The transition to remote work has evolved from an emergency response during the 2020 global pandemic into a permanent structural shift in the American labor market. As of late 2023, data from the U.S. Census Bureau and the Bureau of Labor Statistics indicate that approximately 20% of the workforce continues to work remotely full-time, while an additional 12% engage in hybrid arrangements. While this shift has offered businesses access to a broader talent pool and reduced overhead costs, it has simultaneously created a labyrinth of payroll compliance and tax obligations. For employers, paying a remote worker is no longer as simple as issuing a check from a centralized headquarters; it requires a granular understanding of state-specific labor laws, "nexus" established by the employee’s physical presence, and complex tax reciprocity agreements.

The Evolution of Remote Work Regulation: A Chronology

To understand the current complexity of remote payroll, one must examine the timeline of its regulatory development. Prior to 2020, remote work was largely a niche benefit offered by tech firms or specialized consultancies. The regulatory framework was static, assuming most employees worked in the same jurisdiction as their employer’s physical office.

In March 2020, the sudden shift to work-from-home (WFH) prompted many state tax authorities to issue temporary "nexus relief" provisions. These guidelines allowed businesses to continue withholding taxes based on the employer’s location rather than the employee’s new home office to avoid administrative chaos. However, by 2021 and 2022, as remote work solidified into a permanent fixture, states began rescinding these temporary measures.

By 2023, the regulatory environment transitioned into a "permanent enforcement" phase. States like New York and Massachusetts reinforced "convenience of the employer" rules, which dictate that if an employee works remotely for their own convenience rather than the employer’s necessity, they may still owe taxes to the state where the office is located. Simultaneously, other states have aggressively pursued payroll tax revenue from remote workers residing within their borders, creating a high-stakes environment for corporate compliance departments.

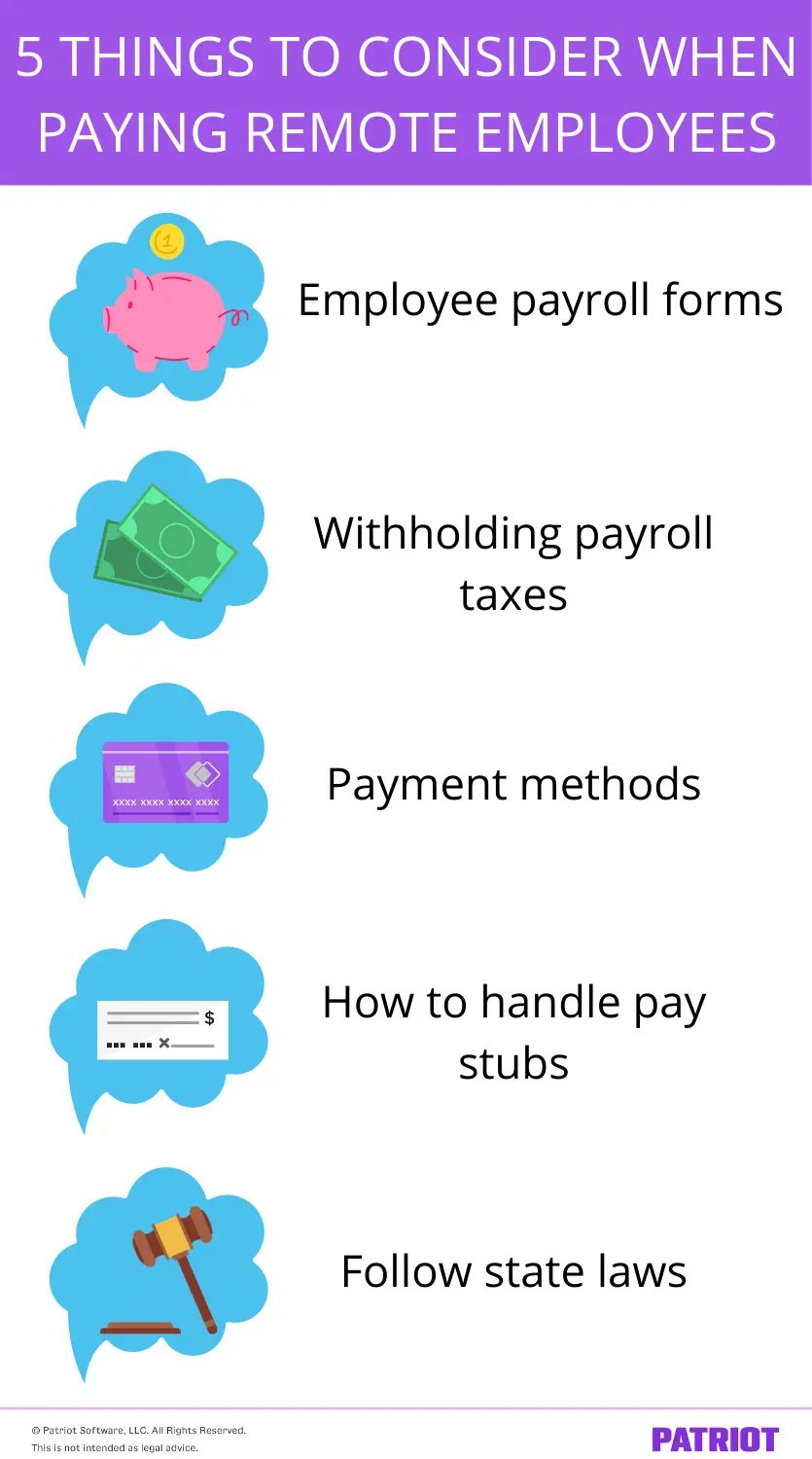

Establishing the Administrative Foundation: Essential Documentation

The first pillar of paying remote employees is the rigorous management of payroll forms. Federal law mandates that certain documents be maintained for every worker, regardless of their physical location. The Form I-9 (Employment Eligibility Verification) remains a critical requirement, though the Department of Labor and U.S. Citizenship and Immigration Services (USCIS) have modernized these requirements. As of August 2023, eligible employers who use E-Verify may now conduct remote document inspections, a significant departure from the previous requirement for in-person verification.

In addition to federal requirements, employers must secure state-specific versions of the Form W-4. If an employee resides in a state different from the business’s physical headquarters, the employer is generally required to withhold income tax for the state where the work is actually performed. This necessitates a thorough audit of the employee’s primary residence and the establishment of a "work situs."

Furthermore, record-keeping remains a legal imperative. The Fair Labor Standards Act (FLSA) requires employers to keep payroll records for at least three years. For remote teams, digital employee portals have transitioned from a luxury to a necessity, ensuring that password-protected documents and sensitive personal information are handled with the level of security required by modern data privacy laws.

The Complexity of Multi-State Taxation and Nexus

The most significant challenge in remote compensation is the concept of "tax nexus." When an employee works from home in a different state, they often create a physical presence for the business in that state. This "nexus" can trigger not only payroll tax withholding obligations but also state unemployment insurance (SUI) liabilities and, in some cases, corporate income tax obligations.

Reciprocity Agreements

Fortunately, some states have entered into tax reciprocity agreements. For example, an employee living in Virginia but working for a company in Maryland may be exempt from Maryland withholding if they file the appropriate exemption forms. These agreements are designed to prevent "double taxation" and simplify the filing process for employees who cross state lines for work. Currently, 16 states and the District of Columbia have some form of reciprocity agreement in place, largely concentrated in the Midwest and Northeast.

State Unemployment Insurance (SUI)

Employers must also register with the unemployment agency in the state where the remote employee resides. Unlike federal unemployment tax (FUTA), which is uniform, SUI rates vary significantly by state and are influenced by the employer’s "experience rating." Failure to register and pay into the correct state fund can result in substantial back-tax assessments and penalties.

Local and Municipal Taxes

Beyond state-level obligations, certain jurisdictions impose local income or occupational taxes. Cities such as Philadelphia, Pittsburgh, and various municipalities in Ohio and Kentucky require specific local withholdings based on where the work is performed. For a remote employer, this necessitates a ZIP-code-level analysis of every employee’s home office.

Modernizing Payment Methods and Pay Stub Compliance

As the workforce becomes more geographically dispersed, the logistics of distributing pay have shifted toward digital-first solutions. While the paper check remains a legal option, the administrative burden of mailing checks across state lines—and the risk of mail delays—has made direct deposit the industry standard.

According to the 2023 "Getting Paid in America" survey by the American Payroll Association, more than 95% of U.S. employees receive their pay via direct deposit. For the unbanked or underbanked segments of the remote workforce, payroll cards and mobile wallets have emerged as viable alternatives. However, employers must be wary of state-specific "pay card laws." For instance, states like New York and California require that employees be given a choice of payment methods and that they have access to at least one method that does not incur fees for withdrawing their full net pay.

Pay stub delivery is another area of regulatory divergence. While federal law does not strictly mandate the provision of pay stubs, most states do. Some states, such as California and Texas, have "opt-out" or "opt-in" laws regarding electronic pay stubs. Employers must ensure that their digital portals provide employees with a printable version of their pay details, including gross wages, deductions, and net pay, to remain compliant with state transparency laws.

Classification and the "Economic Reality" Test

A recurring trap for businesses managing remote teams is the misclassification of workers as independent contractors (1099) rather than employees (W-2). The Department of Labor (DOL) issued a new final rule in early 2024, reinstating the "economic reality" test. This test evaluates the degree of control the employer exerts over the worker, the worker’s opportunity for profit or loss, and the permanency of the relationship.

Remote workers are frequently misclassified because they use their own equipment or set their own hours. However, if the business dictates the specific tasks, provides the software used for work, and the work is integral to the business, the DOL likely views that worker as an employee. Misclassification can lead to devastating financial consequences, including unpaid overtime claims, back taxes, and significant liquidated damages.

Expense Reimbursements and the Cost of the "Home Office"

One of the most debated aspects of remote work compensation is the reimbursement of business expenses. Under the FLSA, employers are generally not required to reimburse employees for work-related expenses unless those expenses cause the employee’s pay to drop below the federal minimum wage.

However, several states have implemented much stricter mandates. California Labor Code Section 2802 requires employers to reimburse employees for all "necessary expenditures or losses incurred" in direct consequence of their duties. This has been interpreted by courts to include a reasonable portion of an employee’s personal cell phone and internet bills if they are required to work from home. Illinois and Massachusetts have similar statutes. For companies with a national remote workforce, the most prudent strategy is often a standardized monthly "technology stipend" to ensure compliance across all jurisdictions.

Implications for Corporate Strategy and Talent Acquisition

The administrative complexity of paying remote employees has led to a strategic re-evaluation of hiring practices. Some mid-sized firms have begun limiting their remote hiring to specific "approved states" where they already have an established tax nexus. This reduces the burden of registering with dozens of different state tax agencies.

Conversely, larger enterprises are viewing the "compliance tax" as a necessary cost of acquiring top-tier talent. The emergence of "Employer of Record" (EOR) services has also surged, allowing companies to hire remote workers in states or countries where they lack a legal entity by using a third party to handle all payroll, tax, and compliance obligations.

Conclusion: The Path Forward for Employers

The era of remote work has fundamentally altered the relationship between geography and compensation. For businesses to thrive in this environment, they must move beyond a "headquarters-centric" mindset and adopt a "jurisdiction-aware" payroll strategy. This involves:

- Continuous Monitoring: Regularly auditing employee residences to detect undisclosed moves across state lines.

- Technological Integration: Utilizing payroll software that automatically updates for state and local tax changes.

- Expert Consultation: Engaging with tax professionals who specialize in multi-state nexus issues.

While the burden of compliance is high, the data suggests that the flexibility of remote work remains a primary driver of employee retention and satisfaction in the modern economy. By mastering the nuances of remote payroll, businesses can mitigate legal risks while maintaining a competitive edge in the global hunt for talent.