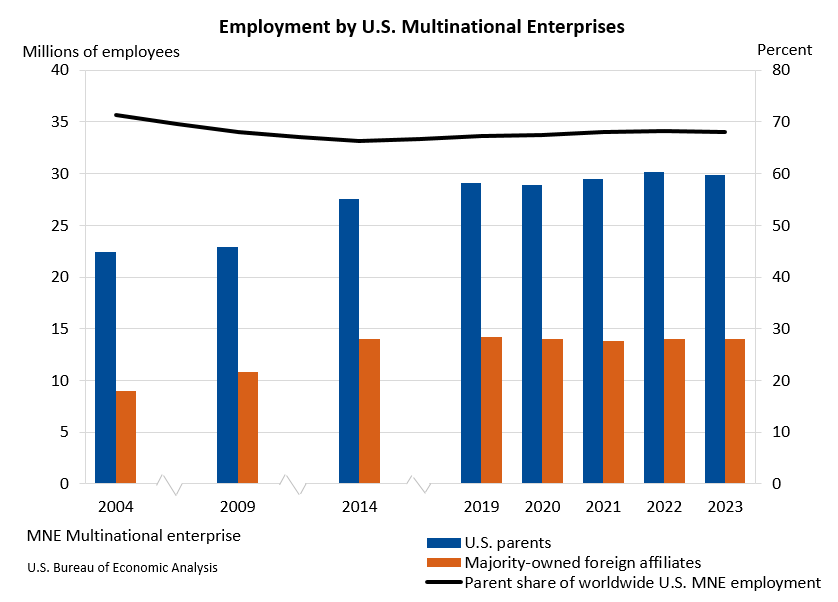

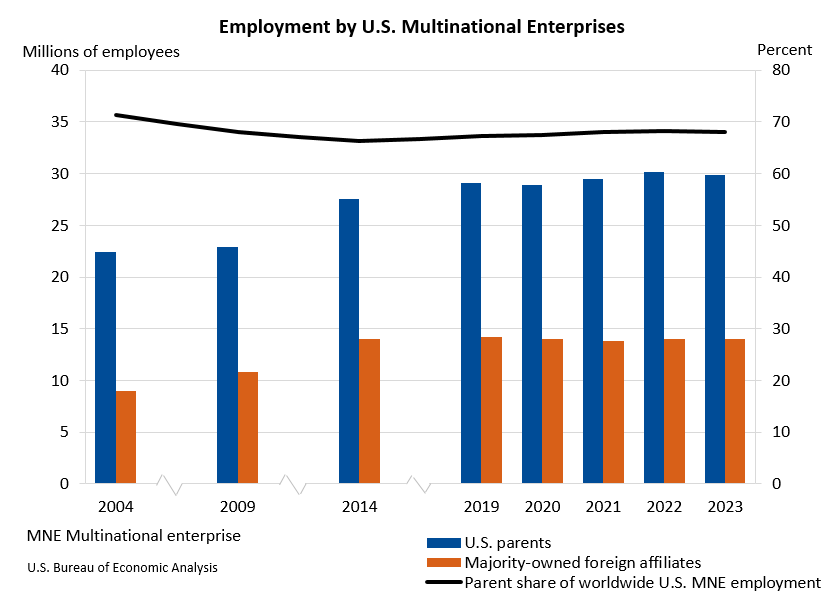

Worldwide employment by U.S. multinational enterprises (MNEs) experienced a slight decrease of 0.4 percent in 2023, falling to 43.9 million workers from a revised 44.1 million in 2022. This preliminary data, released by the U.S. Bureau of Economic Analysis (BEA), offers a snapshot of the operational and financial landscape of American parent companies and their global affiliates. The figures indicate a nuanced economic environment, with a notable contraction in domestic employment within U.S. parent companies partially offset by modest growth in their foreign operations.

Domestic Employment Contracts, Foreign Employment Expands

The primary driver of the overall decline in employment was a 0.8 percent reduction in the workforce of U.S. parent companies, which employed 29.9 million individuals in 2023. Despite this dip, U.S. parents still constituted the vast majority of worldwide employment by these enterprises, accounting for 68.1 percent of the total. This share, however, represents a slight decrease from 68.3 percent in 2022, signaling a marginal shift in the geographical distribution of employment within these global corporations.

In contrast, employment abroad by the foreign affiliates of U.S. MNEs saw a modest uptick of 0.2 percent, reaching 14.0 million workers. This expansion means that foreign affiliates now account for 31.9 percent of the total global workforce employed by U.S. MNEs. This divergence between domestic and international employment trends suggests a complex interplay of factors influencing hiring decisions, potentially including evolving market conditions, labor costs, and strategic investment decisions by American multinational corporations.

U.S. Parents’ Share of Private Industry Employment Dips

The significance of U.S. parent companies in the broader U.S. private industry employment landscape also saw a slight diminution. In 2023, U.S. parents accounted for 21.9 percent of total private industry employment in the United States, down from 22.5 percent in the preceding year. This suggests that while still a substantial employer, their relative contribution to the overall U.S. job market experienced a minor decline.

The leading sectors for employment within U.S. parent companies remained consistent, with manufacturing continuing to be the largest employer. Following closely were "other industries," notably driven by strong activity in transportation and warehousing, and the retail trade sector. These sectors represent core areas of operation and investment for American businesses with a global footprint.

Key Hubs for Foreign Affiliate Employment

Globally, the foreign affiliates of U.S. MNEs concentrated their employment in several key regions. India, Mexico, and the United Kingdom emerged as the top destinations for employment by these majority-owned foreign affiliates. The specific country-level data provides insight into where U.S. companies are strategically placing their operational and manufacturing facilities, likely influenced by factors such as market access, labor availability, and regulatory environments.

Economic Output and Investment Trends

Beyond employment figures, the BEA data also sheds light on the economic output and investment activities of U.S. MNEs. The worldwide current-dollar value added by these enterprises, a measure of their direct contribution to economic output, decreased by 0.6 percent to $6.9 trillion in 2023.

Within this global figure, the value added by U.S. parents, which directly contributes to the U.S. Gross Domestic Product (GDP), saw a more pronounced decline of 1.0 percent, reaching $5.3 trillion. This decline lowered their share of total U.S. private-industry value added to 21.4 percent from 23.1 percent in 2022, mirroring the trend observed in employment.

Conversely, the value added by majority-owned foreign affiliates experienced a growth of 0.8 percent, amounting to $1.6 trillion. This indicates that while the overall economic contribution of U.S. MNEs saw a slight dip, their foreign operations continued to expand their economic output. The primary contributors to this foreign affiliate value added were located in the United Kingdom, Canada, and Ireland, highlighting these nations as significant economic partners for U.S. multinational corporations.

Capital Expenditures and R&D Investment Surge

In stark contrast to the modest contraction in employment and value added, worldwide expenditures on property, plant, and equipment (capital expenditures) by U.S. MNEs surged by a significant 7.5 percent, reaching $1.1 trillion in 2023. This robust increase in capital investment signals a strong commitment to expanding physical assets and infrastructure by these global entities.

Of this total, U.S. parents accounted for $886.1 billion in capital expenditures, while majority-owned foreign affiliates invested $216.2 billion. The substantial investment by U.S. parents underscores a continued focus on domestic infrastructure and operational enhancements.

Further underscoring a forward-looking strategy, worldwide research and development (R&D) expenditures by U.S. MNEs also saw a substantial increase of 7.5 percent, reaching $558.3 billion. This parallel surge in both capital investment and R&D spending suggests a strategic push by U.S. multinational enterprises to innovate, enhance productivity, and secure future growth.

U.S. parents were the primary drivers of this R&D investment, accounting for $476.6 billion, while their majority-owned foreign affiliates contributed $81.7 billion. This indicates a strong emphasis on maintaining R&D leadership within the United States, while still investing in innovation across their global operations.

Context and Chronology of Data Release

The U.S. Bureau of Economic Analysis regularly compiles and releases comprehensive statistics on the operations and finances of U.S. parent companies and their foreign affiliates. This annual data release provides critical insights into the global economic footprint of American businesses. The preliminary statistics for 2023, released in August 2024, are based on the latest available source data, with revisions incorporated for the 2022 figures. The BEA previously published preliminary estimates for 2022 in September 2024, which were highlighted in the Survey of Current Business. These updates allow for a continuous and refined understanding of the dynamic activities of U.S. multinational enterprises.

Analysis and Implications

The BEA’s 2023 data paints a picture of a globalized economy where U.S. multinational enterprises are navigating a complex landscape. The slight decline in overall employment, primarily concentrated within the U.S. parent companies, could be attributed to a variety of factors. These might include ongoing efforts to optimize operational efficiency, shifts in manufacturing processes, or a strategic redeployment of resources in response to evolving market demands and geopolitical considerations. The increasing share of employment held by foreign affiliates suggests a growing reliance on international labor markets for certain functions or a strategic expansion of operations in regions offering competitive advantages.

The divergent trends in employment and investment are particularly noteworthy. While overall employment saw a minor contraction, the significant increases in capital expenditures and R&D spending by both U.S. parents and their foreign affiliates point towards a strong underlying confidence in future growth and innovation. This suggests that U.S. MNEs are prioritizing investments in long-term value creation, even as they manage their current workforce size. The surge in R&D expenditures, in particular, signals a commitment to developing new technologies and products, which could lead to future employment growth and economic expansion.

The data also highlights the continued importance of key international markets for U.S. businesses. The prominent roles of India, Mexico, and the United Kingdom in employing workers through foreign affiliates underscore their significance as operational hubs. Similarly, the concentration of value added by foreign affiliates in countries like the United Kingdom, Canada, and Ireland points to their strategic economic importance in the global value chains of U.S. multinational corporations.

Broader Economic Significance

The activities of U.S. multinational enterprises have a profound impact on the U.S. and global economies. Their employment figures represent a significant portion of the labor market, their investments shape industrial development, and their R&D activities drive technological innovation. The BEA’s detailed data allows policymakers, economists, and businesses to understand these complex interdependencies and to formulate strategies that foster economic growth and competitiveness.

The trend of U.S. parents’ declining share of both total employment and value added within the U.S. private sector, while seemingly modest, warrants continued observation. It could indicate a broader economic shift towards a more service-oriented economy, or potentially a greater concentration of certain types of economic activity in international locations. However, the simultaneous robust investment in capital and R&D within the U.S. suggests a continued commitment to domestic innovation and modernization.

Future Outlook and Data Accessibility

The BEA will release the 2024 activities of U.S. Multinational Enterprises in November 2026. Until then, the 2023 data provides the most current comprehensive overview. The BEA offers extensive data tables and resources on its website, allowing for in-depth analysis of specific industries, countries, and financial metrics. This accessibility is crucial for a thorough understanding of the multifaceted operations of U.S. multinational enterprises and their evolving role in the global economic landscape. The discontinuation of certain historical data tables, as noted by the BEA, signifies an ongoing effort to streamline data reporting and focus on current relevance, while also archiving older data for historical reference.