Accounting, taxes, and comprehensive financial planning represent a formidable challenge for many small business owners. While modern accounting software offers invaluable tools to streamline basic responsibilities, there inevitably comes a juncture where the complexities demand the nuanced expertise and strategic guidance of a professional accountant. This transition from managing finances independently to seeking external support is not merely about delegating tasks, but often signifies a crucial step in a business’s maturation and a proactive measure to safeguard its long-term financial health.

The Unavoidable Truth: Financial Complexity for Small Businesses

The landscape of small business finance is increasingly intricate. Beyond the fundamental recording of transactions, owners must contend with evolving tax codes at federal, state, and local levels, navigate compliance with various regulatory bodies, make informed investment decisions, and strategically plan for growth. For entrepreneurs whose primary expertise lies in their core business operations, dedicating sufficient time and acquiring the specialized knowledge required for meticulous financial management can become an overwhelming burden. Studies consistently indicate that financial mismanagement, often stemming from a lack of expert oversight, is a significant contributor to small business failures. Engaging an accounting professional, therefore, is not a luxury but a strategic imperative that can provide clarity, ensure compliance, and unlock opportunities for sustained profitability.

Key Indicators: When Professional Help Becomes Imperative

While the decision to hire an accountant may seem subjective, several distinct triggers and developmental stages within a business’s lifecycle unequivocally signal the need for expert intervention. Recognizing these signs early can prevent costly errors and position the business for greater success.

I. Launching Your Venture: The Foundation of Financial Health

The genesis of a new business is a period rife with critical decisions that will fundamentally shape its future. From selecting the optimal legal structure—whether a sole proprietorship, partnership, LLC, S-Corp, or C-Corp—to securing initial financing and establishing robust financial systems, the choices made at this stage carry significant weight. An accountant’s early involvement can be transformative. They can offer invaluable guidance on:

- Business Structure Optimization: Advising on the most tax-efficient and legally sound entity type, considering liability, ownership, and future growth aspirations.

- Compliance and Registration: Ensuring adherence to federal, state, and local registration requirements, including obtaining necessary Employer Identification Numbers (EINs), sales tax permits, and industry-specific licenses.

- Financial Projections and Business Plans: Collaborating on the creation of a compelling business plan that includes accurate financial forecasts, critical for attracting investors or securing loans.

- Initial Accounting Setup: Establishing a proper chart of accounts, implementing suitable accounting software, and setting up efficient bookkeeping processes from day one.

- Funding Strategy: Assisting in understanding the financial implications of different funding sources and preparing financial statements required by lenders or investors.

Without professional guidance at this nascent stage, new businesses risk selecting suboptimal structures, missing crucial registrations, or failing to establish sound financial foundations, which can lead to compliance issues, operational inefficiencies, and stunted growth.

II. Scaling Operations: Managing the Dynamics of Growth

A business experiencing rapid or even steady growth, while exciting, often introduces a new layer of financial complexity. Increased sales typically mean more transactions, higher expenses, potential expansion into new markets, and possibly a growing workforce. This period demands sophisticated financial oversight to ensure that growth is sustainable and profitable, not merely a precursor to overextension. An accountant becomes a vital strategic partner by:

- Cash Flow Management: Monitoring and forecasting cash flow to ensure liquidity, especially during periods of significant investment or seasonal fluctuations.

- Budgeting and Cost Control: Developing realistic budgets, identifying areas for cost reduction, and analyzing spending patterns to optimize profitability.

- Investment Analysis: Evaluating the financial viability of new investments, whether in equipment, technology, or additional personnel, projecting returns, and cautioning against financially unsound ventures.

- Performance Monitoring: Tracking key performance indicators (KPIs) and providing regular financial reports that offer actionable insights into the business’s health and trajectory.

- Strategic Planning: Assisting in updating the business plan to reflect new objectives, market conditions, and financial realities, ensuring that growth is aligned with long-term goals.

Without this expertise, a growing business might "fly too close to the sun," expanding too quickly, mismanaging increased revenue, or making regrettable investments that undermine its future stability.

III. Deciphering the Tax Code: A Labyrinth of Regulations

For many small business owners, the sheer complexity of business taxes is a primary driver for seeking professional help. The U.S. tax code is notoriously intricate, with constant updates and nuances that can be challenging for non-specialists to navigate. Mistakes can result in severe IRS penalties, while a lack of knowledge can lead to missed opportunities for legitimate tax deductions and credits. An accountant’s role in tax management is multifaceted:

- Tax Planning: Proactive strategies throughout the year to minimize tax liability legally, including advice on retirement plans, asset depreciation, and business expenses.

- Accurate Tax Preparation: Ensuring all federal, state, and local tax returns are completed accurately and filed on time, utilizing current tax laws and regulations.

- Identifying Deductions and Credits: Leveraging their knowledge to identify every eligible deduction and credit, which can significantly reduce a business’s tax burden.

- Structure-Specific Guidance: Providing tailored advice based on the business’s legal structure, as tax obligations vary significantly between sole proprietorships, partnerships, S-Corps, and C-Corps.

- Representation: In the event of an audit or inquiry from tax authorities, a qualified accountant (CPA or Enrolled Agent) can represent the business and communicate directly with the IRS.

The cost of a tax professional is often outweighed by the savings from avoided penalties and maximized legitimate deductions, not to mention the invaluable peace of mind.

IV. The Burden of Compliance Forms: Beyond the Basic Tax Return

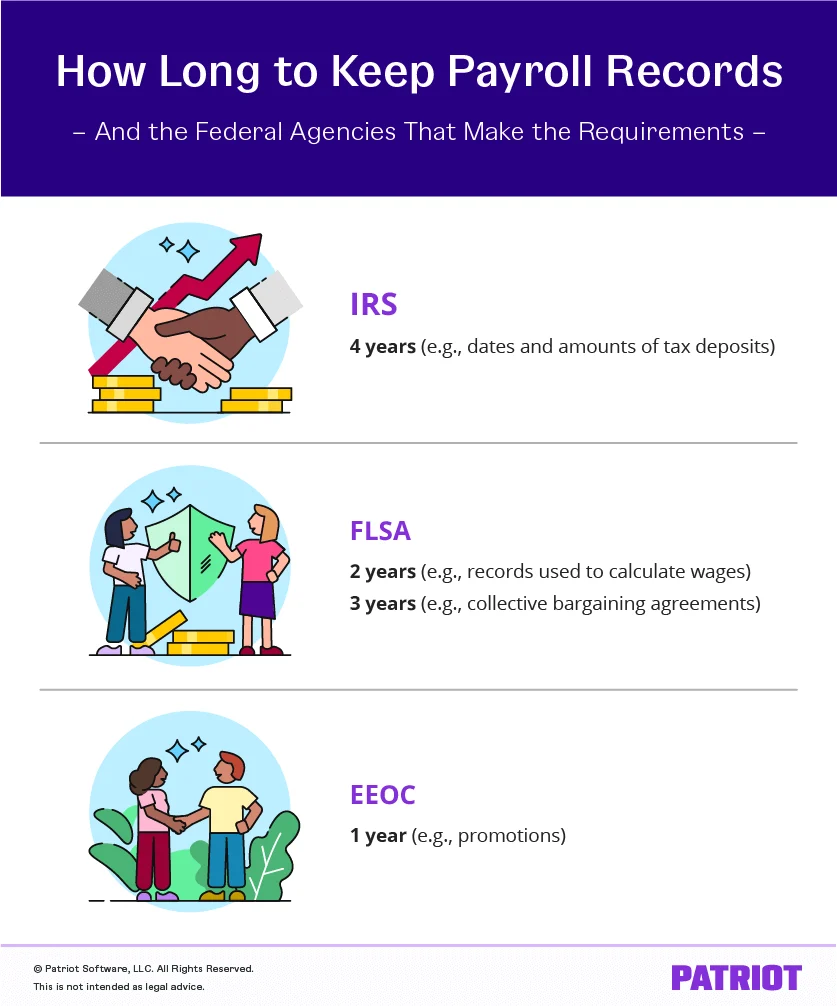

Beyond the annual income tax return, businesses, especially those with employees, face a constant stream of compliance-related paperwork. These forms are critical for reporting payroll taxes, sales taxes, and other regulatory obligations to various government agencies. The administrative burden can be substantial, and errors or missed deadlines carry their own set of penalties. An accountant can assist with:

- Payroll Tax Filings: Preparing and submitting forms like Form 941 (Employer’s Quarterly Federal Tax Return), Forms W-2 (Wage and Tax Statement), and Forms W-3 (Transmittal of Wage and Tax Statements).

- Contractor Reporting: Managing Form 1099-NEC (Nonemployee Compensation) for independent contractors.

- Sales Tax Returns: Ensuring accurate calculation and timely remittance of sales tax to state and local authorities, which can vary significantly by jurisdiction and product/service.

- State Unemployment and Local Business Taxes: Handling specific state unemployment insurance filings and any unique local business taxes.

- Industry-Specific Reporting: Navigating any specialized reporting requirements pertinent to a particular industry.

While full-service payroll software can automate some of these tasks, an accountant provides the oversight and strategic advice to ensure that the underlying data is correct and that the business remains fully compliant across all reporting fronts.

V. Facing an Audit: Navigating Regulatory Scrutiny

The prospect of an IRS or state audit can be a source of immense stress for any business owner. An audit signifies a thorough examination of a business’s financial records to verify accuracy and compliance. Without proper preparation and representation, an audit can be a daunting and potentially costly ordeal. An accountant plays a critical role in:

- Pre-Audit Review: Proactively reviewing financial records, reconciling accounts, and identifying potential discrepancies or missing information that could trigger an audit.

- Record Preparation: Organizing and presenting financial documentation in a clear, coherent manner, making the audit process smoother.

- Representation: Serving as the primary point of contact with auditors, answering questions, providing explanations, and advocating on behalf of the business. Certified Public Accountants (CPAs), Enrolled Agents (EAs), and tax attorneys are authorized to represent taxpayers before the IRS.

- Mitigation: Helping to resolve any identified discrepancies, negotiate settlements, and minimize potential penalties.

Having a qualified professional in your corner during an audit can significantly alleviate stress, protect your business’s interests, and ensure a more favorable outcome.

Beyond Reactive: The Strategic Value of Proactive Accounting

While the "red flags" mentioned above are compelling reasons to seek professional help, the value of an accountant extends far beyond crisis management or compliance. Proactive engagement with an accounting professional can transform a business’s financial trajectory, offering strategic insights that drive growth and efficiency. This approach considers the opportunity cost of an owner’s time—if a business owner bills at $150 per hour and spends five hours a week grappling with books and taxes, that equates to over $3,000 per month in "time tax" that could be redirected towards revenue-generating activities. An accountant can:

- Provide Objective Financial Analysis: Offering an unbiased perspective on financial performance, identifying trends, and flagging potential issues before they escalate.

- Facilitate Strategic Planning: Collaborating on long-term financial goals, succession planning, and expansion strategies.

- Improve Decision-Making: Providing clear, accurate financial reports that empower owners to make informed strategic and operational decisions.

- Enhance Operational Efficiency: Identifying inefficiencies in financial processes and suggesting improvements.

- Offer Peace of Mind: Reducing the mental burden and stress associated with complex financial management, allowing owners to focus on their core competencies.

Choosing Your Financial Partner: Models of Engagement

Small businesses have several options when it comes to managing their accounting needs, each with its own advantages and disadvantages:

- DIY (Do-It-Yourself): Suitable for very small businesses with simple transactions and owners who have the time and inclination to learn accounting basics. This often involves using basic accounting software.

- Hybrid Approach: The most common and often recommended model. Business owners utilize accounting software for daily tasks (invoicing, expense tracking, bank feeds) and then engage an accountant for monthly or quarterly reconciliations, strategic reviews, and year-end tax preparation. This balances cost-effectiveness with professional oversight.

- Full Outsourcing: Delegating all accounting functions, from daily bookkeeping to advanced financial analysis and tax planning, to an external accounting firm or professional. This is ideal for businesses that prefer to completely offload financial management.

- In-House Accountant: Hiring a full-time employee dedicated to accounting. This is typically reserved for larger small businesses or those with highly complex, continuous financial needs.

The best model depends on the business’s size, complexity, budget, and the owner’s comfort level with financial tasks.

Investing in Expertise: Cost and Return on Investment

The cost of accounting services varies significantly based on location, the complexity of the business, the volume of transactions, and the scope of services required.

- Accounting Software: Often ranges from $0 to $50+ per month for basic to advanced features.

- Outsourced Bookkeeping/Accounting Packages: Can range from $300 to $1,000+ per month for comprehensive services, including monthly reconciliations, financial statements, and some tax preparation.

- Hourly Rates for Consulting/Tax Prep: Typically range from $60 to $400+ per hour, with CPAs and specialized consultants commanding higher rates.

- Full-Time In-House Accountant: Generally requires an annual salary exceeding $60,000 to $80,000+, plus benefits.

It is crucial to view accounting fees not as an expense, but as an investment. Professional fees are often tax-deductible, and the return on investment (ROI) can be substantial. An accountant can save money by:

- Avoiding Penalties: Preventing costly fines for late or incorrect filings.

- Maximizing Deductions and Credits: Identifying opportunities that owners might miss, directly reducing tax liability.

- Improving Cash Flow: Through better financial management and forecasting.

- Strategic Growth: Providing insights that lead to more profitable decisions and business expansion.

- Time Savings: Freeing up the owner’s valuable time to focus on core business operations and revenue generation.

Many businesses find that the financial benefits and peace of mind derived from professional accounting services far outweigh the associated costs.

The Search for the Right Professional

Finding the ideal accountant for your small business requires a systematic approach.

1. Defining Your Needs:

Before beginning your search, clearly articulate what you expect from an accountant.

- Do you need daily bookkeeping, or just periodic reviews?

- Are you seeking tax preparation only, or also strategic financial planning?

- Do you require assistance with payroll, sales tax, or audit representation?

- What is your budget for these services?

- Do you prefer an individual practitioner or a larger firm?

Understanding your specific requirements will help narrow your search and ensure you find a professional with the right expertise.

2. Where to Look: Beginning Your Search:

- Referrals: Word-of-mouth recommendations from trusted local small business owners are often the most reliable source. Your local Chamber of Commerce or other business networking groups can also provide excellent leads.

- Professional Directories: The American Institute of Certified Public Accountants (AICPA) offers a directory of CPAs. State CPA societies and national associations for Enrolled Agents also maintain searchable databases.

- Online Platforms: Websites specializing in connecting businesses with accounting professionals can offer a wide range of options, including virtual accountants.

- Other Professionals: Your business attorney or financial advisor may have recommendations for reputable accountants they frequently collaborate with.

3. The Interview Process: Choosing an Accountant:

Once you have a shortlist, schedule interviews to assess compatibility and expertise. It is advisable to meet face-to-face (or via video conference) to discuss your business and its specific needs. Key questions to ask include:

- Experience with Small Businesses and Your Industry: How often do you work with small businesses, especially those in my specific industry or with my business structure (e.g., sole proprietorship, LLC)?

- Scope of Services: What specific accounting tasks can you help me with? Do you offer bookkeeping, tax preparation, payroll, financial consulting, and audit support?

- Availability and Communication: How accessible will you be? Will I work directly with you or a team member? What is your typical response time for inquiries? Do you offer on-site visits if needed?

- Fee Structure: What are your fees and charges? Do you charge hourly, a monthly retainer, or project-based fees? Can you provide a detailed quote for the services I need?

- Technology Proficiency: What accounting software do you use or recommend? Are you proficient with my current software (e.g., Patriot Accounting, QuickBooks, Xero)? How do you handle data exchange?

- Client References: Can you provide references from other small business clients?

- Proactive Engagement: What insights or questions do you have about my business after our discussion? (A lack of questions might be a red flag, indicating less engagement).

Preparing for Collaboration: A Checklist

Before your initial meeting with a prospective accountant, gather the following documents and information to facilitate a productive discussion:

- Business formation documents (e.g., Articles of Incorporation/Organization)

- Previous two to three years of tax returns (business and personal)

- Recent financial statements (Profit & Loss, Balance Sheet)

- Bank and credit card statements

- Payroll reports (if applicable)

- Sales tax filings (if applicable)

- Access to your current accounting and payroll software

- A summary of your business goals and current financial challenges

Finding Your Small Business Accountant

Whether your business requires daily bookkeeping, periodic financial reviews, strategic tax planning, or robust audit representation, securing the right accounting professional is fundamental to maintaining financial health and fostering sustainable growth. By taking the time to define your needs, research potential candidates, and conduct thorough interviews, you can identify a trusted advisor who will not only manage your financial obligations but also provide invaluable insights that empower your company to thrive. This strategic partnership is an investment in clarity, compliance, and ultimately, the enduring success of your entrepreneurial journey.

FAQs

Can I do my own accounting?

Yes, for very simple businesses with minimal transactions, an owner can manage their own accounting, especially with user-friendly software. However, it requires a significant time commitment, continuous learning of tax laws, and meticulous record-keeping. Most owners eventually find that the complexity and time required warrant professional assistance, particularly for tax preparation and strategic planning.

How much does an accountant cost?

Costs vary widely. Basic accounting software can be $0-$50+ monthly. Outsourced bookkeeping packages typically range from $300-$1,000+ per month. Hourly rates for tax preparation or consulting can be $60-$400+ per hour, depending on the professional’s credentials and experience. Full-time in-house accountants command salaries often exceeding $60,000 annually. Importantly, professional fees are generally tax-deductible.

When should I hire an accountant versus a bookkeeper?

Bookkeepers manage day-to-day financial records, process transactions, reconcile accounts, and often handle basic payroll. Accountants (especially CPAs) offer higher-level services: financial analysis, tax planning, strategic advice, audit representation, and more complex reporting. Many businesses benefit from a hybrid approach, using a bookkeeper for daily tasks and an accountant for periodic reviews, tax strategy, and advanced consulting.

Do I need a CPA for taxes?

Not always. For very straightforward returns, a non-CPA tax preparer might suffice. However, for complex business returns, strategic tax planning, or if you anticipate or face an audit, a Certified Public Accountant (CPA) or an Enrolled Agent (EA) is highly recommended. These professionals have specialized credentials, extensive knowledge of tax law, and the authority to represent you before the IRS.

What documents should I prepare before hiring an accountant?

Before your first meeting, gather your business formation documents, prior year tax returns (business and personal), recent financial statements (Profit & Loss, Balance Sheet), bank and credit card statements, payroll reports, sales tax filings, and access details for your current accounting and payroll software.

Will hiring an accountant save me money?

Often, yes. Accountants help businesses save money by identifying eligible tax deductions and credits, preventing costly IRS penalties due to errors or late filings, improving cash flow management, and providing strategic advice that leads to more profitable business decisions. The time saved by delegating financial tasks also allows owners to focus on revenue-generating activities.

What is a good hybrid setup for small business accounting?

A common and effective hybrid setup involves using accounting software (like Patriot Accounting) for daily tasks such as invoicing, expense tracking, and connecting bank feeds. You then perform monthly reconciliations yourself or with a bookkeeper. An accountant is engaged quarterly for financial reviews and strategic advice, and annually for comprehensive tax preparation and planning. This approach balances cost efficiency with expert oversight.