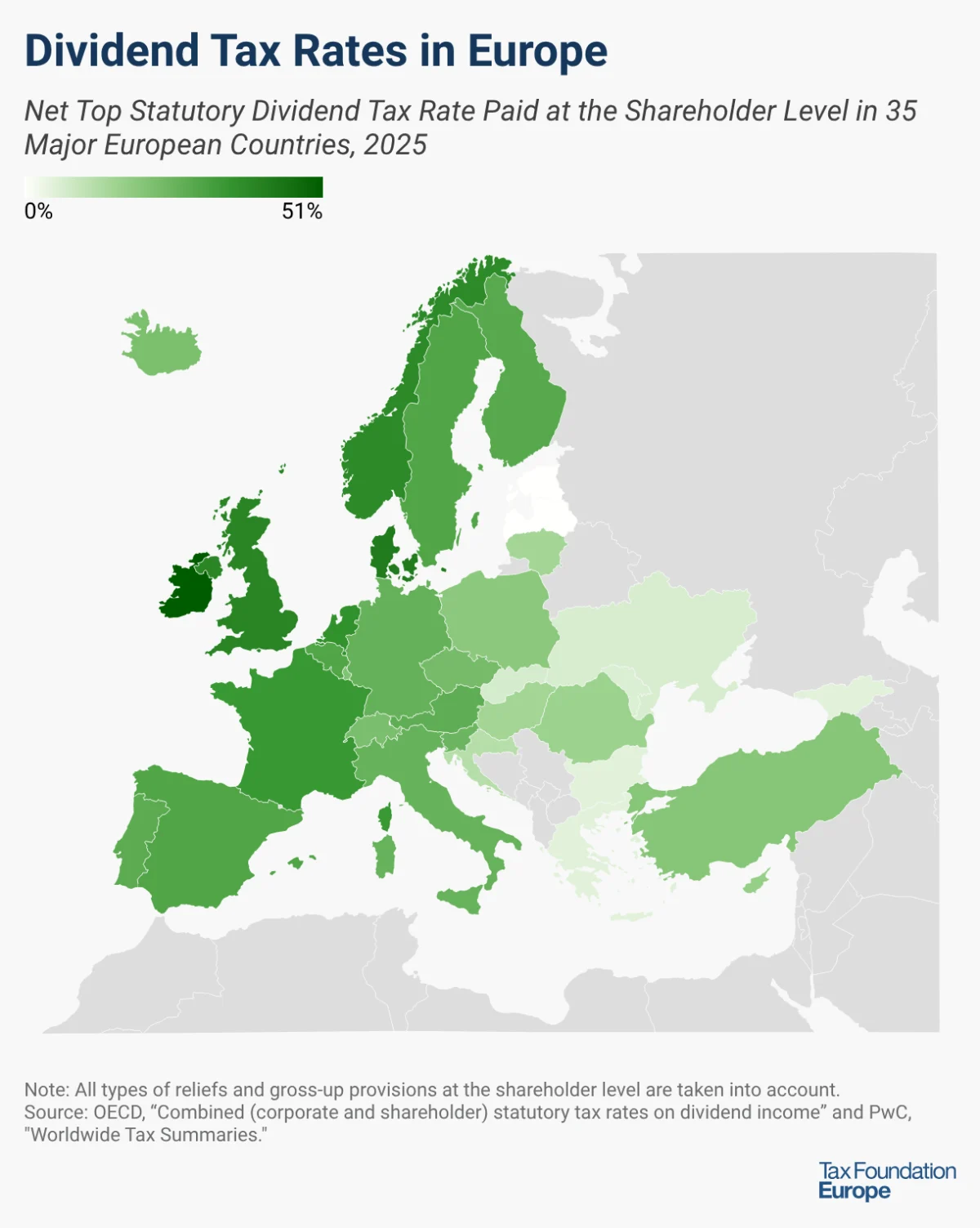

Ireland currently imposes the highest top dividend tax rate among the European countries surveyed, standing at a significant 51 percent, highlighting a stark divergence in fiscal approaches across the continent. Following Ireland, Denmark levies a 42 percent rate, and the United Kingdom applies a 39.35 percent rate, placing these nations at the upper end of dividend taxation within the European economic sphere. This high taxation reflects, in part, national fiscal policies aimed at wealth redistribution, funding robust public services, or maintaining a progressive tax system where capital gains and dividends contribute substantially to state revenues. The cumulative impact of such rates on investor behavior, capital allocation decisions, and the competitiveness of these economies remains a subject of ongoing debate among economists and policymakers. For instance, in Ireland, the high dividend tax rate is often viewed in conjunction with its competitive corporate tax regime, suggesting a strategic balancing act where profits are taxed at distribution rather than solely at the corporate level. Similarly, the UK’s rate, adjusted in recent years, reflects efforts to increase contributions from capital income, particularly following periods of increased public spending and economic uncertainty.

In sharp contrast, Estonia, Latvia, and Malta stand out as the only European countries covered that do not levy a direct tax on dividend income, positioning themselves as attractive destinations for capital distribution. The mechanisms through which these countries achieve a zero-percent dividend tax rate differ significantly, reflecting innovative or distinct national tax philosophies. For Estonia and Latvia, this absence of a direct dividend tax is a direct consequence of their unique cash-flow-based corporate tax systems. Under this model, corporate income tax is not levied on retained earnings but rather when a business distributes its profits to shareholders. Estonia applies a 22 percent corporate income tax at the point of distribution, while Latvia applies 20 percent. This system incentivizes companies to reinvest profits within the business, fostering growth and capital accumulation, as retained earnings are effectively tax-free until distributed. Proponents argue that this system reduces administrative burden, enhances transparency, and encourages long-term investment by deferring taxation until profits leave the corporate sphere. Critics, however, sometimes point to potential complexities in cross-border situations or concerns about immediate revenue generation for the state.

Malta, on the other hand, achieves a zero-percent top dividend tax rate through a full imputation system. Under this system, shareholders are permitted to offset the personal income tax due on their dividend income against the 35 percent corporate tax rate already paid by the distributing company. This mechanism effectively eliminates double taxation of corporate profits (once at the corporate level and again at the shareholder level), a common feature in many traditional tax systems. The Maltese approach ensures that the overall tax burden on distributed profits is borne primarily at the corporate level, making the country highly attractive for international businesses and holding companies seeking efficient repatriation of profits to shareholders. The long-standing stability of this system has been a cornerstone of Malta’s economic strategy to attract foreign direct investment and position itself as a financial hub within the European Union.

The Landscape of Lower Dividend Taxation

Among the European countries that do levy a dividend tax, a cluster of nations maintains remarkably low rates, indicative of policies designed to stimulate investment, attract capital, or support economic development in emerging markets. Bulgaria, Georgia, and Greece lead this group with a minimal 5 percent tax rate on dividends. These rates are among the lowest in Europe and reflect a strategic choice to reduce the cost of capital and encourage both domestic and foreign investment. For Bulgaria and Greece, as EU member states, these low rates aim to enhance their competitiveness within the single market and attract businesses seeking more favorable tax environments. Georgia, a non-EU country with strong European aspirations, also utilizes a low dividend tax rate to foster economic growth and integration into the global economy.

Following closely, Moldova and Ukraine apply dividend tax rates of 6 percent and 6.5 percent, respectively. For these nations, particularly Ukraine, the low rates are part of broader efforts to attract investment and support economic recovery and development, especially in challenging geopolitical contexts. Moldova, an Eastern European country, similarly uses its tax policy to enhance its appeal to investors and stimulate its domestic capital markets. These low rates often come with the expectation that they will boost economic activity, generate employment, and ultimately broaden the overall tax base through increased business profits and consumption taxes, even if direct dividend tax revenues are lower.

Comparative Analysis with the United States and European Average

For a broader perspective, the United States applies a combined state and federal dividend tax rate of 28.73 percent. This composite rate includes various federal income tax brackets for qualified dividends, alongside applicable state-level taxes, demonstrating a multi-layered approach to taxing capital income. The US rate falls between the highest European rates and the lowest, positioning it somewhat in the middle of the spectrum of developed economies. The comparison highlights the diverse philosophical underpinnings of tax policy, with some nations prioritizing higher direct contributions from capital gains and others opting for lower rates to incentivize investment.

Across the 35 European countries examined, the average top dividend tax rate stands at 20.82 percent. This average provides a crucial benchmark, illustrating that while significant disparities exist, the typical European approach involves a moderate level of taxation on distributed profits. This average also underscores the dynamic tension between competing policy objectives: the need for government revenue, the desire to attract and retain capital, and the commitment to principles of tax fairness and wealth distribution. The variance around this average, from zero percent to over 50 percent, is a testament to the sovereign nature of national fiscal policies within a continent increasingly characterized by economic integration.

Notable Changes and Policy Shifts in the European Dividend Tax Landscape

While the original source indicated an empty section for "Notable Changes," the European tax landscape is rarely static, with several countries frequently adjusting their dividend tax rates in response to evolving economic conditions, fiscal pressures, and political priorities. Over the past year, various reports and government announcements have signaled shifts in several jurisdictions, reflecting a broader trend of recalibrating tax policies to address contemporary challenges.

For instance, Germany has seen ongoing debates about its dividend taxation. While its standard rate has remained stable, discussions have intensified around the treatment of high-income earners and the potential for a "solidarity surcharge" or increased capital gains tax to address national debt accumulated during recent crises, indirectly impacting the perceived after-tax return on dividends for certain investor segments. These discussions often emerge from a political desire to ensure that wealthier individuals contribute more to public finances, aligning with principles of social equity.

In France, there have been continuous efforts to simplify the tax code and boost investment. While the "flat tax" (Prélèvement Forfaitaire Unique – PFU) introduced in 2018 set a fixed 30% rate for capital income, including dividends, there are periodic reviews and proposals to adjust components of this rate or introduce exemptions for specific types of investments, particularly those in small and medium-sized enterprises (SMEs). These adjustments are typically aimed at balancing fiscal revenue with incentives for productive investment and job creation.

Some smaller EU economies, like Croatia or Portugal, have reportedly explored or implemented minor adjustments to their dividend tax regimes. For example, a country facing a need to stimulate domestic capital markets might consider a marginal reduction in its dividend tax rate or introduce temporary incentives for reinvestment of dividends. Conversely, a nation aiming to bolster its social security funds might slightly increase the rate, even if only by a few percentage points, to generate additional revenue. These changes, while sometimes incremental, can have significant implications for investor sentiment and capital flows.

The Nordic countries, known for their high levels of public services and progressive taxation, often engage in vigorous policy debates concerning capital income. While Denmark maintains a high rate, countries like Sweden or Finland periodically review their capital income taxes, including dividends, to ensure they remain competitive while upholding their social welfare models. Any proposed changes in these nations typically involve extensive public consultation and parliamentary debate, reflecting a commitment to broad societal consensus on fiscal policy.

The drivers behind these shifts are multifaceted. Post-pandemic economic recovery efforts have pushed many governments to seek new revenue streams or to stimulate specific sectors. Geopolitical events, such as the conflict in Ukraine, have also prompted some nations to reassess their fiscal policies to enhance resilience or support national defense. Furthermore, the global movement towards greater tax transparency and the OECD’s Pillar Two initiative, while primarily focused on corporate income tax, indirectly influence national approaches to capital taxation by encouraging a more coherent and less aggressive form of tax competition. These "notable changes," whether implemented or debated, underscore the dynamic and often politically charged nature of dividend taxation across Europe.

Broader Impact and Implications for European Economies

The disparate landscape of dividend taxation across Europe carries significant implications for capital markets, corporate structuring, foreign direct investment (FDI), and wealth distribution. For corporations, the decision of where to incorporate, where to base headquarters, and how to structure profit repatriation strategies is heavily influenced by these tax rates. Companies operating across multiple jurisdictions must navigate complex tax treaties and national laws to optimize their after-tax returns, often leading to sophisticated corporate structures that minimize overall tax leakage.

From an investor’s perspective, dividend tax rates directly impact the net yield from equity investments. High dividend taxes can make certain markets less attractive for income-focused investors, potentially diverting capital towards jurisdictions with more favorable tax treatment or towards alternative asset classes. This can influence the cost of equity for companies in high-tax countries, potentially affecting their ability to raise capital for expansion and innovation. Conversely, countries with zero or low dividend taxes, such as Estonia, Latvia, and Malta, consciously position themselves as attractive hubs for holding companies, wealth management, and international investment, capitalizing on their favorable tax regimes to draw in capital and expertise.

The varying tax rates also contribute to the ongoing debate about tax competition within the European Union. While the EU strives for a single market, national tax sovereignty allows member states to set their own direct tax rates, including on dividends. This can lead to a "race to the bottom" where countries lower rates to attract businesses, potentially eroding the tax base for others. Efforts towards greater tax harmonization, such as the proposed Common Consolidated Corporate Tax Base (CCCTB), aim to address some of these disparities, though direct dividend taxation often remains a sensitive area of national prerogative.

Furthermore, dividend taxes play a crucial role in government revenue generation. For countries with high rates, dividends contribute significantly to national budgets, funding public services, infrastructure, and social welfare programs. For those with low or zero rates, the rationale is often that lower capital taxes will stimulate economic activity, leading to higher corporate profits, more employment, and increased consumption, which in turn generate other forms of tax revenue (e.g., corporate income tax, VAT, payroll taxes). The effectiveness of these differing approaches in achieving overall economic prosperity and fiscal stability is a continuous subject of economic analysis and political discourse.

The trend towards greater transparency in global taxation, spearheaded by initiatives from the OECD and the EU, is also influencing dividend tax policies. While not directly targeted, increased scrutiny on international tax planning and profit shifting may lead countries to review the fairness and sustainability of their capital income tax regimes. Governments are increasingly balancing the need to attract investment with the imperative to ensure that all forms of income, including capital distributions, contribute equitably to public finances.

In conclusion, Europe’s dividend tax landscape is a complex mosaic of national fiscal philosophies, economic objectives, and geopolitical realities. From Ireland’s high 51 percent rate to the zero-tax models of Estonia, Latvia, and Malta, and the minimal rates in countries like Bulgaria and Greece, the continent presents a spectrum of approaches. These variations profoundly influence investment decisions, corporate strategies, and national economies, reflecting a continuous effort by European nations to balance revenue generation with the imperative to foster economic growth and maintain global competitiveness in an increasingly interconnected world. The average rate of 20.82 percent encapsulates this diversity, serving as a reminder that while Europe seeks economic integration, significant national differences in capital income taxation persist, shaping the continent’s financial future.