For countless entrepreneurs, the journey of building a business often begins with a hands-on approach to every operational facet, including financial management. Initially, handling one’s own bookkeeping—tracking expenses, managing invoices, and reconciling accounts with a simple spreadsheet or basic software—is a pragmatic decision driven by tight budgets and straightforward transaction volumes. This do-it-yourself (DIY) methodology serves as a vital foundation for nascent ventures, allowing founders to maintain direct oversight of every financial entry. However, as businesses mature and expand, the very practices that once fostered agility can become significant impediments to sustainable growth, demanding a strategic shift towards professional financial stewardship.

The Evolution of Financial Management in a Growing Business

The transition from a fledgling startup to a thriving enterprise introduces a myriad of complexities that inevitably outpace the capabilities of ad-hoc bookkeeping. What starts as a handful of transactions quickly escalates into a complex web of sales, purchases, payroll, inventory management, and potentially multi-jurisdictional tax obligations. This natural progression often pushes business owners to a critical juncture where the time and mental energy diverted to financial administration begin to detract from core business activities, such as sales, product development, and strategic planning.

Industry analysts and small business surveys frequently highlight that inadequate financial management is a leading cause of small business failure. A 2022 report by the U.S. Small Business Administration, for instance, indicated that a significant percentage of business closures could be linked to poor financial planning and cash flow management. While this doesn’t directly pinpoint DIY bookkeeping as the sole culprit, it underscores the critical need for accurate, timely, and insightful financial data, which becomes increasingly difficult to maintain without specialized expertise.

The initial phase of DIY accounting, typically spanning the first 1-3 years, is characterized by:

- Direct Oversight: The owner has intimate knowledge of every financial detail.

- Cost Efficiency: Minimal out-of-pocket expenses for accounting services.

- Simplicity: Suitable for businesses with low transaction volumes and uncomplicated financial structures.

However, as a business scales, the disadvantages become pronounced:

- Time Consumption: Hours spent on manual data entry and reconciliation, diverting focus from revenue-generating activities.

- Increased Error Risk: Greater transaction volume and complexity amplify the chances of costly mistakes, from miscategorized expenses to unreconciled accounts.

- Compliance Challenges: Keeping pace with evolving tax laws, payroll regulations, and industry-specific compliance requirements becomes a formidable task for non-experts.

- Lack of Strategic Insight: Without proper financial analysis, businesses operate in the dark, unable to make informed decisions about pricing, expansion, or investment.

DIY Bookkeeping Versus Professional Accounting: A Detailed Comparison

Both approaches aim to achieve accurate and useful financial information, but the methodologies and outcomes diverge significantly. Understanding these differences is crucial for any business owner contemplating a shift.

DIY Accounting:

In a DIY setup, the business owner or a designated team member assumes responsibility for:

- Transaction Recording: Logging all income and expenses, often manually or using basic software.

- Bank Reconciliation: Matching bank statements with recorded transactions.

- Invoice Management: Creating and sending invoices, tracking receivables.

- Basic Reporting: Generating rudimentary profit and loss statements or balance sheets.

- Payroll Processing: Managing employee wages, taxes, and deductions, often using separate software.

- Receipt Management: Storing and categorizing physical or digital receipts.

While offering lower immediate out-of-pocket costs and direct visibility into every transaction, DIY accounting is inherently time-consuming, prone to errors, and struggles to adapt to dynamic regulatory landscapes. It is best suited for businesses with extremely simple operations and minimal growth ambitions.

Professional Accounting:

Engaging a professional accountant or Certified Public Accountant (CPA) introduces a layer of expertise and efficiency. A professional typically handles:

- Comprehensive Bookkeeping: Ensuring all transactions are accurately recorded, categorized, and reconciled.

- Financial Statement Preparation: Producing reliable profit & loss statements, balance sheets, and cash flow reports.

- Tax Planning and Preparation: Optimizing tax strategies, preparing and filing all necessary tax returns (federal, state, local).

- Payroll Management: Overseeing or executing payroll processing, including compliance with wage and tax laws.

- Financial Analysis and Advisory: Providing insights into financial performance, cash flow, profitability, and offering strategic guidance.

- Audit Support: Representing the business in case of tax audits.

- Compliance Assurance: Staying abreast of changing financial regulations and ensuring the business adheres to them.

The advantages of professional accounting are substantial: significant time savings for the business owner, a drastic reduction in error risk, access to expert advice for strategic decision-making, and robust compliance assurance. While it represents an added cash expense, many businesses find this investment yields substantial returns through improved efficiency, avoided penalties, and optimized financial performance. The "sweet spot" for many growing small businesses often lies in a hybrid approach: leveraging simple cloud-based software for daily operational tasks, with a professional accountant providing oversight, cleanup, and strategic counsel.

Identifying the Tipping Point: Signs Your Business Has Outgrown DIY

Waiting for a financial crisis to engage professional help is a reactive and potentially costly mistake. Proactive recognition of the signs of growth and complexity can facilitate a smoother transition.

-

Bookkeeping Consumes Disproportionate Time: If administrative financial tasks regularly spill into evenings, weekends, or detract significantly from core business hours, it signals an unsustainable burden. This opportunity cost — the value of what you could be doing instead — often far exceeds the cost of hiring a professional. Entrepreneurs should focus on high-value activities that drive revenue and innovation, not routine data entry.

-

Increased Business Complexity: Growth inherently brings complexity. This might manifest as:

- Hiring Employees: Introducing payroll, benefits, and associated tax compliance.

- Managing Inventory: Requiring sophisticated tracking, valuation, and cost-of-goods-sold calculations.

- Expanding to New Markets or Locations: Navigating new tax jurisdictions and regulatory environments.

- Securing Loans or Investments: Requiring detailed, accurate financial projections and historical performance data.

- Diversifying Revenue Streams: Adding services, products, or sales channels that complicate revenue recognition.

More complexity directly translates to a higher potential for financial errors and compliance breaches.

-

Lack of Confidence in Financial Numbers: If financial reports evoke uncertainty or apprehension rather than clarity, it’s a critical red flag. Operating without reliable data leads to suboptimal decision-making, from incorrect pricing strategies to misjudged investment opportunities. This can erode profitability and hinder growth. A professional accountant provides the assurance of accurate, verifiable data.

-

Chronic Tax Season Stress: For many DIY bookkeepers, tax season becomes an annual ordeal of frantic scrambling, document hunting, and last-minute calculations. This stress often indicates a lack of organized, year-round financial management. An accountant can streamline this process, ensure all deductions are claimed, and help proactively plan for tax liabilities, turning a chaotic period into a manageable one.

-

Desire for Strategic Financial Advice: When an entrepreneur’s questions evolve beyond "What was my profit last month?" to "How can I improve my cash flow?", "Should I invest in new equipment?", "What are my most profitable product lines?", or "How can I prepare for a future acquisition?", it signifies a need for strategic financial partnership. Professional accountants offer insights into key performance indicators, budgeting, forecasting, and long-term financial planning that raw data simply cannot provide.

The Strategic Imperative: Beyond Compliance to Growth

The decision to hire a professional accountant is not merely about offloading tedious tasks or ensuring compliance; it is a strategic investment in the business’s future. A robust financial framework, guided by professional expertise, transforms finances from a necessary evil into a powerful tool for sustainable growth and long-term viability.

- Enhanced Decision-Making: Accurate, timely financial reports empower owners to make informed decisions about pricing, operational efficiencies, market expansion, and capital allocation.

- Improved Access to Capital: Banks and investors require meticulous financial records and projections. Professional accounting provides the credibility necessary to secure loans, attract investment, and facilitate business sales.

- Optimized Tax Planning: Beyond mere compliance, accountants can implement strategies to minimize tax liabilities legally, freeing up capital for reinvestment.

- Risk Mitigation: Professionals identify and mitigate financial risks, from fraud to non-compliance penalties, safeguarding the business’s assets and reputation.

- Business Valuation: Clean books are essential for accurately valuing a business, whether for internal strategic purposes or external transactions.

Preparing for a Seamless Transition: A Step-by-Step Guide

A smooth handover to a professional accountant requires some preparatory work, which can significantly reduce initial costs and accelerate the onboarding process.

-

Choose Simple, Cloud-Based Accounting Software: Even with an accountant, businesses still need a system for day-to-day operations. Cloud-based software offers accessibility, real-time collaboration, and automation features. Look for platforms that are user-friendly, scalable, offer bank feeds for automated transaction import, and provide robust reporting capabilities. Software like Patriot Accounting is designed to facilitate seamless teamwork between owners and their accountants.

-

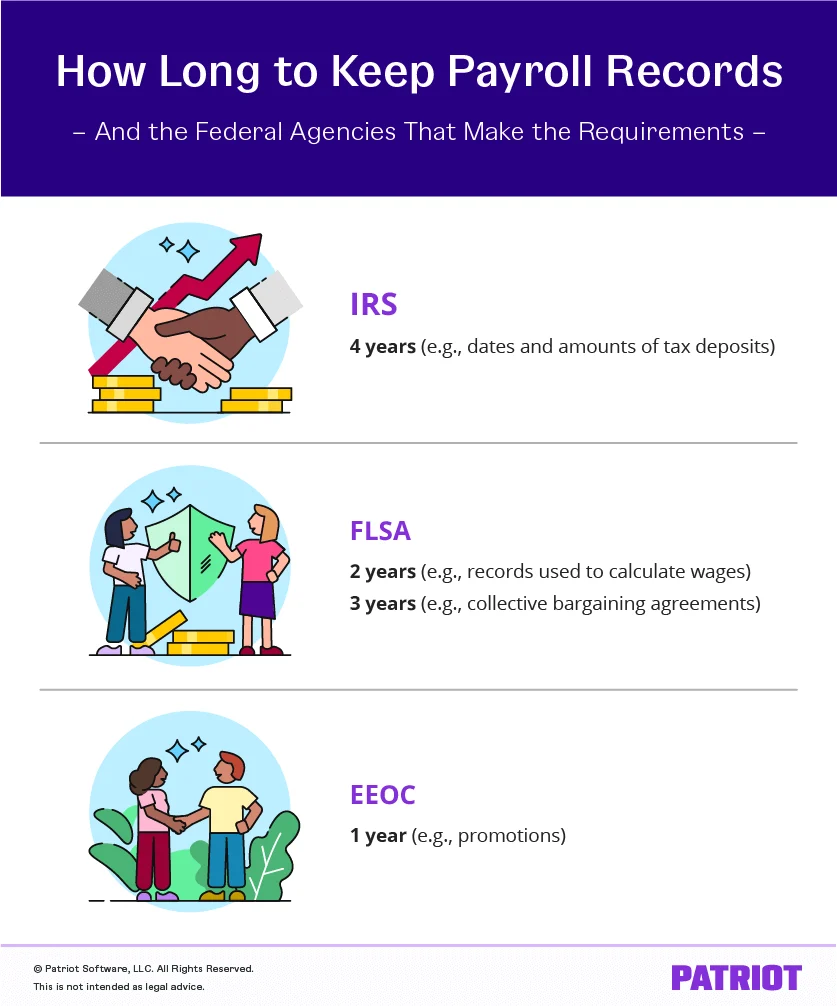

Gather and Organize Financial Documents: Before the initial meeting, collect all pertinent financial records. This includes:

- Recent bank and credit card statements (at least the last 12-24 months).

- Prior year’s business tax returns.

- Any existing bookkeeping records (spreadsheets, previous software files).

- Loan agreements, lease contracts, and significant asset purchase documentation.

- Legal formation documents (Articles of Incorporation/Organization).

- Payroll records, if applicable.

- Sales tax records.

Organize these documents by year and month, preferably in digital format, for easy sharing and reference.

-

Clean Up What You Can (But Don’t Stress): While accountants are adept at cleanup jobs, performing basic organization beforehand can save time and money.

- Reconcile the most recent bank statements.

- Categorize obvious income and expenses.

- Identify and flag any questionable transactions or discrepancies.

The goal is not perfection, but rather to provide a clearer starting point. Unsure how to categorize something? Leave it flagged; your accountant will address it.

-

Document Your Current Process: Write down a brief overview of how you currently manage finances:

- How income is received and recorded.

- How bills are paid and expenses tracked.

- Your payroll process.

- How often you reconcile accounts.

- Any specific software or tools you use.

This documentation offers your accountant a clear snapshot of your existing financial workflows, enabling them to understand your operations quickly and recommend improvements.

Selecting the Right Financial Partner: More Than Just Numbers

Choosing an accountant is a critical decision. It’s about finding a trusted advisor who understands your business and aligns with your long-term goals.

-

Look for Relevant Experience and Specialization: Ask potential accountants about their experience with businesses of your size and within your industry. An accountant familiar with your sector will understand common challenges, opportunities, and specific compliance requirements. Inquire about their CPA designation, which signifies a high level of expertise and ethical standards.

-

Inquire About Services and Pricing Models: Clarify the scope of services included (bookkeeping, payroll, tax preparation, advisory). Understand their fee structure:

- Hourly: Common for one-off projects or initial cleanup.

- Fixed Monthly Fee: Predictable costs for ongoing services, popular for small businesses.

- Value-Based Pricing: Fees tied to the value delivered, rather than hours.

Ensure transparency in pricing to avoid surprises and budget effectively.

-

Assess Communication and Compatibility: You need an accountant with whom you feel comfortable asking questions, regardless of how basic they may seem. Look for someone who:

- Communicates clearly and explains complex financial concepts in an understandable way.

- Is responsive to inquiries.

- Uses technology (like cloud software) to facilitate collaboration.

- Demonstrates a proactive approach to financial advice.

This is a long-term partnership, and a strong communication fit is paramount for mutual success.

Leveraging Technology: How Accounting Software Facilitates the Transition

The right accounting software acts as the essential bridge between your daily business operations and your accountant’s expert oversight. Modern cloud-based platforms are designed for collaborative financial management, offering distinct benefits for both parties.

| Accounting Software Benefits for Business Owners | Accounting Software Benefits for Accountants |

|---|---|

| Less Data Entry: Automated bank feeds and recurring transactions save time and reduce manual effort. | Cleaner Data: Consistent categorization and standardized workflows result in more reliable financial information. |

| Real-time Visibility: Instant access to cash flow, income, and expense data empowers immediate decision-making. | Remote Access: Accountants can securely log in, review, and work on books without needing physical files or meetings. |

| Simpler Invoicing & Payments: Professional invoice generation and tracking streamline accounts receivable processes. | Efficient Reporting: Standardized, accurate financial statements can be generated quickly, facilitating analysis. |

| Expense Tracking: Easy capture and categorization of expenses via mobile apps or integrations. | Focus on Advisory: Less time spent on data entry and cleanup means more time for strategic financial advice. |

| Secure Document Storage: Centralized digital repository for financial documents. | Enhanced Collaboration: Secure sharing of documents and real-time communication within the platform. |

By utilizing robust accounting software, business owners don’t need to become bookkeeping experts. Instead, they manage the operational flow, while their professional accountant ensures accuracy, compliance, and provides strategic direction.

A Comprehensive Transition Checklist for Business Owners

Embarking on the transition from DIY to professional accounting can be broken down into manageable steps:

- Acknowledge Readiness: Recognize and commit to moving beyond DIY bookkeeping.

- Select Cloud-Based Accounting Software: Research and implement a suitable platform.

- Consolidate Financial Documents: Gather all necessary bank statements, tax returns, and records.

- Perform Initial Data Cleanup: Address obvious errors and organize existing financial data.

- Document Current Financial Processes: Outline existing workflows for income, expenses, and payroll.

- Research and Interview Accountants: Identify and select a professional with relevant experience and a good communication fit.

- Grant Secure Access: Provide your chosen accountant with secure access to your accounting software and relevant financial records.

- Collaborate on Setup & Cleanup: Allow your accountant to review, clean up historical data, and set up ongoing processes.

- Define Roles and Responsibilities: Establish clear boundaries on who handles what tasks moving forward.

- Schedule Regular Reviews: Set up periodic meetings (monthly/quarterly) to review financial performance and receive strategic advice.

Frequently Asked Questions

When is the ideal time to stop doing my own bookkeeping?

Consider making the switch when financial tasks consistently consume more than a few hours per week, when you feel uncertain about the accuracy or compliance of your records, or when your business experiences significant growth or complexity, such as hiring employees, managing inventory, or expanding to multiple locations. At this juncture, your time is typically more valuable when spent on sales, operations, and strategic development.

Do I still need accounting software if I hire an accountant?

Yes, in almost all cases. Accounting software serves as the fundamental system of record for your business. It centralizes your daily transactions, provides real-time visibility into your financial health, and significantly streamlines the process for your accountant to manage and analyze your books. Your chosen accountant can often assist in selecting and configuring the most appropriate software for your business needs.

How much does it typically cost to hire a professional accountant?

The cost varies widely based on several factors: your geographical location, the inherent complexity of your business operations, and the specific range of services you require (e.g., basic bookkeeping, comprehensive tax planning, advisory services, payroll management). Many small businesses begin with a monthly retainer package that covers essential bookkeeping and basic support. Always request a clear breakdown of pricing and what is included in their service offerings. For a tailored estimate, direct consultation with a tax professional or accountant is recommended.

What essential documents should I bring to my initial meeting with an accountant?

For your first consultation, prepare to share or provide access to: your most recent bank and credit card statements (ideally for the past 12-24 months), your prior year’s business tax returns, any existing bookkeeping records or spreadsheets you maintain, and a concise list of your primary questions, concerns, and business goals. Providing comprehensive context upfront enables your accountant to quickly understand your financial situation and offer the most pertinent advice.

Will a professional accountant assume full control over all my business finances?

Not necessarily. The division of financial responsibilities is typically a collaborative decision between you and your accountant. Many small business owners opt to retain control over day-to-day operational financial tasks such as invoicing customers, approving vendor bills, and making routine spending decisions. Your accountant’s primary focus will be on ensuring the accuracy of records, maintaining compliance with regulations, and providing strategic financial analysis and guidance.

Can an accountant rectify past bookkeeping errors or disorganization?

Absolutely. One of the common initial services provided by accountants to new clients is the cleanup of historical records. They possess the expertise to reconcile past bank statements, correct miscategorized transactions, adjust account balances to reflect actual financial positions, and generally bring your books up to a professional standard. This crucial cleanup process ensures that all subsequent reports and tax filings are built upon a reliable and accurate foundation.

In conclusion, entrepreneurs are not faced with an binary choice between managing every financial detail themselves and completely relinquishing control. By leveraging intuitive accounting software as a daily operational tool and partnering with a professional accountant for expert oversight and strategic guidance, business owners can achieve financial clarity, ensure compliance, and unlock their company’s full growth potential. This integrated approach empowers them to focus on what they do best: innovating, leading, and expanding their vision.