Navigating the complexities of payroll tax compliance stands as a fundamental, non-negotiable responsibility for every business owner. The Internal Revenue Service (IRS) mandates not only the withholding of specific taxes from employee earnings but also direct employer contributions, forming a critical component of the nation’s social insurance framework. A failure to meticulously manage these obligations can lead to significant financial penalties, legal repercussions, and reputational damage. This comprehensive guide delves into the intricacies of federal payroll taxes, elucidating the distinctions between various tax types, outlining the precise calculation and deposit schedules, and emphasizing best practices for meticulous record-keeping, ensuring businesses remain fully compliant and fiscally sound.

Understanding the Foundational Differences: Payroll Taxes vs. Income Taxes

At the outset, it is crucial for business owners to differentiate between the various categories of employment taxes, specifically payroll taxes and income taxes. While both are collected through the employer, their nature, funding mechanisms, and beneficiaries are distinct.

Payroll Taxes: These are often referred to as "employment taxes" and are characterized by a shared responsibility between the employer and the employee. They fund specific social insurance programs designed to provide benefits to American workers and their families. The primary component of federal payroll taxes is the Federal Insurance Contributions Act (FICA) tax, which comprises Social Security and Medicare taxes. Both employers and employees contribute an equal percentage of the employee’s wages towards these programs. Unlike income taxes, payroll taxes are earmarked for specific trust funds, directly supporting retirees, the disabled, and those with certain health conditions. Additionally, employers are solely responsible for contributing to the Federal Unemployment Tax Act (FUTA), which funds unemployment benefits.

Income Taxes: In contrast, income tax is paid exclusively by the employee, although employers are responsible for withholding it from their paychecks and remitting it to the appropriate tax authorities. This category includes federal income tax, and potentially state and local income taxes, depending on the jurisdiction. The amount of income tax withheld is determined by information provided by the employee on their Form W-4, including their filing status and any additional withholdings requested. Unlike payroll taxes, which are dedicated to specific social programs, income tax revenue primarily funds general government operations, public services, and infrastructure projects.

For the scope of this article, the primary focus will remain on the mechanics of federal payroll tax obligations, particularly FICA taxes, due to their universal applicability and direct employer contribution requirements.

The Pillars of Payroll Tax: Deconstructing FICA

The Federal Insurance Contributions Act (FICA) tax is the cornerstone of federal payroll tax obligations, directly funding two vital social safety nets: Social Security and Medicare. Understanding their individual components, historical context, and current application is essential for accurate compliance.

Social Security Tax: Established in 1935 as part of President Franklin D. Roosevelt’s New Deal, Social Security was designed to provide a safety net for retired workers. Over time, its scope expanded to include benefits for the disabled, survivors (spouses and children of deceased workers), and certain dependents. The program operates on a pay-as-you-go system, where current workers’ contributions fund the benefits of current retirees and beneficiaries. Both the employer and employee contribute 6.2% each, totaling 12.4% of the employee’s gross taxable wages, up to an annually adjusted wage base. This wage base acts as a cap; any earnings above this threshold are not subject to Social Security tax. For example, in 2024, the Social Security wage base is $168,600, meaning earnings beyond this amount are exempt from Social Security tax for both parties.

Medicare Tax: Introduced in 1965, Medicare provides health insurance primarily for individuals aged 65 or older, younger people with disabilities, and individuals with End-Stage Renal Disease (ESRD) or Amyloidosis. Similar to Social Security, both employers and employees contribute to Medicare. The current rate is 1.45% each, totaling 2.9% of the employee’s gross taxable wages. A key distinction from Social Security is that there is no wage base limit for Medicare taxes; all earned wages are subject to this tax. Furthermore, an Additional Medicare Tax of 0.9% applies to individual wages exceeding certain thresholds ($200,000 for single filers, $250,000 for married filing jointly, and $125,000 for married filing separately). Employers are responsible for withholding this additional tax, but they do not match the 0.9% contribution.

These FICA taxes collectively provide crucial financial and healthcare security for millions of Americans, making their proper collection and remittance a matter of public interest and legal obligation.

The Compliance Imperative: A Step-by-Step Guide for Businesses

Achieving and maintaining payroll tax compliance requires a systematic approach. The following steps outline the procedural chronology for calculating, withholding, reporting, and depositing federal payroll taxes.

1. Precision in Calculation: Determining FICA Tax Liabilities

The first critical step involves accurately calculating the FICA tax components for each employee. This requires meticulous attention to current tax rates, wage bases, and the taxability of various compensation elements.

- Social Security Calculation: For each employee, multiply their gross taxable wages by 0.062 (6.2%) to determine the employee’s share. The employer’s matching contribution is also 0.062 of the same taxable wages. Crucially, remember to cease withholding and contributing Social Security tax once an employee’s cumulative earnings reach the annual Social Security wage base limit. For instance, if an employee earns $5,000 bi-weekly, and the wage base is $168,600, their Social Security contributions would stop after approximately 33 bi-weekly pay periods ($168,600 / $5,000 = 33.72), with the final payment adjusted accordingly.

- Medicare Calculation: Multiply the employee’s gross taxable wages by 0.0145 (1.45%) for the employee’s share and an equal 0.0145 for the employer’s matching contribution. There is no wage base limit for Medicare, meaning all wages are subject to this tax.

- Additional Medicare Tax: For employees whose annual wages will exceed the IRS-specified thresholds, the employer must withhold an additional 0.9% from the employee’s wages. It’s important to reiterate that this additional tax is not matched by the employer.

- Pre-Tax Benefits Consideration: Be mindful that certain pre-tax benefits (e.g., Section 125 health insurance premiums, 401(k) deferrals) can affect taxable wages differently for federal income tax versus FICA taxes. For example, health insurance premiums paid pre-tax typically reduce wages for both federal income tax and FICA, while 401(k) deferrals reduce wages for federal income tax but are generally still subject to FICA. Always confirm the taxability of each benefit.

Example Scenario: Consider an employee, Maria, earning an annual salary of $70,000 in 2024, paid bi-weekly. Her bi-weekly gross pay is approximately $2,692.31 ($70,000 / 26).

- Social Security (Employee & Employer): $2,692.31 x 0.062 = $166.92 each.

- Medicare (Employee & Employer): $2,692.31 x 0.0145 = $39.04 each.

- Total FICA per bi-weekly period: Employee: $166.92 + $39.04 = $205.96. Employer: $166.92 + $39.04 = $205.96.

- The total FICA tax remitted to the IRS for Maria’s bi-weekly pay would be $205.96 (employee) + $205.96 (employer) = $411.92.

2. Secure Withholding and Employer Contribution Segregation

Once calculations are complete, the employer must withhold the employee’s portion of FICA and income taxes from their paycheck. Simultaneously, the employer must set aside their own matching FICA contributions and any FUTA obligations. It is a critical best practice to segregate these funds immediately into a separate bank account, often a dedicated payroll or tax liability account. This prevents accidental commingling with operational funds and ensures that the money is available when deposit deadlines arrive. Failure to hold these funds in trust can lead to severe penalties, as the IRS views withheld taxes as funds held on behalf of the government, not as part of the business’s working capital.

3. Reporting Obligations: Timely Filing of Forms 941 or 944

Beyond calculation and withholding, businesses must formally report their payroll tax liabilities to the IRS. This is primarily done through either Form 941 or Form 944.

- Form 941, Employer’s Quarterly Federal Tax Return: This is the most common form for reporting federal income tax, Social Security tax, and Medicare tax. It is filed quarterly, with strict deadlines: April 30 (for Q1: Jan 1-Mar 31), July 31 (for Q2: Apr 1-Jun 30), October 31 (for Q3: Jul 1-Sep 30), and January 31 of the following year (for Q4: Oct 1-Dec 31). Form 941 reconciles the total wages paid, taxes withheld, and employer contributions for the quarter.

- Form 944, Employer’s Annual Federal Tax Return: This form is for very small businesses with an annual tax liability of $1,000 or less. The IRS will explicitly inform eligible businesses if they are required to file Form 944 instead of Form 941. Form 944 is filed annually, typically by January 31 of the following year. It simplifies reporting for micro-businesses but requires careful monitoring of tax liability to ensure eligibility.

Both forms can be filed electronically (e-file) or via paper. The IRS strongly encourages e-filing for accuracy and efficiency.

4. Deposit Schedule Adherence: The Lookback Period and EFTPS

The frequency and timing of payroll tax deposits are not determined by the filing frequency of Form 941 or 944, but rather by the employer’s total tax liability during a specific "lookback period." This mechanism helps the IRS manage the flow of tax revenue.

- The Lookback Period Defined: For Form 941 filers, the lookback period is a 12-month window running from July 1 of the second preceding calendar year through June 30 of the preceding calendar year. For example, to determine the deposit schedule for calendar year 2026, the lookback period would be July 1, 2024, to June 30, 2025. This period covers four quarters (Q3 and Q4 of 2024, and Q1 and Q2 of 2025). The total tax liability from these four quarters dictates the deposit schedule for 2026. For Form 944 filers, the lookback period is simply the second preceding calendar year’s annual tax liability.

- Deposit Schedules:

- Monthly Depositor: If the total tax liability during the lookback period was $50,000 or less, the business is a monthly depositor. Deposits are due on the 15th day of the following month for taxes accumulated during the current month.

- Semiweekly Depositor: If the total tax liability during the lookback period was more than $50,000, the business is a semiweekly depositor.

- For payments made on Wednesday, Thursday, or Friday, deposits are due by the following Wednesday.

- For payments made on Saturday, Sunday, Monday, or Tuesday, deposits are due by the following Friday.

- The $100,000 Next-Day Rule: This rule is a critical exception. If at any point an employer accumulates $100,000 or more in employment tax liability, those taxes must be deposited by the next business day. Furthermore, triggering this rule automatically makes the employer a semiweekly depositor for the remainder of the current year and the entire following calendar year, regardless of their previous status based on the lookback period.

- Electronic Federal Tax Payment System (EFTPS): All federal tax deposits, including payroll taxes, must be made electronically through the Electronic Federal Tax Payment System (EFTPS). This secure online platform allows businesses to schedule payments up to 365 days in advance, providing flexibility and ensuring timely deposits. Enrollment is mandatory for most businesses.

Adhering strictly to these deposit schedules is paramount. Missing deadlines or making incorrect deposits can trigger significant penalties, including interest charges and failure-to-deposit penalties, which can escalate rapidly.

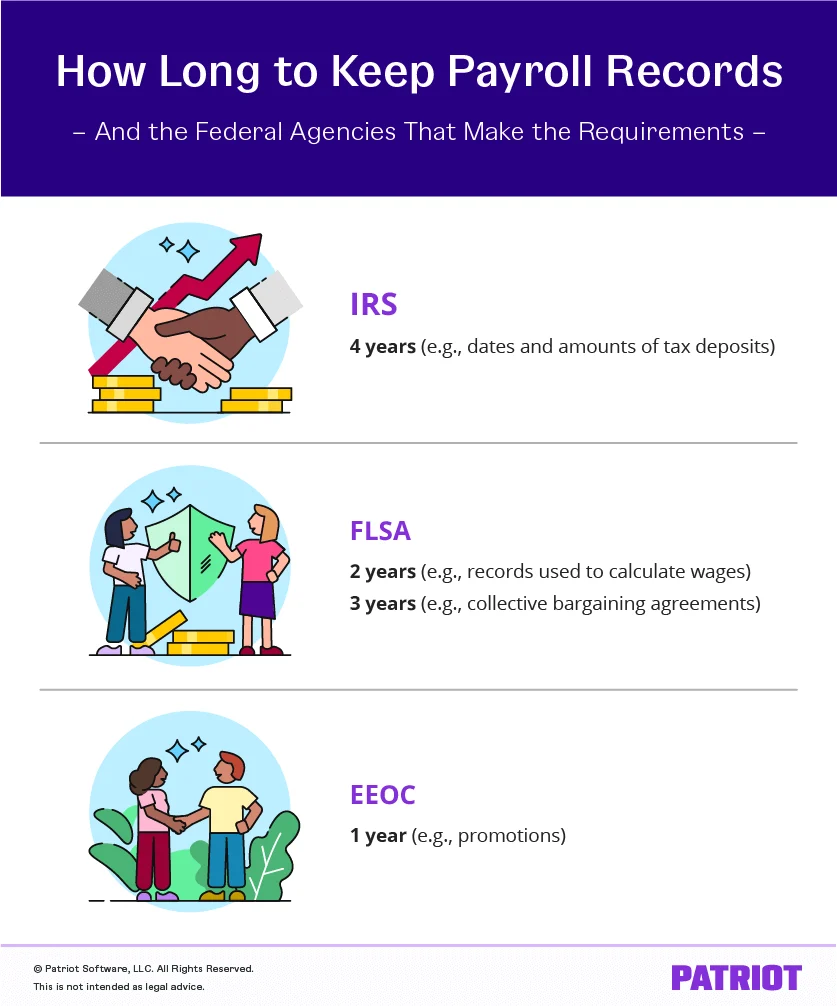

5. Meticulous Record-Keeping: The Cornerstone of Compliance

Even after taxes are calculated, withheld, reported, and deposited, the compliance journey is not complete. Maintaining detailed and accurate records is a non-negotiable requirement for all businesses. These records serve as evidence of compliance during audits, facilitate accurate year-end reporting, and provide a clear financial history.

Key records to retain include:

- Employee information: Names, addresses, Social Security numbers, dates of employment.

- Payroll data: Wages paid, tips reported, fringe benefits, dates of payment.

- Tax forms: Copies of employee W-4s (Employee’s Withholding Certificate), W-2s (Wage and Tax Statement), and state/local withholding forms.

- Reporting forms: Filed copies of Form 941 or 944, Form 940 (Employer’s Annual Federal Unemployment (FUTA) Tax Return).

- Deposit confirmations: EFTPS receipts, bank statements showing tax payments.

- Benefit plan documentation: Records related to pre-tax deductions and their taxability.

- Dates and amounts of tax deposits.

The IRS generally requires federal employment tax records to be kept for at least four years after the due date of the return or the date the tax was paid, whichever is later. State and local agencies may have their own, sometimes longer, retention requirements. Organized and accessible records are invaluable during potential IRS audits, proving due diligence and preventing costly disputes.

Navigating Common Pitfalls: Mitigating Risks in Payroll Tax Management

Despite the clear guidelines, businesses frequently encounter common mistakes that lead to non-compliance. Awareness of these pitfalls is the first step towards prevention:

- Employee Misclassification: Incorrectly classifying employees as independent contractors to avoid payroll tax obligations is a serious offense. The IRS has strict criteria for distinguishing between employees and contractors, and misclassification can result in significant back taxes, penalties, and interest.

- Inaccurate Calculations: Errors in applying FICA rates, overlooking the Social Security wage base, or miscalculating the Additional Medicare Tax can lead to underpayment or overpayment.

- Missed Deadlines: Failing to file reports or make deposits by the prescribed deadlines is a primary cause of penalties. The IRS assesses penalties for both failure to file and failure to deposit.

- Poor Record-Keeping: Inadequate or disorganized records make it challenging to verify compliance during an audit, potentially leading to disputes and additional scrutiny.

- Neglecting State and Local Taxes: While this article focuses on federal taxes, ignoring state unemployment taxes (SUTA), state income tax withholding, or local payroll taxes can also result in severe penalties from state and municipal authorities.

- Lack of Fund Segregation: Using withheld employee taxes for operational expenses is a critical error, as these funds are held in trust for the government.

To mitigate these risks, businesses should consider utilizing robust payroll software, engaging full-service payroll providers, or consulting with qualified tax professionals. These resources can automate calculations, manage deposit schedules, and ensure accurate reporting, significantly reducing the burden and risk of non-compliance.

Broader Economic and Social Impact of Payroll Taxes

Payroll taxes, particularly FICA, are more than just a regulatory burden; they represent a fundamental mechanism for collective social security and economic stability. The revenues generated from Social Security and Medicare taxes directly fund programs that support millions of Americans, preventing widespread poverty among the elderly and disabled, and ensuring access to healthcare for vulnerable populations. The consistent collection and remittance of these taxes are vital for the solvency and sustainability of these programs.

From an economic perspective, payroll taxes redistribute wealth and provide a safety net that stabilizes consumer spending, especially during economic downturns. They represent a significant portion of federal revenue and play a crucial role in the overall fiscal health of the nation. Non-compliance by businesses not only undermines their own financial stability but also erodes the funding base for these critical social programs, potentially impacting future beneficiaries.

Conclusion

Effective payroll tax management is an indispensable aspect of operating a successful and compliant business. It demands a thorough understanding of federal regulations, meticulous adherence to calculation and deposit schedules, and unwavering commitment to accurate record-keeping. While the process can appear daunting, recognizing the distinct roles of payroll and income taxes, mastering FICA calculations, utilizing the Electronic Federal Tax Payment System (EFTPS), and maintaining diligent records will pave the way for seamless compliance. Businesses that prioritize these responsibilities not only avoid penalties but also contribute to the integrity and stability of the nation’s vital social insurance programs. When in doubt, seeking professional advice from certified public accountants or reputable payroll service providers is always recommended to ensure full adherence to the ever-evolving tax landscape.

This article is intended for informational purposes only and does not constitute legal or tax advice. Businesses should consult with qualified tax professionals for guidance specific to their individual circumstances.