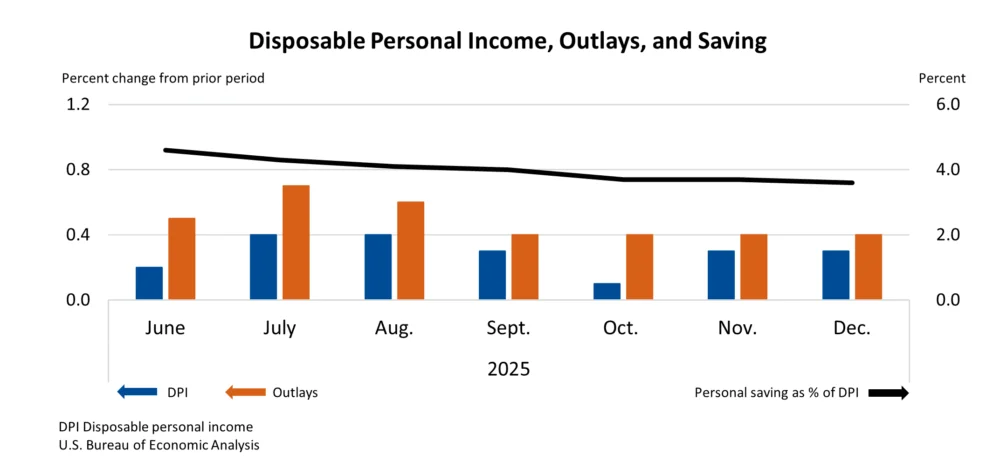

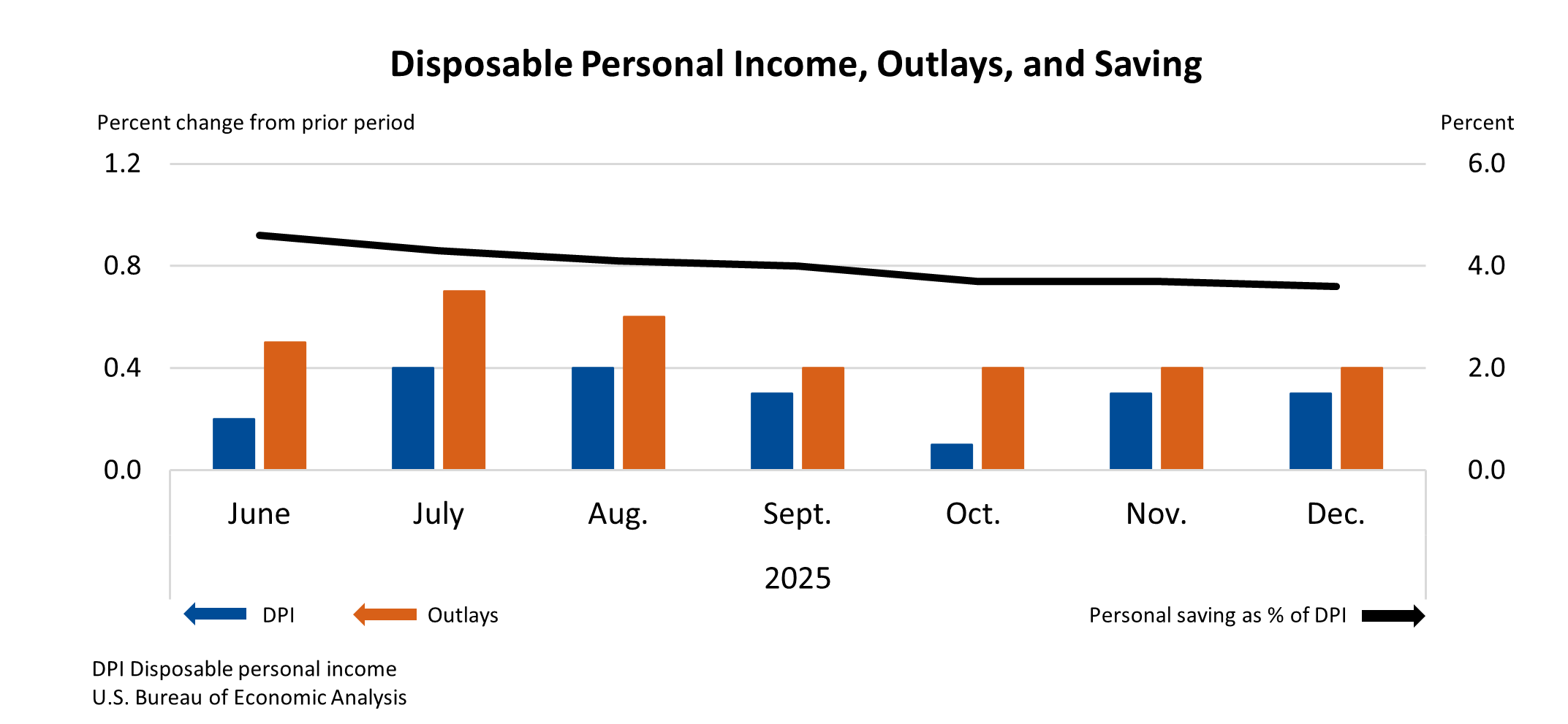

The United States economy demonstrated a pattern of measured expansion in December 2025, as evidenced by a modest increase in personal income and a corresponding uptick in consumer spending. According to data released by the U.S. Bureau of Economic Analysis (BEA), personal income rose by $86.2 billion, or 0.3 percent, during the month. This growth was accompanied by a $75.7 billion, or 0.3 percent, increase in disposable personal income (DPI), which represents income after taxes. Concurrently, personal consumption expenditures (PCE), a key indicator of consumer spending, saw a rise of $91.0 billion, or 0.4 percent.

This latest report, originally slated for release on January 29, 2026, experienced a rescheduling to February 20, 2026. The delay was a direct consequence of the federal government shutdown that spanned October and November of 2025, impacting the operational capacity of various government agencies, including the BEA. The disruption underscored the vulnerabilities of government data collection and dissemination processes to political stalemates, highlighting the need for robust contingency planning in such events.

Deeper analysis of the income figures reveals that the overall increase in current-dollar personal income was primarily driven by gains in personal current transfer receipts and compensation. These components of income are critical for understanding the financial well-being of households, with transfer receipts often encompassing government benefits and compensation reflecting wages and salaries. The sustained growth in these areas suggests a degree of resilience in the labor market and social safety net programs, even as broader economic conditions remained subject to evolving global and domestic factors.

Disposable personal income, a more direct measure of the funds available for spending and saving, also saw a steady increase. This growth in DPI is crucial as it forms the basis for consumer spending decisions. The 0.3 percent rise indicates that households had slightly more discretionary funds at their disposal in December compared to the previous month. However, it is important to note that real DPI, which accounts for inflation, registered a more tepid growth of 0.0 percent in December. This suggests that while nominal incomes rose, the purchasing power of those incomes did not significantly increase, pointing to persistent inflationary pressures.

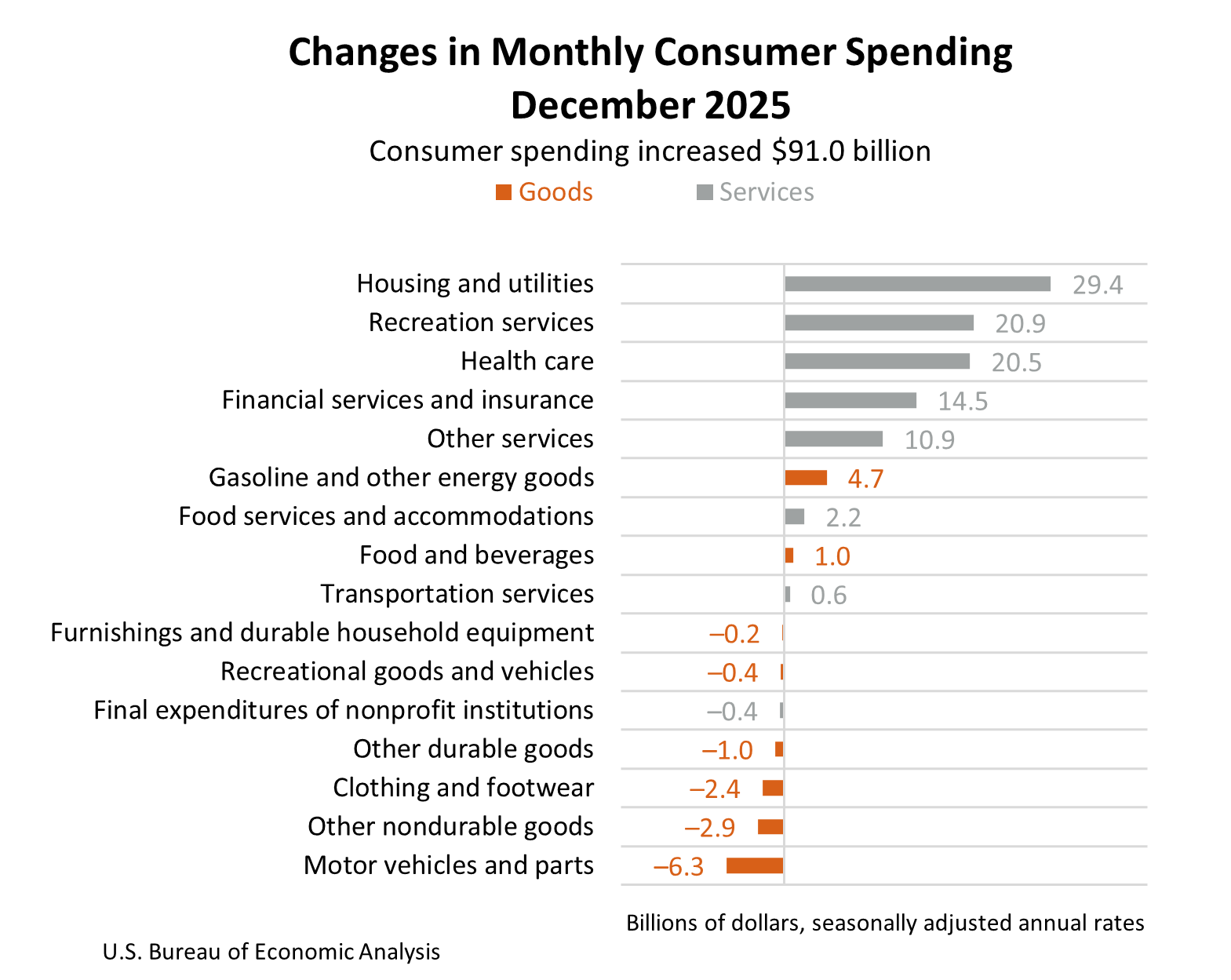

Consumer spending, as measured by personal consumption expenditures (PCE), closely tracked the increase in disposable income, rising by 0.4 percent in current dollars. This expenditure pattern is a significant driver of economic activity, and its continued expansion in December signaled ongoing consumer confidence and demand. The breakdown of PCE further illuminates the nature of this spending. Spending on services surged by $98.5 billion, while spending on goods experienced a contraction of $7.5 billion. This divergence highlights a continued consumer preference shift towards services, a trend observed in recent periods, potentially influenced by evolving lifestyle choices and the normalization of in-person activities post-pandemic.

Economic Context and Recent Trends

The December 2025 economic landscape was characterized by a complex interplay of factors. While the income and spending data indicated continued, albeit moderate, economic growth, underlying concerns persisted regarding inflation, interest rate policies, and geopolitical uncertainties. The Federal Reserve had been navigating a delicate balance, aiming to curb inflation without triggering a significant economic downturn. The data from December provided further input for these ongoing policy deliberations.

In the preceding months of 2025, the U.S. economy had shown signs of moderating growth after a period of robust recovery. Inflation, while showing some signs of easing from its peaks, remained above the Federal Reserve’s target of 2 percent. This persistent inflationary pressure had led to a series of interest rate hikes by the Federal Reserve throughout 2024 and into 2025, aiming to cool down demand and stabilize prices. The impact of these monetary policy tightening measures was a key area of focus for economists and policymakers.

The government shutdown in late 2025 cast a shadow over the release of economic data, adding a layer of uncertainty. Such shutdowns can disrupt the flow of critical economic information, making it more challenging for businesses and policymakers to make informed decisions. The extended duration of the October-November shutdown underscored the potential for significant disruptions to government functions and the economic data infrastructure.

Personal Outlays and Saving Dynamics

Beyond personal consumption expenditures, total personal outlays, which include PCE, personal interest payments, and personal current transfer payments, increased by $90.2 billion in December. This comprehensive measure of household spending reflects the totality of funds directed towards consumption and financial obligations.

The personal saving rate, a crucial metric for assessing household financial health and capacity for future spending or investment, stood at 3.6 percent in December. This rate represents personal saving as a percentage of disposable personal income. While this indicates that households were saving a portion of their income, the relatively modest saving rate suggests that a significant portion of disposable income was being allocated to consumption. The personal saving itself amounted to $830.8 billion in December. The dynamics of the saving rate are closely watched as they can signal consumer confidence, concerns about future economic stability, and the availability of funds for discretionary spending. A sustained low saving rate can sometimes be a precursor to reduced consumer spending in the future, should economic conditions become more challenging.

Inflationary Indicators and Their Implications

The PCE price index, a key inflation gauge closely monitored by the Federal Reserve, increased by 0.4 percent in December from the previous month. This monthly increase was consistent across both the headline PCE index and the core PCE price index, which excludes volatile food and energy prices. This persistent month-over-month inflation rate signaled that price pressures remained a significant concern for the U.S. economy.

On an annual basis, the PCE price index rose by 2.9 percent in December compared to the same month in the previous year. The core PCE price index, excluding food and energy, saw a slightly higher increase of 3.0 percent year-over-year. These figures, while indicating a moderation from the multi-decade highs seen in prior periods, still represented inflation rates that were above the Federal Reserve’s target. The stickiness of core inflation, in particular, suggested that underlying inflationary forces were proving to be more resilient than anticipated, potentially influencing the Federal Reserve’s future monetary policy decisions. The path of inflation remained a critical determinant of interest rate trajectories and, consequently, the broader economic outlook.

Analysis of Real vs. Nominal Growth

The distinction between nominal and real figures is essential for a comprehensive understanding of economic trends. While nominal income and spending figures showed positive growth in December, the inflation-adjusted (real) figures provided a more nuanced picture. Real disposable personal income remained flat, indicating that the purchasing power of income did not increase. Similarly, real PCE, which measures the volume of goods and services consumed, increased by a modest $11.5 billion, or 0.1 percent, on a monthly basis. This tepid growth in real consumption suggests that while consumers were spending more dollars, they were not necessarily buying significantly more in terms of quantity, a direct consequence of elevated price levels.

The divergence between nominal and real growth underscores the impact of inflation on household budgets and the overall economy. For consumers, it means that their nominal pay raises might not translate into a substantial increase in their ability to purchase goods and services. For businesses, it can create challenges in managing costs and setting prices.

Broader Economic Implications and Outlook

The economic data for December 2025 painted a picture of an economy continuing to expand, albeit at a measured pace. The resilience of consumer spending, supported by modest income growth, provided a foundation for continued economic activity. However, the persistent inflationary pressures, as indicated by the PCE price index, remained a significant challenge.

The Federal Reserve’s policy decisions would continue to be heavily influenced by incoming inflation data. A sustained period of elevated inflation, even with moderate income growth, could necessitate further monetary tightening or a prolonged period of higher interest rates. This, in turn, could dampen consumer and business investment, potentially slowing economic growth. Conversely, any clear signs of inflation receding towards the 2 percent target could provide the Federal Reserve with more flexibility to ease monetary policy, potentially stimulating economic activity.

The performance of the services sector in consumer spending, which saw a notable increase, suggested a continued evolution of consumer behavior. This trend could have implications for various industries, with those focused on services potentially benefiting more than those primarily dealing in goods.

The background of the government shutdown also served as a reminder of the potential for policy-induced disruptions to economic data and market confidence. Such events can create short-term volatility and underscore the importance of stable governance for economic predictability.

Future Projections and Data Releases

The U.S. Bureau of Economic Analysis has outlined its schedule for upcoming releases of Personal Income and Outlays (PIO) data. The next release, covering January 2026 data, is scheduled for March 13, 2026, at 8:30 a.m. Eastern Daylight Time. These future releases will be critical for tracking the evolving economic trajectory and assessing the impact of ongoing economic policies and global events. The BEA has also indicated improvements to its news release packages, including direct links to its online Interactive Data Tables, aiming to enhance user access and efficiency. The discontinuation of PDF and Excel format news release tables, beginning with the February 2026 estimate, marks a shift towards digital-first data dissemination.

The technical notes accompanying the December 2025 report highlighted revisions to personal income estimates for October and November 2025, incorporating updated data from the Bureau of Labor Statistics (BLS) on employment, hours, and earnings. Such revisions are standard practice in economic data releases and are crucial for ensuring the accuracy and reliability of national economic accounts. These ongoing updates provide a more refined understanding of economic performance over time.

In summary, the December 2025 data indicated a U.S. economy in a phase of sustained, albeit modest, growth, characterized by rising incomes and consumer spending. However, the persistent challenge of inflation and the implications of monetary policy remained central to the economic narrative, shaping expectations for the path ahead. The careful monitoring of income, spending, and inflation trends will be crucial for navigating the economic landscape in the coming months.