The rapid evolution of the digital economy has transformed the traditional retail landscape, shifting a significant portion of global commerce toward online marketplaces. As these platforms grow in scale and complexity, the burden of tax compliance has shifted from individual vendors to the marketplace providers themselves. For entrepreneurs and corporations establishing platforms where multiple third-party sellers list and sell products, the management of sales tax represents one of the most significant operational and legal hurdles. This transition is driven by a combination of landmark judicial rulings and the subsequent enactment of marketplace facilitator laws across the United States. Understanding the nuances of "seller of record" status, economic nexus, and automated tax integration is no longer optional; it is a fundamental requirement for maintaining fiscal viability and regulatory standing in a multi-jurisdictional environment.

The Emergence of the Online Marketplace Model

An online marketplace is defined as a digital platform that facilitates transactions between third-party sellers and buyers. While industry giants such as Amazon, eBay, and Etsy dominate the public consciousness, the model has proliferated into niche sectors. Platforms like 1stDibs for luxury furniture, Ruby Lane for antiques, and specialized eco-conscious sites like Ecohabitude demonstrate the versatility of the marketplace structure. These entities provide the digital infrastructure, payment processing, and marketing reach that allow smaller vendors to access a global audience.

From a consumer perspective, marketplaces offer a centralized, curated shopping experience. For sellers, they lower the barrier to entry by handling the "heavy lifting" of customer acquisition and web development. However, the convenience of this "win-win" scenario is complicated by the intricate web of tax obligations that arise when goods are sold across state and international borders.

The Historical Shift: From Quill to Wayfair

To understand the current state of marketplace tax compliance, one must look at the legal chronology that redefined "nexus"—the connection between a business and a taxing jurisdiction that allows the state to require tax collection. For decades, the standard was set by the 1992 Supreme Court case Quill Corp. v. North Dakota, which dictated that a state could only require a business to collect sales tax if the business had a physical presence, such as an office or warehouse, within that state.

This paradigm was overturned on June 21, 2018, in the landmark decision South Dakota v. Wayfair, Inc. The Supreme Court ruled that states could mandate tax collection based on "economic nexus"—a threshold of economic activity measured by total sales revenue or the number of transactions, regardless of physical presence. This ruling paved the way for "Marketplace Facilitator Laws," which are now active in nearly every U.S. state that imposes a general sales tax. These laws generally require the platform operator to collect and remit sales tax on behalf of their third-party sellers once certain volume thresholds are met.

Strategic Options for Marketplace Tax Management

Marketplace providers must choose a structural approach to tax compliance, a decision that dictates their legal liability and administrative workload. There are two primary avenues:

1. Assuming the Role of Seller of Record

Under this model, the marketplace platform acts as the "Seller of Record" (SoR) or Merchant of Record (MoR). The platform takes full responsibility for the transaction, including the administrative burden of tax compliance. This approach is often preferred by third-party sellers because it absolves them of the need to track varying tax rates across thousands of jurisdictions.

However, for the marketplace provider, this creates a massive compliance footprint. The platform must register for sales tax permits in every state where it meets economic nexus thresholds. Furthermore, because the platform’s sellers are distributed geographically, their physical presence may create "nexus by proxy" for the platform itself. The provider must calculate the correct tax for every item sold, taking into account product-specific exemptions—such as the varying taxability of apparel in New York versus Pennsylvania—and file recurring returns in dozens of states.

2. Facilitating Seller-Led Collection

The alternative model involves providing the technical infrastructure for sellers to manage their own tax obligations. In this scenario, the marketplace provides tools—often via an Application Programming Interface (API)—that allow sellers to input their tax registration data and apply the correct rates to their listings.

While this reduces the platform’s direct liability in some contexts, the rise of marketplace facilitator laws has made this distinction increasingly narrow. In most states, the law now mandates that the platform must be the party responsible for collection and remittance, regardless of whether they wish to pass that responsibility to the seller. Consequently, modern marketplace platforms usually adopt a hybrid approach: they use automated tax engines to calculate and collect the tax at the point of sale, then either remit it centrally or provide detailed reporting for sellers to use in their own filings.

Technical Integration and the Role of Sales Tax APIs

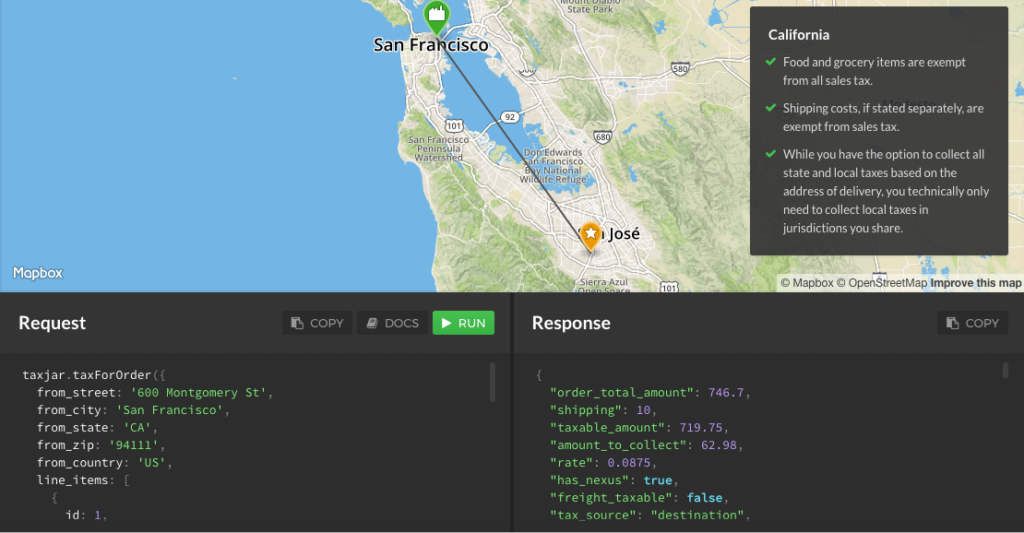

Given that there are over 11,000 taxing jurisdictions in the United States, manual tax calculation is functionally impossible for a growing marketplace. This has led to the widespread adoption of Sales Tax APIs, such as those provided by TaxJar. These tools integrate directly into the marketplace’s checkout flow to provide real-time tax calculations.

The integration of a robust API addresses several critical data points:

- Address Validation: Ensuring the buyer’s location is accurately identified to determine the correct local, county, and state tax rates.

- Product Categorization: Different states tax products differently. For example, digital software may be taxable in one state but exempt in another.

- Sourcing Rules: Determining whether a sale is taxed based on the seller’s location (origin-based) or the buyer’s location (destination-based).

Furthermore, high-level APIs provide multi-channel support. Since many vendors sell on Amazon, Shopify, and their own independent marketplaces simultaneously, the ability to aggregate this data into a single dashboard is essential for accurate reporting and avoiding the "double-counting" of tax liabilities.

Supporting Data and Economic Implications

The fiscal impact of marketplace tax compliance is substantial. According to data from the National Conference of State Legislatures (NCSL), states have seen a significant revenue boost following the Wayfair decision. In the first few years following the ruling, states collected billions in additional sales tax revenue specifically from remote sellers and marketplace facilitators. For instance, California reported billions in revenue from remote sales in the years following its implementation of facilitator laws.

For the marketplace provider, the cost of non-compliance is high. Penalties for failing to collect and remit sales tax can include back taxes, interest, and substantial fines. In some jurisdictions, corporate officers can be held personally liable for unpaid "trust fund" taxes (taxes collected from customers but not remitted to the state).

Reactions from the Business Community

The shift toward marketplace-centric tax collection has met with mixed reactions. State tax authorities generally favor the model because it is more efficient to audit a single large marketplace than thousands of individual small sellers. The Multistate Tax Commission (MTC) has worked to create more uniformity in how these laws are applied, though significant variations between states remain.

From the perspective of small business owners selling on these platforms, marketplace facilitator laws have provided a measure of relief. Before these laws, a small artisan selling on Etsy might have technically been required to register and file in 20 different states—a task that could cost more in accounting fees than the value of the goods sold. By shifting the burden to the platform, the regulatory barrier to entry for small-scale e-commerce has been lowered.

Conversely, marketplace operators have expressed concerns regarding the complexity of "classifying" products and the risk of over-collection or under-collection. If a platform over-collects tax, it risks consumer class-action lawsuits; if it under-collects, it faces state audits.

Future Outlook and Broader Impact

Looking forward, the landscape of marketplace tax is expected to expand beyond the borders of the United States. Many countries in the European Union, as well as the United Kingdom, Canada, and Australia, have implemented similar Value-Added Tax (VAT) or Goods and Services Tax (GST) requirements for marketplace facilitators. This global trend suggests that the "platform-as-tax-collector" model is becoming the international standard.

As artificial intelligence and machine learning become more integrated into financial technology, the accuracy of real-time tax categorization is expected to improve, reducing the risk of human error in product mapping. However, the fundamental challenge remains: as long as tax laws are determined at the local level and commerce happens at the global level, the marketplace provider will remain the critical link in the chain of fiscal compliance. For those building the next generation of online marketplaces, investing in a robust, API-driven tax strategy is not just a matter of accounting—it is a cornerstone of long-term business strategy.