For virtually every business operating in the United States with employees, the IRS Form 941, officially known as the Employer’s Quarterly Federal Tax Return, stands as a critical and mandatory filing. This comprehensive document serves as the bedrock for reporting federal income tax, Social Security, and Medicare taxes that employers withhold from employee wages, alongside their own contributions to Social Security and Medicare. Given its intricate structure and the significant financial implications of errors, understanding Form 941 is not merely a bureaucratic task but a fundamental aspect of sound business management and regulatory compliance.

Understanding the Mandate: What is Form 941?

At its core, Form 941 is the Internal Revenue Service’s mechanism for tracking and collecting payroll taxes on a quarterly basis. These taxes, commonly referred to as FICA (Federal Insurance Contributions Act) taxes, fund crucial federal programs: Social Security, which provides retirement, disability, and survivor benefits, and Medicare, which offers health insurance for the elderly and disabled. The form consolidates these withholding and employer contributions, providing the IRS with a regular snapshot of a business’s payroll tax liabilities.

Historically, the establishment of Social Security in 1935 and Medicare in 1965 necessitated a robust system for funding. Quarterly reporting, via forms like the 941, ensures a steady revenue stream for these programs and allows for timely reconciliation of employer and employee contributions. This system minimizes the risk of large, unmanageable tax burdens at year-end and facilitates smoother government operations.

While most employers are required to file Form 941, there are specific exceptions. Businesses with only household employees, agricultural employees, or those that file annually using Form 944 (Employer’s Annual Federal Tax Return) typically do not file Form 941. Certain tax-exempt organizations might also have different reporting requirements. However, for the vast majority of small to medium-sized businesses, non-compliance with Form 941 filing can lead to significant penalties, including interest charges and fines for failure to file, failure to pay, and accuracy-related discrepancies. The IRS emphasizes that accurate and timely filing is paramount to avoid these financial repercussions and potential audits.

Essential Information for Accurate Form 941 Completion

Before embarking on the line-by-line completion of Form 941, employers must meticulously gather several pieces of payroll data. Accuracy in this preparatory phase is crucial, as any discrepancies will ripple through the entire form. Key information required includes:

- The employer’s Employer Identification Number (EIN), legal business name, trade name (if different), and business address.

- Total wages, tips, and other compensation paid to employees during the quarter.

- The total amount of federal income tax withheld from employee paychecks.

- The combined employee and employer portions of Social Security and Medicare taxes.

- Any adjustments to Social Security and Medicare taxes, such as those related to sick pay, unreported tips, or group-term life insurance.

- Details of any payroll tax credits, such as the credit for increasing research activities (requiring Form 8974).

- A comprehensive record of all federal tax deposits made throughout the quarter.

This data collection underscores the importance of robust payroll record-keeping systems. Many tax experts advise businesses to maintain detailed digital or physical records of all payroll transactions, including pay stubs, tax deposit receipts, and employee earnings records, for at least four years. This not only aids in Form 941 preparation but also provides essential documentation in the event of an IRS inquiry or audit.

Navigating Form 941: A Detailed Line-by-Line Breakdown

Form 941 is structured into five main parts, each addressing different aspects of an employer’s quarterly tax liability. Understanding each section is vital for accurate completion.

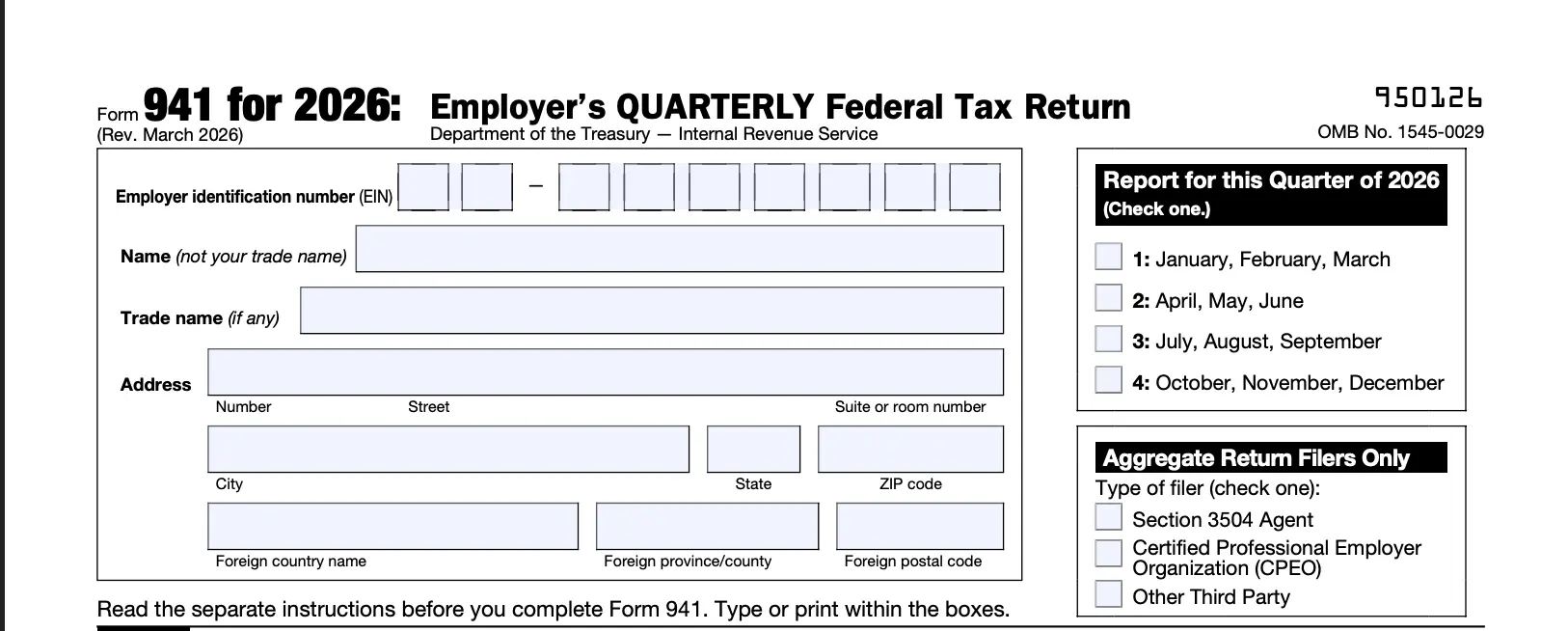

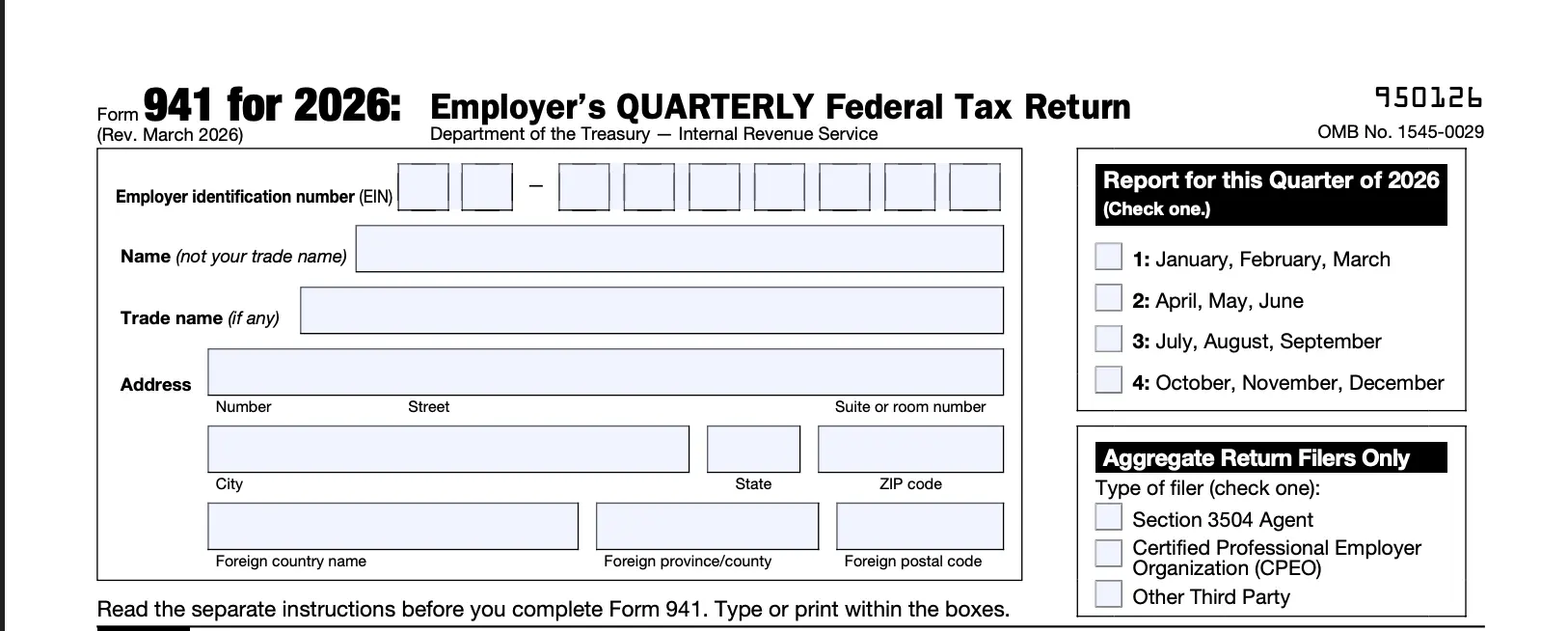

Part 0: Business and Quarter Information

This initial section, located at the top of the form, requires basic identification. Employers must input their EIN, legal business name, trade name (if applicable), and business address. Crucially, the correct quarter for which the form is being filed must be marked (e.g., January, February, March for Q1). Using the most current version of Form 941, as issued by the IRS, is imperative, as forms are frequently updated to reflect new tax laws and regulations.

Part 1: Questions for the Quarter (Lines 1-15e)

This is the most extensive section, detailing the calculation of the total tax liability.

-

Line 1: Number of Employees: This seemingly simple line often causes confusion. Employers must report the number of employees on their payroll for the pay period that includes specific dates: March 12 (Q1), June 12 (Q2), September 12 (Q3), or December 12 (Q4). Exclusions apply, such as household employees, agricultural employees, and certain nonresident aliens. For instance, if a company had 15 employees throughout the quarter but only 12 were active during the pay period encompassing September 12, only "12" would be reported.

-

Line 2: Wages, Tips, and Other Compensation: This line requires the total taxable compensation paid to all employees during the quarter, including regular wages, reported tips, and ordinary sick pay.

-

Line 3: Federal Income Tax Withheld: Employers report the total federal income tax withheld from employee wages, tips, and other compensation for the quarter. It’s important not to include income tax withheld by a third-party sick payer or qualified health plan expenses here.

-

Line 4: If No Taxable Social Security and Medicare Wages: This box is checked if no employee compensation is subject to Social Security and Medicare taxes, allowing the employer to skip several subsequent lines. This is rare for most businesses.

-

Lines 5a-5d: Taxable Social Security and Medicare Wages and Tips: These lines are central to FICA tax calculations.

- Lines 5a and 5b (Social Security): Employers must multiply taxable Social Security wages (5a) and taxable Social Security tips (5b) by 0.124. This rate represents the combined employee (6.2%) and employer (6.2%) portions of Social Security tax. It’s critical to note the Social Security wage base, which is adjusted annually by the IRS. For example, in 2024, the wage base is $168,600. Any wages paid above this annual limit are not subject to Social Security tax.

- Line 5c (Medicare): Taxable Medicare wages and tips are multiplied by 0.029, reflecting the combined employee (1.45%) and employer (1.45%) Medicare tax rate. Unlike Social Security, Medicare tax has no wage base limit; all earnings are subject to it.

- Line 5d (Additional Medicare Tax): If an employee’s wages and tips exceed a certain threshold (e.g., $200,000 for single filers), an additional 0.9% Medicare tax must be withheld. This amount is calculated by multiplying the applicable taxable wages and tips by 0.009.

-

Line 5e: Total Social Security and Medicare Taxes: This is a simple sum of the amounts from lines 5a, 5b, 5c, and 5d.

-

Line 5f: Section 3121(q) Notice and Demand (Unreported Tips): This line is specifically for employers who receive an IRS notice regarding previously unreported tips by employees.

-

Line 6: Total Taxes Before Adjustments: This aggregates the total federal income tax withheld (Line 3), total Social Security and Medicare taxes (Line 5e), and any taxes on unreported tips (Line 5f).

-

Line 7: Fractions of Cents Adjustment: This line accounts for minor rounding differences that can occur when calculating employee Social Security and Medicare taxes, which are often rounded down. This adjustment can be positive or negative.

-

Line 8: Adjustment for Third-Party Sick Pay: Used when a third-party payer (e.g., an insurance company) transfers the employer’s share of Social Security and Medicare tax liability to the employer.

-

Line 9: Adjustments for Uncollected Taxes: This line is for adjustments related to uncollected employee Social Security and Medicare taxes on tips or group-term life insurance.

-

Line 10: Total Taxes After Adjustments: The sum of lines 6 through 9, representing the total tax liability after all adjustments.

-

Line 11: Payroll Tax Credit for Increasing Research Activities: Employers claiming this nonrefundable credit, as calculated on Form 8974, enter the amount here. Form 8974 must be attached to Form 941.

-

Line 12: Total Taxes After Nonrefundable Credits: Calculated by subtracting Line 11 from Line 10. This is the final tax amount due or to be reconciled against deposits.

-

Line 13: Total Deposits for the Quarter: Employers list all federal tax deposits made for the quarter, including any overpayments from previous quarters applied to the current return.

-

Line 14: Balance Due: If Line 12 is greater than Line 13, the difference is the balance owed to the IRS. Amounts less than $1 do not need to be paid.

-

Lines 15a-15e: Overpayment: If Line 13 is greater than Line 12, an overpayment exists. Employers can choose to apply it to their next return or request a refund. Providing direct deposit information on lines 15c-15e can expedite refunds, though the IRS reserves the right to apply overpayments to any outstanding tax liabilities.

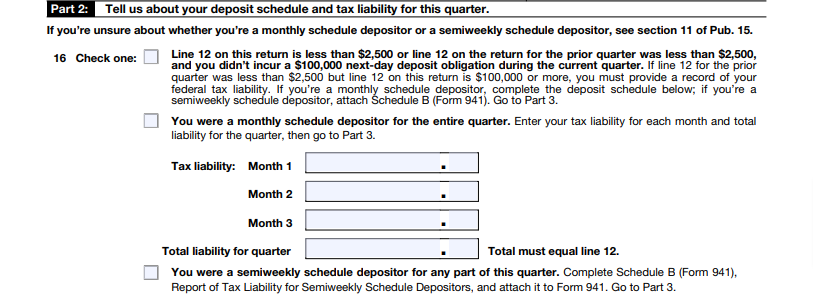

Part 2: Deposit Schedule and Tax Liability (Line 16)

This section determines how an employer reports their tax liability. Employers must indicate whether they are a "monthly depositor" or a "semiweekly depositor." This status is determined by the total tax liability reported on Form 941 during a 12-month lookback period. IRS Publication 15 provides detailed guidance on determining deposit schedules.

- Monthly Depositors: Report their total tax liability for each month of the quarter.

- Semiweekly Depositors: Must complete and attach Schedule B (Report of Tax Liability for Semiweekly Schedule Depositors), which breaks down tax liability by day.

Adherence to the correct deposit schedule is critical to avoid "failure to deposit" penalties, which can be significant, ranging from 2% to 15% of the underpayment depending on the delay.

Part 3: About Your Business (Lines 17-18)

This section addresses specific business circumstances.

- Line 17: Business Closed or Stopped Paying Wages: If a business ceased operations or stopped paying wages during the quarter, this box is checked, and the final date wages were paid is entered. A statement must be attached to the final return.

- Line 18: Seasonal Employer: Seasonal employers who do not file returns for every quarter of the year mark this box.

Part 4: Third-Party Designee

Employers can authorize an individual (e.g., a payroll specialist, accountant, or tax preparer) to discuss their Form 941 with the IRS. If "Yes" is selected, the designee’s name, phone number, and a five-digit PIN must be provided. This can be invaluable for resolving any IRS queries efficiently.

Part 5: Signature

The final section requires a signature from an authorized individual (owner, officer, partner, or fiduciary) along with their printed name, title, date, and phone number. If a paid preparer completes the form, they must fill out the "Paid Preparer Use Only" section, providing their details and signature. The IRS highly emphasizes that without a valid signature, the form is considered incomplete and may not be processed.

Submission Process and Critical Deadlines

Once completed and signed, Form 941 must be submitted to the IRS. The IRS strongly encourages electronic filing, as it is generally faster, more secure, and reduces the likelihood of errors. Various IRS-approved e-file providers are available. For those who choose to mail a paper form, the correct mailing address depends on the state where the business is located and whether a payment is enclosed. The IRS website provides specific mailing addresses.

The quarterly due dates for Form 941 are non-negotiable and are as follows:

- Quarter 1 (January 1 – March 31): Due April 30

- Quarter 2 (April 1 – June 30): Due July 31

- Quarter 3 (July 1 – September 30): Due October 31

- Quarter 4 (October 1 – December 31): Due January 31 of the following year

If a due date falls on a weekend or holiday, the deadline is shifted to the next business day. It’s worth noting that if an employer has made timely deposits of all their tax liability for the quarter, they may be granted an additional 10 calendar days to file Form 941.

Common Mistakes and Strategies for Avoidance

Despite its routine nature, Form 941 is a frequent source of employer errors. Common mistakes include:

- Incorrect Wage Base Calculations: Overlooking the Social Security wage base limit or failing to apply the additional Medicare tax when applicable.

- Misclassifying Workers: Incorrectly classifying employees as independent contractors, leading to under-reporting of payroll taxes.

- Late Deposits or Filings: Missing deposit deadlines or filing the form after the due date, incurring penalties. The penalty for failure to file is typically 5% of the unpaid tax for each month or part of a month the return is late, up to 25%. The penalty for failure to pay is 0.5% of the unpaid taxes for each month or part of a month, also capped at 25%.

- Using Outdated Forms: Relying on previous year’s forms, which may not reflect current tax laws.

- Rounding Errors: Minor mathematical errors that can lead to discrepancies, particularly in the fractions of cents adjustments.

- Inaccurate Employee Counts: Miscalculating the number of employees for Line 1 based on the specific pay period requirements.

To mitigate these risks, tax professionals universally recommend several best practices:

- Automated Payroll Systems: Utilizing payroll software or services that automate tax calculations, withholdings, and deposit schedules can drastically reduce errors. Many full-service payroll providers also handle the submission of Form 941 on behalf of their clients.

- Regular Reconciliation: Periodically reconciling payroll records with tax deposits to catch discrepancies early.

- Stay Informed: Keeping abreast of IRS changes, especially annual adjustments to wage bases and tax rates.

- Professional Review: Having a qualified accountant or tax professional review Form 941 before submission, especially for complex payroll scenarios.

The Broader Implications of Form 941 Compliance

Beyond individual business penalties, accurate and timely Form 941 compliance has broader societal implications. It ensures the integrity of the Social Security and Medicare systems, which are vital safety nets for millions of Americans. For businesses, meticulous compliance safeguards against costly audits, protects their financial standing, and reinforces their reputation as responsible corporate citizens.

In an increasingly digitized world, the IRS continues to streamline its processes, encouraging electronic filing and offering resources like its official instructions and Publication 15. The consistent message from the agency and tax experts alike is clear: understanding and accurately fulfilling the requirements of Form 941 is not just good practice, it is indispensable for any employer in the United States.