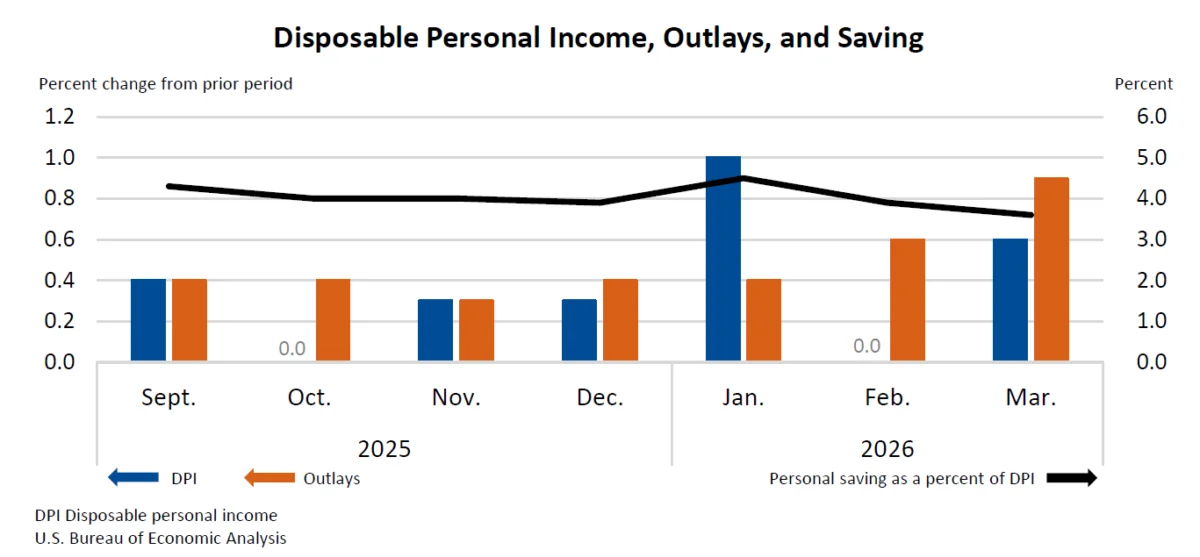

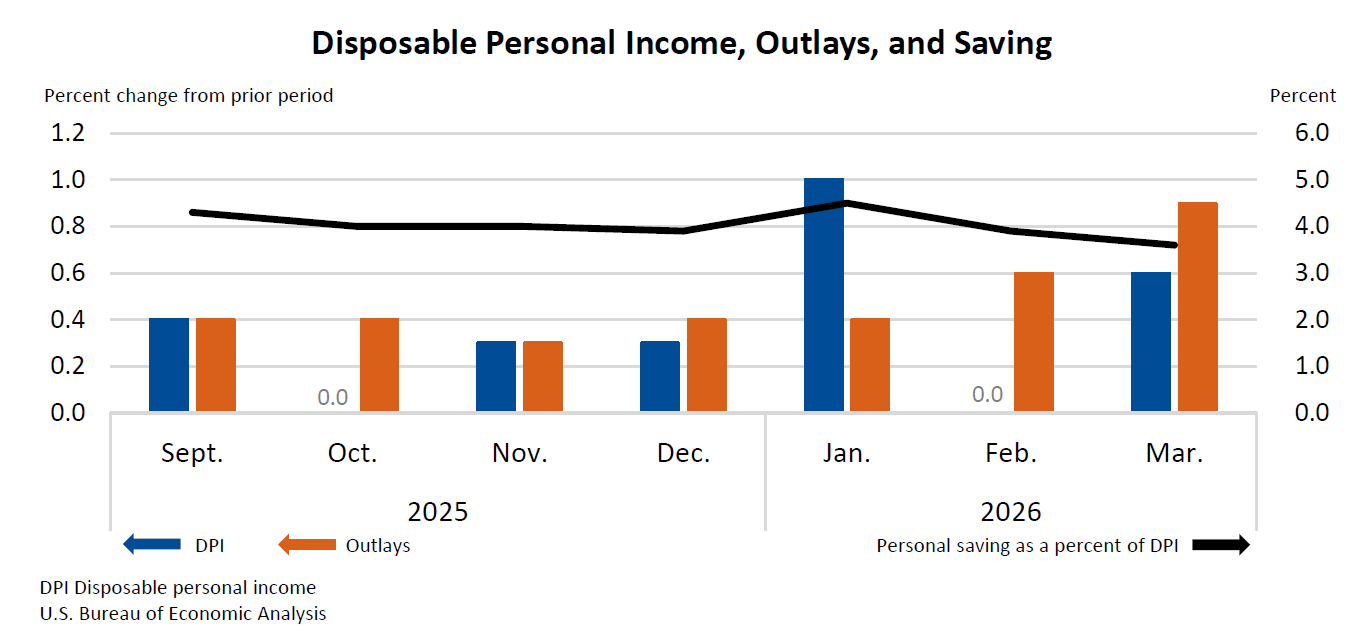

The United States experienced a notable uptick in personal income during March, with a 0.6 percent monthly increase, translating to $149.2 billion, according to the latest data released by the U.S. Bureau of Economic Analysis (BEA). This growth was primarily fueled by gains in compensation and farm proprietors’ income, signaling a robust start to the spring economic period. This rise in income has direct implications for consumer spending, with disposable personal income (DPI) – the income remaining after taxes – also climbing by 0.6 percent, an increase of $142.5 billion. Concurrently, personal consumption expenditures (PCE), a key indicator of consumer spending, saw a substantial rise of 0.9 percent, amounting to $195.4 billion, underscoring a strong inclination for consumers to spend their increased earnings.

The BEA’s comprehensive report details a dynamic economic landscape where increased earnings are translating into greater economic activity. Personal outlays, which encompass PCE, personal interest payments, and personal current transfer payments, escalated by $198.6 billion in March. This surge in spending, however, did not significantly erode personal savings. In March, personal saving stood at $857.3 billion, with the personal saving rate – the proportion of disposable personal income that is saved – holding steady at 3.6 percent. This indicates that while consumers are actively spending, they are also maintaining a degree of financial prudence.

Driving Forces Behind Income Growth

The primary drivers of the current-dollar personal income increase in March were identified as gains in compensation and farm proprietors’ income. Compensation, which includes wages and salaries, benefits, and proprietors’ contributions to employee pension and insurance funds, is a cornerstone of personal income. An expansion in this category suggests a healthy labor market with potential increases in employment or wage growth. Farm proprietors’ income, which can be volatile due to factors like crop yields and commodity prices, also contributed positively, indicating a favorable period for the agricultural sector.

These positive contributions were partially offset by a decrease in other government social benefits. While the specific nature of these benefits was not detailed in the initial release, such fluctuations can occur due to policy changes, program adjustments, or seasonal factors. However, the net effect was a solid overall increase in personal income, providing a foundation for increased consumer activity.

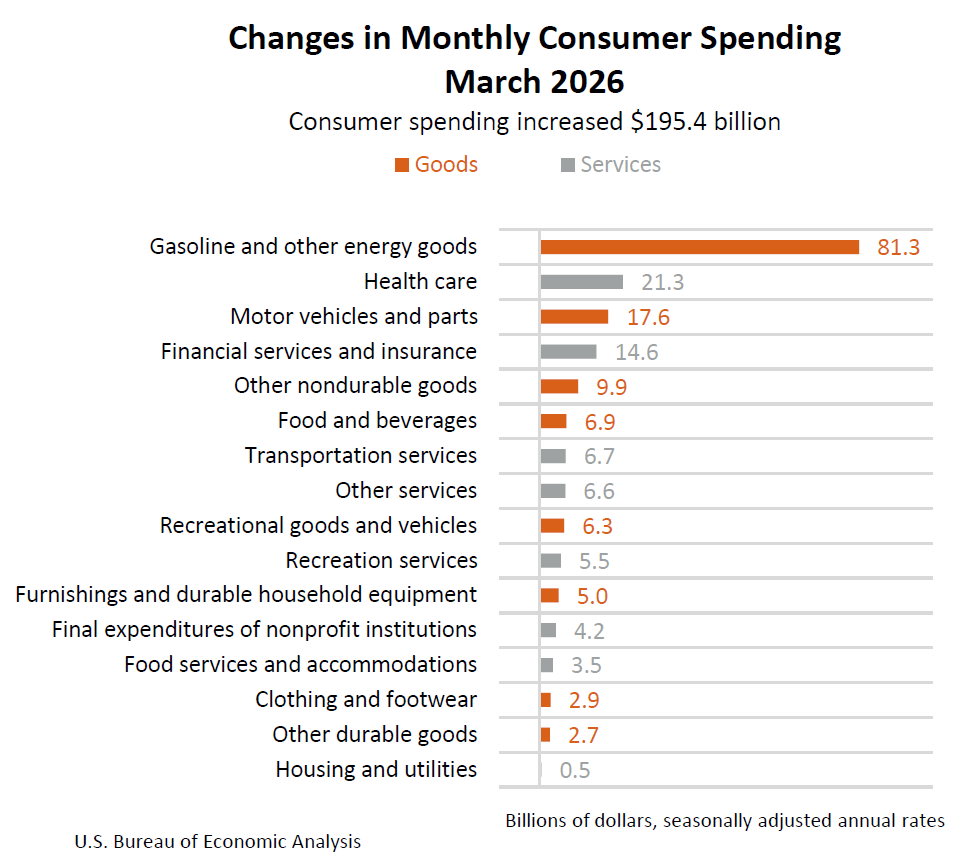

Consumer Spending on the Rise: Goods and Services Both Benefit

The substantial $195.4 billion increase in current-dollar personal consumption expenditures (PCE) in March paints a picture of a consumer base actively engaging with the economy. This growth was broadly distributed across both goods and services. Spending on goods rose by $132.6 billion, while spending on services increased by $62.9 billion.

The robust growth in spending on goods suggests a strong demand for tangible products, which could range from durable goods like vehicles and appliances to nondurable goods such as food and clothing. This uptick in goods consumption is a positive signal for retailers and manufacturers alike, indicating a healthy flow of products through the economy.

Simultaneously, the rise in spending on services, though smaller in absolute terms than goods, is also a significant indicator of economic vitality. This includes expenditures on areas such as healthcare, transportation, recreation, and financial services. An increase in service spending often reflects a growing confidence in the economy and a willingness of consumers to invest in experiences and essential services.

Real Consumption Reflects Inflationary Pressures

While nominal PCE saw a significant jump, the growth in real PCE, which adjusts for inflation, was more modest. Real PCE increased by $39.6 billion, or 0.2 percent, in March. This disparity between nominal and real growth highlights the impact of inflation on purchasing power. Even with higher nominal spending, the actual volume of goods and services consumed increased at a slower pace, indicating that price increases are a factor for consumers.

The Personal Consumption Expenditures (PCE) price index, a key inflation gauge, rose by 0.7 percent from the preceding month. This acceleration in inflation, particularly for goods and services generally, suggests that while consumers are spending more, they are also paying higher prices. The core PCE price index, which excludes volatile food and energy prices, increased by a more moderate 0.3 percent, indicating that inflationary pressures in essential categories might be less pronounced but still present.

On a year-over-year basis, the PCE price index for March saw a 3.5 percent increase. The core PCE price index also demonstrated an upward trend, rising by 3.2 percent from the same month one year ago. These figures provide context for the monthly inflation data, showing a sustained elevation in price levels compared to the previous year. This persistent inflation, even as income and spending rise, presents a complex scenario for policymakers and consumers, potentially impacting future spending decisions and the overall economic trajectory.

Analytical Perspective and Implications

The March data from the BEA presents a multifaceted view of the U.S. economy. The increase in personal income, driven by compensation and farm income, is a positive indicator of economic health and consumer confidence. This growth in earnings provides households with greater financial capacity, which is reflected in the robust rise in personal consumption expenditures. The balanced growth across both goods and services suggests a broad-based consumer demand that supports various sectors of the economy.

However, the concurrent rise in inflation, as evidenced by the PCE price index, warrants close attention. The fact that real PCE growth lagged behind nominal PCE growth indicates that a portion of the increased spending is absorbed by higher prices. This dynamic can erode the real purchasing power of consumers, potentially leading to a slowdown in spending if wage growth does not keep pace with inflation.

The personal saving rate of 3.6 percent, while not exceptionally high, suggests that consumers are not drastically depleting their savings to finance current consumption. This could imply that the income growth is sufficiently covering increased spending and maintaining a baseline level of savings. However, sustained inflation could put pressure on this saving rate in the future, as consumers may need to dip into savings to maintain their consumption levels.

The BEA’s technical notes also provided insights into specific adjustments made to the data. The PCE price index for legal services was adjusted for January and March, indicating a meticulous process of data refinement. Furthermore, revisions to personal income for January and February, incorporating updated Medicaid benefit data, highlight the dynamic nature of economic data collection and the ongoing efforts to ensure accuracy. These adjustments, while technical, underscore the rigor behind the economic statistics that guide policy and business decisions.

Broader Economic Context and Historical Trends

Understanding the March figures requires placing them within a broader economic context. The post-pandemic economic recovery has been characterized by fluctuating inflation rates and shifting consumer behavior. While stimulus measures and pent-up demand initially fueled significant spending increases, the subsequent rise in inflation has presented a new challenge. The BEA’s data on personal income and consumption expenditures are critical for assessing the effectiveness of monetary and fiscal policies aimed at managing inflation and promoting sustainable economic growth.

Historically, a 0.6 percent increase in personal income is considered a healthy monthly gain. Similarly, a 0.9 percent increase in PCE suggests strong consumer demand. The key question for economic analysts will be the sustainability of these trends in the face of ongoing inflationary pressures and potential shifts in consumer sentiment.

The next release of Personal Income and Outlays data, scheduled for May 28, 2026, will provide crucial insights into April’s economic performance. This subsequent data will offer a clearer picture of whether the trends observed in March are continuing, accelerating, or moderating, allowing for a more informed assessment of the economy’s trajectory.

Official Responses and Expert Commentary (Inferred)

While the original release did not include direct quotes, it is standard practice for economic data of this magnitude to be analyzed by various stakeholders. Federal Reserve officials, for instance, would closely examine these figures when formulating monetary policy. A sustained rise in inflation, even with income growth, could influence decisions regarding interest rates.

Economists from financial institutions and research think tanks would likely offer their interpretations. Some might emphasize the positive signs of income and spending growth, viewing it as evidence of economic resilience. Others might express concerns about the inflationary pressures, pointing to the need for continued vigilance in price stability. Business leaders would analyze these trends to inform their investment and hiring decisions, while consumer advocacy groups might focus on the impact of inflation on household budgets.

The BEA’s role is to provide objective data. However, the implications of this data are far-reaching, influencing discussions among policymakers, market participants, and the public about the health and direction of the U.S. economy. The interplay between rising incomes, robust spending, and persistent inflation will remain a central theme in economic discourse for the foreseeable future.

Looking Ahead: The Path Forward

The March data on personal income and outlays presents a picture of an economy that is expanding, with consumers actively participating. The significant increases in both income and spending are encouraging signs. However, the persistent inflation, particularly evident in the PCE price index, introduces a layer of complexity. The ability of wage growth to outpace inflation will be a critical determinant of consumers’ real purchasing power and the overall sustainability of economic expansion.

The BEA’s commitment to refining its data, as demonstrated by the technical notes on legal services prices and revisions to past estimates, ensures that policymakers and the public have access to the most accurate economic indicators available. As the economy navigates these evolving conditions, the monthly releases of personal income and outlays will remain indispensable tools for understanding the financial well-being of American households and the broader health of the U.S. economy. The upcoming data for April will be eagerly anticipated for further clarity on these crucial economic dynamics.