The hospitality sector serves as a foundational pillar of the American economy, yet for business owners within this space, the administrative complexity of maintaining a compliant payroll system remains one of the most significant operational hurdles. Unlike standard corporate environments where salaries or fixed hourly wages are the norm, restaurant payroll involves a multifaceted calculation of base pay, varying shift rates, tip reporting, and specific tax credits that require meticulous oversight. As the industry evolves toward greater transparency and digital payment systems, understanding the end-to-end process of restaurant payroll—from initial tax identification to the application of the FICA tip credit—is essential for both legal compliance and financial sustainability.

The Regulatory Framework of Restaurant Compensation

Restaurant payroll is defined as the comprehensive process of compensating staff while adhering to federal, state, and local mandates regarding wages, tips, and taxes. This cycle encompasses time tracking, tip reporting, gross-to-net calculations, and the distribution of funds. According to data from the National Restaurant Association, the industry was projected to reach $1.1 trillion in sales in 2024, employing nearly 15.5 million people. With such a massive workforce, the Department of Labor (DOL) and the Internal Revenue Service (IRS) maintain rigorous standards to ensure workers are paid fairly and taxes are remitted accurately.

The primary differentiator in this sector is the treatment of tips. Under the Fair Labor Standards Act (FLSA), tips are considered the property of the employee, yet they must be recorded as taxable income by the employer. This creates a dual responsibility: employees must report their earnings, and employers must verify those reports to calculate the correct tax withholdings. Failure to manage this accurately can result in significant penalties, back taxes, and legal action.

Chronological Implementation of a Compliant Payroll System

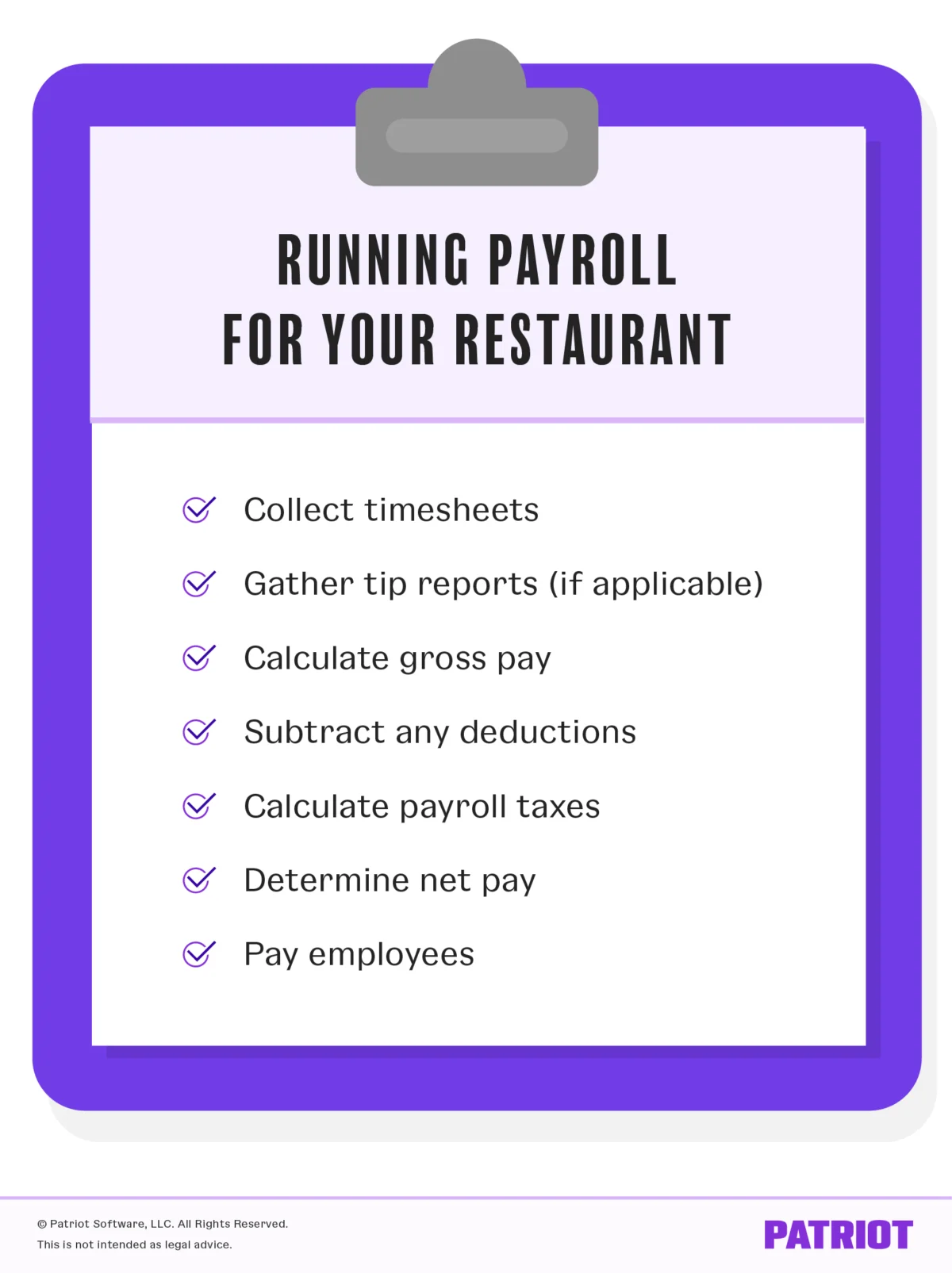

Establishing a functional payroll system requires a structured approach that begins long before the first shift is scheduled. For new establishments or those transitioning from manual to automated systems, the following chronology serves as the industry standard for setup.

Phase 1: Statutory Registration and Identification

Before any payroll can be processed, an entity must establish its legal identity with tax authorities. This begins with obtaining a Federal Employer Identification Number (EIN) from the IRS. Furthermore, state-level registration is required for State Unemployment Tax Acts (SUTA) and state income tax withholding. In many jurisdictions, local tax IDs are also necessary. Industry analysts note that delays in these registrations often lead to the "lag effect," where employees cannot be paid on time during the first month of operation, potentially leading to immediate labor disputes.

Phase 2: Employee Onboarding and Documentation

Every hire must complete a suite of federal and state documents. This includes the Form W-4 for federal income tax withholding and the Form I-9 for employment eligibility verification. In the restaurant context, additional forms are often required, such as direct deposit authorizations and agreements regarding tip-pooling arrangements. Storing these records securely is not just a best practice but a legal requirement; the IRS generally recommends keeping payroll records for at least three to four years to satisfy potential audit requirements.

Phase 3: Determining Pay Structures and Schedules

Operators must decide on a pay frequency—weekly, bi-weekly, or semi-monthly—while ensuring compliance with state-specific pay frequency laws. While some states allow for monthly payments, the majority of the hospitality industry operates on a weekly or bi-weekly schedule to accommodate the high turnover and immediate financial needs of service staff. Additionally, the method of payment (paper checks, direct deposit, or payroll cards) must be established, with careful attention paid to state laws that may prohibit mandatory direct deposit.

The Technical Mechanics of Tip Reporting and Taxation

Tip reporting is perhaps the most scrutinized aspect of restaurant accounting. The IRS requires that any employee receiving more than $20 in tips per month report those earnings to their employer. These tips are subject to Social Security, Medicare, and federal income tax withholdings.

The Role of Form 4070

Employees are technically required to report their tips by the 10th day of the month following the month the tips were received. Most modern restaurants utilize Point of Sale (POS) systems that prompt employees to enter their cash tips upon clocking out, effectively automating the collection of Form 4070 data. This integration reduces the "tax gap"—the difference between taxes owed and taxes paid—which is a high-priority area for IRS enforcement.

Service Charges vs. Gratuities

A common point of confusion in restaurant payroll is the distinction between a service charge and a tip. The IRS classifies mandatory service charges (such as a 20% automatic gratuity for large parties) as service charge wages, not tips. These funds belong to the employer initially and, when distributed to staff, are treated as regular wages subject to standard payroll taxes. They do not count toward the tip credit, a distinction that has significant implications for an employer’s bottom line.

Economic Data and the Impact of the FICA Tip Credit

One of the few tax advantages available to restaurant owners is the FICA Tip Credit, authorized under Internal Revenue Code Section 45B. This credit allows employers to claim a federal income tax credit for the portion of Social Security and Medicare taxes they pay on employee tips that exceed the federal minimum wage of $5.15 per hour (the rate in effect when the credit was established).

Data suggests that for a mid-sized restaurant with 20 tipped employees, the 45B credit can save the business thousands of dollars annually in federal income tax liability. While this credit does not change the amount of tax withheld from the employee’s check or the amount deposited during the payroll cycle, it serves as a critical offset during the year-end tax filing process.

Labor Law Compliance: Weighted Overtime and Tip Credits

The legal landscape for restaurant wages is currently in a state of flux as many states move to abolish or significantly alter the "tip credit."

Understanding the Tip Credit Floor

Under federal law, the maximum tip credit an employer can claim is $5.12 per hour, meaning they can pay a "cash wage" of as little as $2.13 per hour, provided the employee’s tips bring their total hourly earnings up to the federal minimum wage of $7.25. However, several states, including California, Oregon, and Washington, have eliminated the tip credit entirely, requiring employers to pay the full state minimum wage regardless of tips earned.

The Weighted Average Overtime Calculation

In environments where employees perform multiple roles at different pay rates—such as a staff member who works as a server at $5.00/hour and a trainer at $15.00/hour—calculating overtime becomes complex. The DOL requires the use of the weighted-average method. To calculate this, the employer must:

- Calculate the total earnings from all hours worked.

- Divide the total earnings by the total hours worked to find the "weighted average" rate.

- Multiply that weighted average by 0.5 for all hours worked over 40.

This ensures that employees are compensated fairly based on their total contribution throughout the workweek, rather than just their base server rate.

Industry Reactions and the Shift Toward Automation

The reaction from the restaurant community to these complex requirements has been a rapid shift toward specialized payroll software. Traditional, general-purpose payroll providers often struggle with the nuances of tip credits and weighted overtime. Consequently, a sub-sector of the fintech industry has emerged to provide restaurant-specific solutions that integrate directly with POS systems and time-tracking hardware.

"Manual payroll is no longer viable for a restaurant looking to scale," says industry analyst Mark Henderson. "Between the risk of a DOL audit and the administrative time lost to calculating weighted overtime, the ROI on specialized software is almost immediate."

The rise of "on-demand pay" or "earned wage access" is another trend gaining traction. This allows restaurant workers to access a portion of their earned wages and tips immediately after a shift, rather than waiting for a two-week pay cycle. While popular with employees, this requires sophisticated backend payroll synchronization to ensure that taxes are still withheld accurately before the final disbursement.

Broader Implications for the Hospitality Industry

The complexities of restaurant payroll reflect a broader shift in the American labor market toward increased regulation and worker protection. As more municipalities implement "Fair Workweek" laws—which require predictable scheduling and premium pay for last-minute changes—the payroll process will only become more integrated with operations.

Furthermore, the potential for a federal increase in the minimum wage or the elimination of the federal tip credit remains a central point of debate in Washington. Should the tip credit be abolished at the federal level, restaurant owners would face a significant increase in labor costs, likely leading to a fundamental shift in the American dining model, potentially moving toward higher menu prices or service-inclusive pricing.

In conclusion, running a restaurant payroll is a high-stakes balancing act between financial management and legal compliance. By following a rigorous chronology of setup, leveraging tax credits like Section 45B, and utilizing modern technological integrations, operators can mitigate the risks associated with this complex administrative burden. As the industry continues to navigate post-pandemic labor shortages and evolving tax laws, the ability to execute a precise, compliant, and transparent payroll system remains a definitive characteristic of a successful hospitality enterprise.