The landscape of American commerce is inextricably linked to a complex web of state and local tax obligations, with forty-five states and the District of Columbia currently enforcing some form of sales tax. As the United States moves toward the 2026 fiscal year, business owners face an increasingly granular regulatory environment characterized by varying rates, shifting nexus thresholds, and distinct rules for online versus brick-and-mortar transactions. Staying compliant requires more than a passing familiarity with local rates; it demands a deep understanding of the legal frameworks that govern how tax is collected, reported, and remitted across disparate jurisdictions.

The Evolution of Sales Tax: From Physical Presence to Economic Nexus

The modern era of sales tax compliance was fundamentally reshaped by the 2018 U.S. Supreme Court decision in South Dakota v. Wayfair, Inc. Before this landmark ruling, states were generally prohibited from requiring out-of-state retailers to collect sales tax unless the business had a physical presence, such as a warehouse or office, within the state. The Wayfair decision overturned this "physical presence" standard, clearing the way for "economic nexus" laws.

Under economic nexus, a business is required to collect and remit sales tax once it exceeds a specific threshold of sales revenue or transaction volume within a state, regardless of physical location. By 2026, nearly every state with a sales tax has adopted these rules, typically setting the bar at $100,000 in annual sales or 200 individual transactions. This shift has created a significant administrative burden for small and medium-sized enterprises (SMEs), necessitating the use of sophisticated accounting software to track multi-state obligations in real-time.

Deciphering the Lexicon of Tax Compliance

To navigate state-specific mandates, business owners must first master the terminology that defines their legal obligations. Sales tax is structurally a "pass-through" tax; while the customer pays the tax at the point of sale, the business acts as the state’s collection agent. Failure to collect the correct amount does not absolve the business of the debt; rather, the business becomes liable for the unpaid tax during an audit.

Defining Nexus and Economic Thresholds

Nexus is the legal term for the "connection" between a business and a taxing jurisdiction. Physical nexus is triggered by tangible factors such as owning property, employing staff, or storing inventory in a third-party fulfillment center. Conversely, economic nexus is strictly a numbers game based on revenue generated from residents of that state.

Sourcing Methods: Origin vs. Destination

A critical distinction in tax law is the "sourcing" method used to determine which rate applies. In "origin-based" states, the tax rate is determined by where the seller is located. In "destination-based" states, the rate is determined by where the buyer receives the product. As of 2026, the majority of states have moved toward destination-based sourcing to ensure that local jurisdictions receive the tax revenue generated by their residents’ consumption.

Use Tax and Gross Receipts Tax

While sales tax is collected by the seller, "use tax" is a self-reported tax paid by the consumer when sales tax was not collected at the time of purchase. Additionally, some states eschew traditional sales tax for alternative models. Hawaii utilizes a General Excise Tax (GET), which is levied on all business activities, while New Mexico employs a Gross Receipts Tax (GRT).

The State-by-State Regulatory Framework

The following breakdown details the specific compliance requirements and nexus triggers for states maintaining sales tax systems as of 2026.

The Southeastern Corridor: Alabama to Florida

Alabama maintains a dual system of state and local taxes, with nexus triggered by physical presence or exceeding economic thresholds. The state offers exemptions for essentials like prescription drugs. Florida, a destination-based state, has historically relied heavily on sales tax revenue due to its lack of state income tax. Florida nexus is triggered by physical presence, including the use of traveling sales representatives or the storage of goods in-state.

The Mid-Atlantic and Northeast: New York to Massachusetts

New York operates as a destination-based state, requiring businesses to calculate rates based on the specific delivery address, which may include state, county, and city layers. In contrast, Connecticut and Massachusetts offer a more streamlined approach by maintaining statewide rates without additional local sales taxes. New Jersey remains a strictly destination-based state with a base rate of 6.625%, exempting most grocery items and clothing to alleviate the tax burden on residents.

The Midwest: Ohio, Illinois, and Michigan

The Midwest presents a mixture of sourcing philosophies. Ohio and Illinois utilize origin-based sourcing for in-state sellers, meaning a business in Chicago or Columbus charges the rate applicable to its storefront location regardless of where the customer lives within the state. However, for remote sellers, these states often shift to destination-based rules. Michigan maintains a flat 6% state rate with no local add-ons, simplifying compliance for retailers.

The Western Frontier: California to Washington

California is unique for its "hybrid-origin" sourcing model. While the state base rate is 7.25%, district taxes vary wildly, often requiring sellers to use a mixture of origin and destination logic depending on the transaction type. Washington State, a destination-based jurisdiction, has been a leader in marketplace facilitator laws, requiring platforms like Amazon and eBay to collect tax on behalf of third-party sellers.

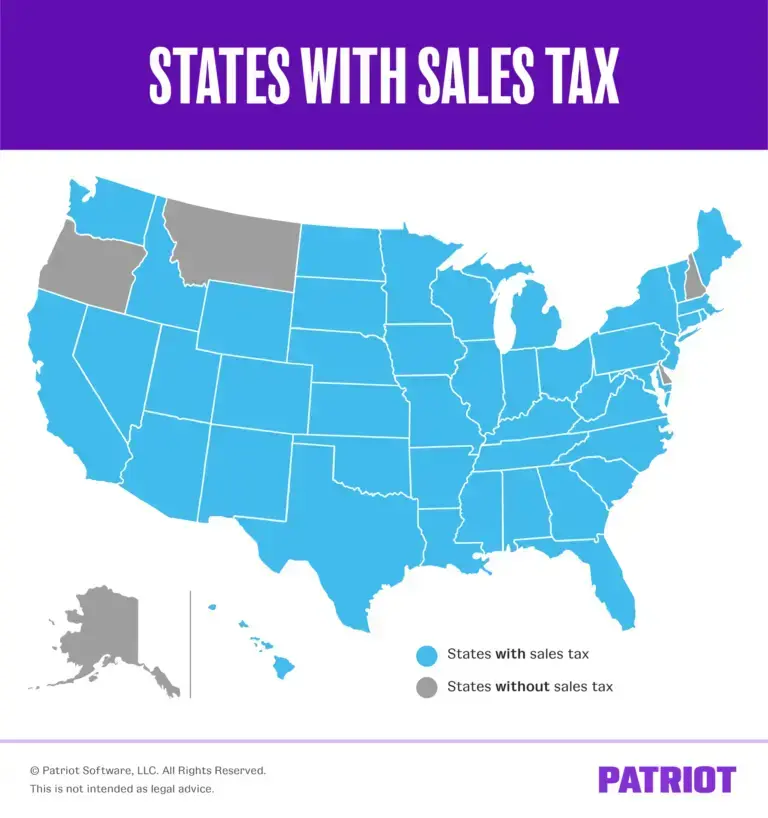

States Without General Sales Tax: The "NOMAD" Group

Five states—New Hampshire, Oregon, Montana, Alaska, and Delaware—do not impose a statewide sales tax. Often referred to by the acronym NOMAD, these states are frequent hubs for distribution centers. However, business owners should not assume a total lack of tax liability. For example, Alaska allows local municipalities to levy their own sales taxes, and Montana permits "resort taxes" in specific tourist-heavy areas.

2026 Statistical Overview and Sourcing Data

The following table outlines the projected base rates and sourcing methods for the 2026 fiscal year. These figures represent the foundation of the tax calculation, though local jurisdictions may add significant percentages.

| State | 2026 Base Rate | Local Range | Sourcing Method |

|---|---|---|---|

| Alabama | 4.00% | 0.10% – 7.50% | Destination |

| Arizona | 5.60% | 0.00% – 5.60% | Origin |

| California | 7.25% | 0.10% – 3.00% | Hybrid |

| Colorado | 2.90% | 0.00% – 8.30% | Destination |

| Illinois | 6.25% | 0.00% – 4.75% | Origin |

| Indiana | 7.00% | N/A | Destination |

| Louisiana | 5.00% | 0.00% – 8.50% | Destination |

| New York | 4.00% | 0.00% – 4.875% | Destination |

| Ohio | 5.75% | 0.00% – 2.25% | Origin |

| Texas | 6.25% | 0.00% – 2.00% | Origin |

| Washington | 6.50% | 0.00% – 3.90% | Destination |

Industry Reactions and Economic Implications

Tax experts and small business advocacy groups have voiced concerns over the growing complexity of these regulations. The National Federation of Independent Business (NFIB) has frequently highlighted that the cost of compliance—investing in software, hiring tax consultants, and managing audits—disproportionately affects smaller retailers who lack the administrative infrastructure of large corporations.

"The move toward destination-based sourcing and economic nexus has essentially forced every small e-commerce shop to become an expert in the tax codes of 45 different states," notes one senior tax analyst. "While this has been a windfall for state treasuries, it creates a significant barrier to entry for new entrepreneurs."

Conversely, state revenue departments argue that these laws are essential for maintaining a level playing field. Before the Wayfair decision, local brick-and-mortar stores were at a competitive disadvantage against out-of-state online retailers who did not have to charge sales tax. The current framework ensures that all sellers contributing to a state’s economy also contribute to its public services.

Analysis: The Future of Tax Automation

As we move further into 2026, the trend toward automation in tax compliance is expected to accelerate. Many states have joined the Streamlined Sales and Use Tax Agreement (SSUTA), an effort to simplify and modernize sales and use tax administration. States that participate in SSUTA offer businesses reduced filing requirements and access to certified service providers who can automate the entire collection and remittance process.

For the modern business owner, the "wait and see" approach to sales tax is no longer viable. With states utilizing increasingly sophisticated data-mining techniques to identify non-compliant out-of-state sellers, the risk of back taxes, penalties, and interest is higher than ever. Compliance in 2026 is defined by proactive registration, accurate rate calculation, and a rigorous understanding of the specific nexus triggers in every state where a customer resides. By integrating these tax considerations into the core of their operational strategy, businesses can avoid the pitfalls of the American multi-state tax maze and focus on sustainable growth in an interconnected economy.