The rapid expansion of the digital economy has transformed the traditional retail landscape, giving rise to a sophisticated ecosystem of online marketplaces where third-party vendors and consumers converge. As of February 2026, the complexity of managing transactional taxes has become a primary operational hurdle for platform architects. For those establishing or maintaining a multi-seller platform, the burden of sales tax collection is no longer a peripheral concern but a core regulatory requirement that dictates the viability of the business model. This comprehensive analysis examines the current state of marketplace taxation, the strategic choices available to providers, and the technological frameworks necessary to maintain compliance in an increasingly fragmented global tax environment.

The Evolution of Marketplace Taxation: A Historical Chronology

To understand the current regulatory environment, one must look back at the pivotal shifts in e-commerce law over the last decade. Prior to 2018, the "physical nexus" standard, established by the 1992 Supreme Court case Quill Corp. v. North Dakota, governed sales tax collection. Under this rule, businesses were only required to collect sales tax in states where they maintained a physical presence, such as an office or warehouse.

The landscape shifted fundamentally on June 21, 2018, with the landmark decision in South Dakota v. Wayfair, Inc. The Supreme Court overturned the physical presence requirement, allowing states to mandate sales tax collection based on "economic nexus"—a threshold typically defined by a specific dollar amount of sales or a number of transactions within a state. Following this ruling, states moved rapidly to close the "tax gap" by introducing Marketplace Facilitator (MPF) laws.

By 2020, the majority of U.S. states with a general sales tax had enacted MPF legislation, shifting the legal responsibility for tax collection from individual third-party sellers to the marketplace platform itself. By 2024, the harmonization of these laws across 45 states and the District of Columbia created a standardized, albeit complex, framework that online marketplace providers must navigate today. As we move through 2026, the focus has shifted from mere adoption to rigorous enforcement and the integration of automated reporting technologies.

Defining the Modern Online Marketplace

An online marketplace is defined as a digital platform that facilitates the sale of goods or services by connecting multiple third-party sellers with buyers. While giants such as Amazon, eBay, and Etsy dominate the public consciousness, the sector has diversified into niche categories. Examples include 1stDibs for luxury furniture, RubyLane for high-end collectibles, and Ecohabitude for sustainable goods.

The value proposition for these platforms is twofold. For buyers, the marketplace acts as a curated hub that simplifies the discovery process. For sellers, the platform provides infrastructure, marketing, and a ready-made audience, allowing them to scale without the overhead of building a proprietary e-commerce site. However, this facilitation role brings the platform into the direct line of sight of state and federal tax authorities, who view the marketplace as the most efficient point of collection for tax revenue.

Strategic Options for Sales Tax Management

Marketplace providers generally face two primary paths for handling sales tax, each with distinct administrative and legal implications.

Option 1: Assuming the Role of Seller of Record

When a marketplace acts as the "Seller of Record," it assumes full responsibility for every transaction occurring on its platform. Under this model, the platform is legally viewed as the seller for tax purposes, regardless of who actually owns or ships the inventory.

This approach offers a significant competitive advantage in terms of seller recruitment. By absorbing the administrative burden of tax compliance, the platform becomes an attractive "turnkey" solution for vendors who wish to avoid the complexities of multi-state tax registration and filing. However, the internal burden on the platform is substantial. The provider must:

- Identify and monitor economic nexus thresholds in every jurisdiction.

- Register for sales tax permits in dozens of states.

- Track varying taxability rules (e.g., some states tax apparel while others do not).

- File monthly, quarterly, or annual returns and remit the collected funds to the respective revenue departments.

In the current regulatory climate, many states mandate this role via Marketplace Facilitator laws once the platform hits specific revenue targets (often $100,000 in annual sales).

Option 2: Facilitating Individual Seller Collection

The second option involves providing the technical infrastructure for third-party sellers to manage their own tax obligations. This is the model historically utilized by platforms like Shopify and eBay for their non-facilitated transactions. In this scenario, the marketplace provides a "tax engine" that calculates the correct tax at checkout based on the seller’s specific nexus profile.

The seller remains responsible for registering with state authorities and remitting the funds. While this reduces the platform’s direct liability, it necessitates a highly robust API integration to ensure that the calculations provided to the buyer are accurate. Failure to provide accurate tools can lead to seller dissatisfaction and potential legal disputes regarding the platform’s role in the transaction chain.

Supporting Data and Economic Impact

The scale of e-commerce taxation is immense. According to data from the Multistate Tax Commission (MTC), state and local governments have seen a significant increase in revenue since the widespread adoption of marketplace facilitator laws. In the fiscal year 2024, it was estimated that marketplace facilitator laws contributed over $15 billion in additional sales tax revenue across the United States.

For individual marketplace providers, the cost of non-compliance is high. Audit rates for digital platforms have increased by an estimated 22% since 2023, as states leverage sophisticated data-mining tools to identify unregistered facilitators. Penalties for failing to collect tax can range from 10% to 50% of the tax due, plus interest, which can quickly jeopardize the capital reserves of a growing startup.

Technological Integration and the Role of Automation

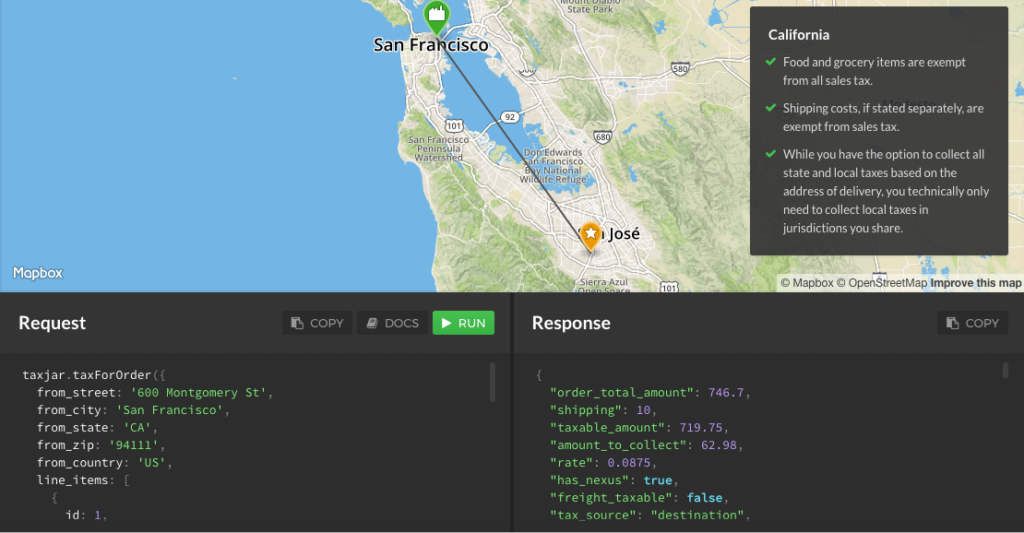

Given the thousands of tax jurisdictions in the U.S. alone, manual tax management is functionally impossible for a multi-seller marketplace. The industry has converged on the use of Application Programming Interfaces (APIs) to handle real-time tax calculations.

Tools such as the TaxJar API allow marketplace providers to automate the entire lifecycle of sales tax. When a customer adds an item to their cart, the API identifies the precise tax rate based on the buyer’s rooftop address and the specific taxability of the product category. This automation is critical for marketplaces that support diverse product types—such as a platform that sells both digital downloads (often subject to telecommunications or digital goods tax) and physical furniture (subject to traditional sales tax).

Furthermore, modern tax engines provide "multi-channel support." Because many sellers operate on several platforms simultaneously—selling on their own site, Amazon, and a niche marketplace—the tax software must be able to aggregate data from all these sources to provide a unified view of the seller’s total nexus exposure.

Official Responses and Industry Sentiment

The shift toward centralized marketplace responsibility has met with mixed reactions. Organizations like NetChoice, which represents major e-commerce players, have advocated for simplified state tax codes to reduce the "undue burden" on interstate commerce. In a 2025 policy brief, industry analysts noted that while the "Wayfair era" has stabilized, the lack of a federal standard for economic nexus thresholds continues to create friction for small to mid-sized marketplaces.

Conversely, state revenue departments have praised the marketplace facilitator model. A spokesperson for the National Association of State Tax Administrators (NASTA) recently stated that "collecting tax at the platform level is the only viable method for ensuring a level playing field between brick-and-mortar retailers and the vast, decentralized world of online commerce."

Broader Implications and Future Outlook

The implications of marketplace tax laws extend beyond mere accounting. They are shaping the very structure of the internet economy. We are seeing a "professionalization" of the seller class; as tax compliance becomes more automated and mandatory, the "casual seller" is increasingly pushed toward platforms that act as the Seller of Record to avoid personal liability.

Looking forward to the remainder of 2026 and into 2027, several trends are emerging:

- Global Harmonization: Following the U.S. model, more international jurisdictions are implementing "deemed supplier" rules, requiring marketplaces to collect Value Added Tax (VAT) or Goods and Services Tax (GST) on cross-border transactions.

- Real-Time Reporting: Several states are exploring "split-payment" systems where the sales tax portion of a transaction is diverted directly to the state treasury at the moment of sale, rather than being held by the marketplace until the filing deadline.

- Increased Scrutiny of Exemptions: Marketplaces are being held to higher standards for verifying resale certificates and tax-exempt sales, requiring more sophisticated document management features within the platform’s architecture.

For the marketplace provider, the directive is clear: tax compliance must be integrated into the product roadmap from day one. Utilizing robust APIs and staying abreast of legislative changes is no longer just a matter of "best practice"—it is a fundamental requirement for operational survival in the modern e-commerce landscape. By leveraging automation, marketplaces can transform a complex regulatory hurdle into a seamless part of the user experience, allowing them to focus on their primary goal of connecting sellers with the global market.