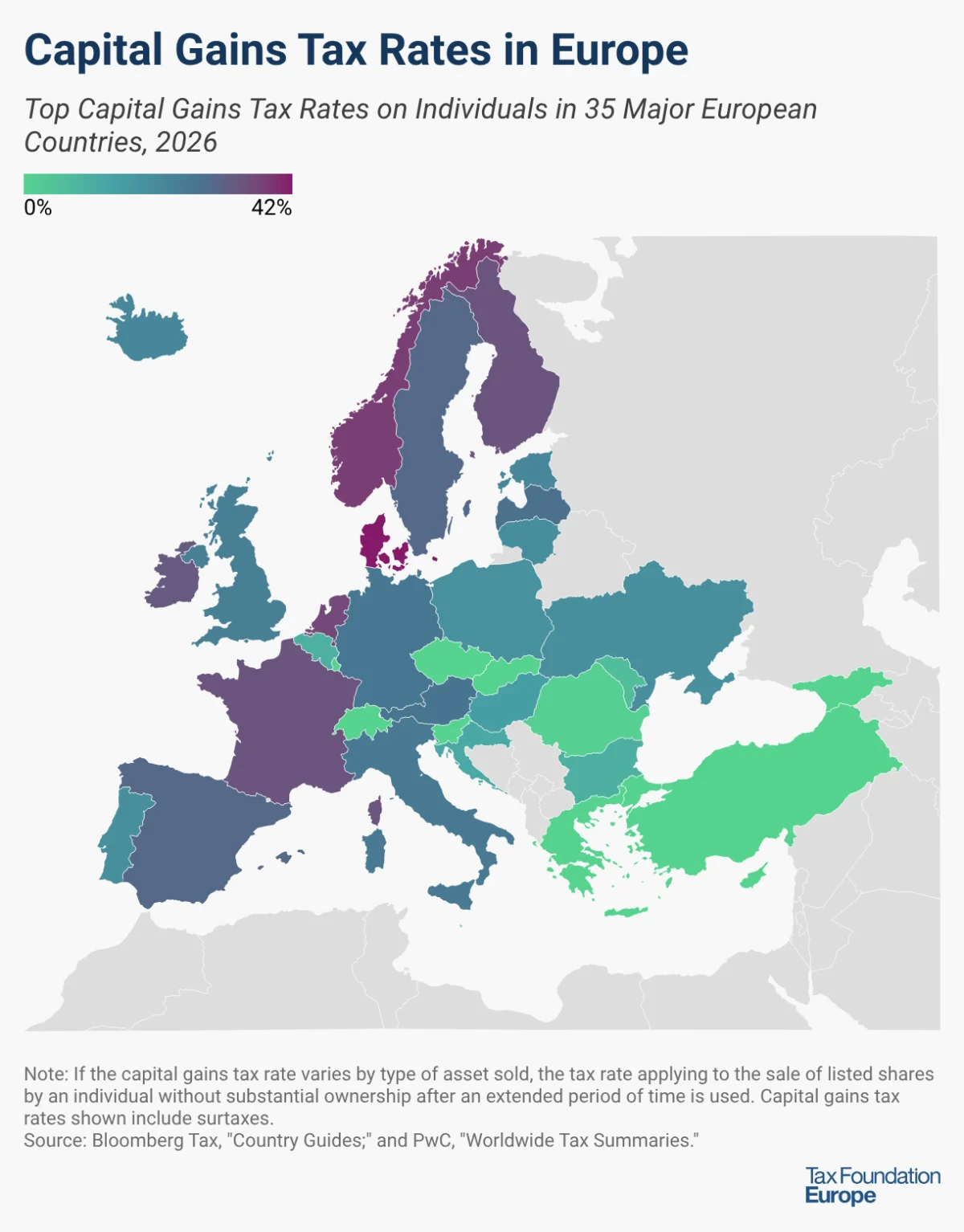

As Europe looks towards 2026, a diverse and complex landscape of capital gains tax (CGT) rates for individuals holding long-held listed shares without substantial ownership emerges, revealing significant disparities in fiscal approaches across the continent. Analysis of the projected top marginal rates for that year indicates a spectrum ranging from a complete absence of CGT in several nations to a substantial 42.0 percent in Denmark, underscoring the varied economic philosophies and revenue strategies employed by European governments. This intricate web of taxation profoundly influences investment decisions, capital mobility, and the overall competitiveness of national economies within the broader European market.

A Panoramic View of European Capital Gains Taxation

The data for 2026, compiled from sources such as Bloomberg Tax and PwC’s Worldwide Tax Summaries, paints a detailed picture of the fiscal environment awaiting investors. While the average top marginal rate for capital gains across the surveyed European countries hovers around 19.5 percent, this figure masks considerable divergence. A significant cluster of nations has opted for a zero percent CGT rate under specific conditions, aiming to foster investment and stimulate their financial markets. Conversely, a smaller group imposes some of the highest rates globally, reflecting a different set of priorities often centered on wealth redistribution and robust public services.

The Zero-Tax Enclave: Attracting Capital and Fostering Growth

A notable characteristic of the 2026 landscape is the presence of several countries where capital gains on long-held listed shares are entirely exempt from taxation, albeit often under specific conditions designed to prevent speculative abuse or target specific types of investment. These nations include Cyprus, the Czech Republic, Georgia, Greece, Luxembourg, Malta, Slovakia, Slovenia, Switzerland, and Turkey.

In Cyprus, shares listed on any recognised stock exchange are outright excluded from CGT, positioning the island nation as an attractive hub for international investors. Similarly, Malta exempts transfers of shares listed on recognised stock exchanges, reinforcing its reputation as a business-friendly jurisdiction.

The Czech Republic offers an exemption if shares of a joint stock company are held for at least three years, extending to five years for limited liability companies. This policy encourages longer-term investment over short-term trading. Georgia applies a similar principle, with capital gains from shares held for more than two years generally exempt from Personal Income Tax (PIT).

Greece, under the specified conditions (individuals owning long-held listed shares without substantial ownership), imposes a 0% rate, with CGT at 15% only applying if an individual holds at least 0.5% of the share capital of the listed entity. This distinction is crucial for understanding the target scope of the exemption.

Luxembourg, a significant financial center, exempts capital gains if a movable asset like shares was held for at least six months and is owned by a non-large shareholder, taxing them at progressive rates only if held for less than six months. A dependency contribution of 1.4 percent is still applicable for individuals subject to the Luxembourg social security system on the taxable portion of gains.

Slovakia offers an exemption for shares held for more than one year, provided they are not part of the taxpayer’s business assets, while Slovenia takes a longer-term view, granting a 0% rate only if the asset was held for more than 15 years, with rates up to 25% for shorter holding periods.

Switzerland, renowned for its favorable tax environment, normally exempts capital gains on movable assets such as shares. Turkey provides a similar incentive, with shares traded on the stock exchange and held for at least one year being tax-exempt, extending to two years for joint stock companies. These zero-tax policies are often underpinned by a strategic aim to attract foreign direct investment, boost domestic capital formation, and enhance the liquidity and depth of local stock exchanges. They represent a competitive advantage in the global race for capital, signaling a commitment to a less burdensome tax environment for long-term investors.

The High-Tax Bracket: Revenue Generation and Wealth Redistribution

At the other end of the spectrum are countries imposing substantial capital gains taxes, often reflecting a policy emphasis on revenue generation, wealth redistribution, or the funding of extensive social welfare programs. Denmark leads this group with a top marginal rate of 42.0 percent. This rate applies to share income exceeding DKK 79,400 (approximately EUR 10,650), with income below this threshold taxed at 27.0 percent, indicating a progressive approach to capital income.

Norway follows closely with an effective rate of 37.8 percent. While capital gains are taxed at a 22.0 percent rate, a significant multiplier of 1.72 is applied before taxation to gains from the sale of shares, effectively increasing the tax burden. This mechanism underscores Norway’s approach to ensuring that capital income contributes substantially to state coffers.

The Netherlands employs a unique system, taxing the net asset value at a flat rate of 36.0 percent on a deemed annual return above an annual exemption of EUR 59,357 per person. The deemed annual return varies by the total value of assets owned, reflecting a wealth-based approach rather than a direct tax on realized gains.

Other high-tax jurisdictions include Finland and France, both at 34.0 percent. Finland applies a 30.0 percent rate up to EUR 30,000 of taxable capital income, with the excess taxed at 34.0 percent. France imposes a flat 30.0 percent tax on capital gains, augmented by an additional 4.0 percent for high-income earners. Ireland levies a 33.0 percent CGT, though annual gains up to EUR 1,270 for an individual are exempt. Spain and Sweden both stand at 30.0 percent, without the detailed conditionalities seen in other nations. These higher rates are often justified by governments as necessary to maintain social equity, fund public services, and ensure that those who derive significant income from capital contribute proportionally to the national welfare.

The Middle Ground: Balancing Competitiveness and Revenue Needs

A large contingent of European nations occupies the middle ground, balancing the need for tax revenue with the desire to remain competitive in attracting investment. Austria has a flat rate of 27.5 percent, while Germany imposes a flat 25.0 percent tax, plus a 5.5 percent solidarity surcharge, bringing its effective rate to 26.4 percent. Italy stands at 26.0 percent.

In the Baltic states, Latvia levies a flat 25.5 percent on capital gains, with an additional 3.0 percent for high-income earners, leading to a top rate of 28.5 percent. Lithuania applies a top rate of 20.0 percent, while Estonia is set to tax capital gains at 22.0 percent, an increase from 20.0 percent in 2024, signaling a slight upward adjustment in its fiscal policy.

The United Kingdom (post-Brexit) has a 24.0 percent CGT rate, with an annual exemption of EUR 1,270. Iceland applies a 22.0 percent rate, with an exemption for capital income up to ISK 300,000 per year. Ukraine also imposes a 19.5 percent PIT on capital gains.

Lower-Mid Range and Specific Conditions

Several countries present lower, often conditional, rates. Belgium notably taxes capital gains from the sale of financial assets exceeding an annual exemption of EUR 10,000 at 10.0 percent, with a carry-forward mechanism for the exemption. However, capital gains realized outside the normal management of private assets and considered speculative remain subject to a 33.0 percent tax, illustrating a nuanced approach. Bulgaria and Hungary both apply a flat PIT rate of 10.0 percent and 15.0 percent respectively to capital gains. Croatia is at 12.0 percent and Poland at 19.0 percent.

Portugal demonstrates a progressive approach based on holding periods: while a flat 28.0 percent rate generally applies, capital gains income can be 10 percent tax-free for holding periods between 2 and 5 years, 20 percent for 5 to 8 years, and 30 percent after 8 years, incentivizing long-term investment. Romania has particularly low rates, with gains from securities transfers taxed at 3.0 percent for holding periods less than 356 days and a mere 1.0 percent thereafter, aimed at boosting capital market activity. Moldova has a unique system where capital gains are taxed at 50 percent of the PIT rate, resulting in a 6.0 percent effective rate.

Background and Evolution of Capital Gains Taxation

Capital gains tax, fundamentally, is a tax on the profit realized from the sale of a non-inventory asset that was purchased at a lower price. Its implementation and rates are often subjects of intense debate, rooted in differing economic philosophies regarding fairness, efficiency, and revenue generation. Historically, many European nations did not tax capital gains, viewing them differently from earned income. However, over the last few decades, the trend has generally shifted towards including capital gains in the tax base, driven by increasing wealth inequality, the need for public funds, and a desire to harmonize tax treatment across different income sources.

The varying rates for 2026 reflect not a single, unified European tax policy, but rather the sovereign choices of individual states, each responding to its unique economic circumstances, social priorities, and political mandates. The ongoing discussions about wealth taxation at both national and international levels, often spearheaded by organizations like the OECD, also exert pressure on these domestic policies.

Inferred Statements and Reactions

From the perspective of governments adopting zero or very low CGT rates, the underlying message is often one of welcoming capital, fostering entrepreneurship, and stimulating economic growth through investment. Fiscal authorities in Cyprus or Malta might highlight their competitive advantage in attracting foreign investors and supporting local businesses, positioning their nations as gateways for capital. Conversely, Denmark’s Ministry of Finance might emphasize the importance of a progressive tax system in funding its extensive welfare state, ensuring that all forms of income contribute to societal well-being.

The financial industry and individual investors naturally react differently to these varying rates. Low-tax jurisdictions are often lauded by investors for providing higher potential net returns, encouraging capital allocation to those markets. High-tax regimes, however, can be seen as deterrents, potentially leading to capital flight or a reluctance to realize gains, thereby reducing market liquidity. Organizations representing investors often lobby for lower CGT rates, arguing that they stimulate economic activity and innovation.

Economists often debate the "optimal" capital gains tax rate. Supply-side economists might argue that lower rates encourage investment, risk-taking, and ultimately lead to greater economic prosperity and potentially even higher tax revenues (the Laffer Curve effect). Others might contend that higher rates are crucial for addressing wealth inequality and ensuring fiscal stability, particularly in times of increasing public debt. The 2026 rates provide a real-world laboratory for these economic theories.

Broader Impact and Implications

The patchwork of 2026 CGT rates has several significant broader implications. Firstly, it fuels tax competition within the European Union and the wider continent. Countries with lower rates can attract mobile capital and high-net-worth individuals, potentially putting pressure on higher-tax jurisdictions to reconsider their policies or risk losing investment. This dynamic complicates efforts towards greater fiscal harmonization within the EU, where tax policy remains largely a national prerogative.

Secondly, these disparities affect the mobility of capital and individuals. Wealthy investors and entrepreneurs may choose to establish residency or conduct their investment activities in jurisdictions offering more favorable tax treatment for capital gains, influencing migration patterns and the distribution of wealth across Europe.

Thirdly, the varying conditions for exemptions—such as holding periods, ownership thresholds, and the nature of the listed exchange—highlight the complexity investors must navigate. This complexity can increase compliance costs and necessitate specialized advice, particularly for cross-border investments.

Looking ahead, the 2026 rates are not static. Global economic shifts, domestic political changes, and international efforts to combat tax avoidance and promote tax fairness (such as the OECD’s BEPS initiatives, though primarily focused on corporate tax, can influence the broader tax environment) could all lead to further adjustments. The ongoing debate about whether to tax wealth more aggressively, spurred by concerns over inequality and the increasing cost of public services, suggests that capital gains taxation will remain a focal point of fiscal policy discussions well beyond 2026. Understanding this intricate tax landscape is thus crucial for investors, policymakers, and citizens alike, as it shapes the economic future of Europe.