollution and climate change are not fully reflected in current fuel prices and that increased duties, especially carbon taxes, help internalize these costs. These groups often advocate for the revenue generated from such taxes to be ring-fenced for investment in public transport, renewable energy, and electric vehicle charging infrastructure, creating a virtuous cycle that supports sustainable transitions. They also stress the importance of clear, long-term policy signals to drive innovation and investment in greener technologies.

The Road Ahead: Future of Energy Taxation

The January 1, 2026, perspective on excise duties on gas and diesel is merely a waypoint in a much longer journey towards a sustainable and equitable energy future. As the world progresses towards decarbonization, the traditional model of fuel taxation faces fundamental challenges.

The rapid electrification of the transport sector, particularly the proliferation of electric vehicles (EVs), presents a significant fiscal dilemma. As more vehicles transition away from internal combustion engines, the revenue base for fuel duties will inevitably shrink. This impending decline necessitates a rethinking of how governments will fund road infrastructure and other public services currently supported by fuel taxes. Discussions are already underway across Europe and the UK regarding alternative revenue mechanisms, such as:

- Road Pricing/Congestion Charges: Levying charges based on distance traveled, time of day, or specific road usage. This could be a more equitable system, taxing actual road use rather than fuel consumption, and could be adapted for both conventional and electric vehicles.

- Vehicle Excise Duty (VED) Reform: Adjusting annual vehicle taxes to better reflect environmental impact or vehicle weight, irrespective of fuel type.

- Broader Carbon Pricing: Expanding carbon pricing mechanisms to cover all energy sources, ensuring a consistent incentive across the economy to reduce emissions.

- Energy Consumption Taxes: Shifting from fuel-specific taxes to broader energy consumption taxes, potentially based on energy content or environmental impact, applicable to all forms of energy used for transport and heating.

The debates surrounding the revision of the ETD within the EU, and the ongoing policy considerations in the UK, underscore the complexity of designing energy tax systems that simultaneously meet fiscal needs, achieve climate goals, and address social equity concerns. The challenge lies in creating a predictable and coherent framework that encourages sustainable behavior without unduly burdening households and businesses, while also adapting to technological advancements and evolving energy mixes. The focus will increasingly shift from taxing the input (fossil fuels) to taxing the output (emissions) or the service (mobility), reflecting a deeper integration of environmental costs into economic activity.

In conclusion, the excise duties on gas and diesel in the European Union and the United Kingdom as of January 1, 2026, represent a critical juncture in the ongoing evolution of energy taxation. They embody the complex balance national governments and the EU collectively strive to achieve between generating essential revenue, mitigating climate change, and ensuring economic stability and social fairness. This snapshot reveals not just the existing tax rates but also the underlying policy philosophies and the direction of future reforms, signaling a continued commitment to leveraging fiscal instruments in the pursuit of a greener, more sustainable future for transport across the continent.