The United States economy demonstrated a moderated pace of expansion in the fourth quarter of 2025, with real gross domestic product (GDP) increasing at an annual rate of 1.4 percent. This figure, released by the U.S. Bureau of Economic Analysis (BEA) in its advance estimate, marks a significant deceleration from the robust 4.4 percent growth recorded in the third quarter. The delay in the release of this crucial economic report, originally slated for January 29, 2026, was attributed to the extensive government shutdown that spanned October and November of 2025, underscoring the disruptive impact of federal legislative impasses on timely economic data dissemination.

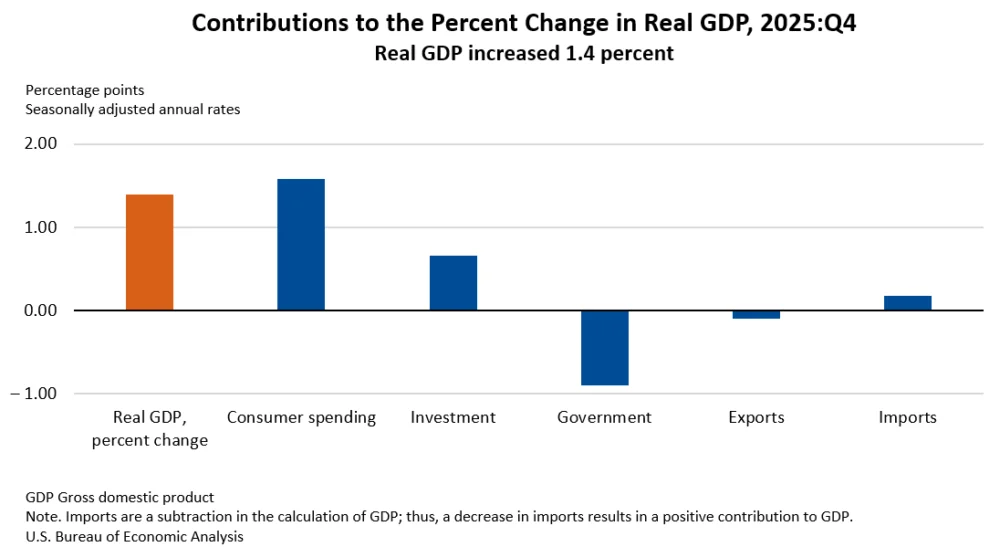

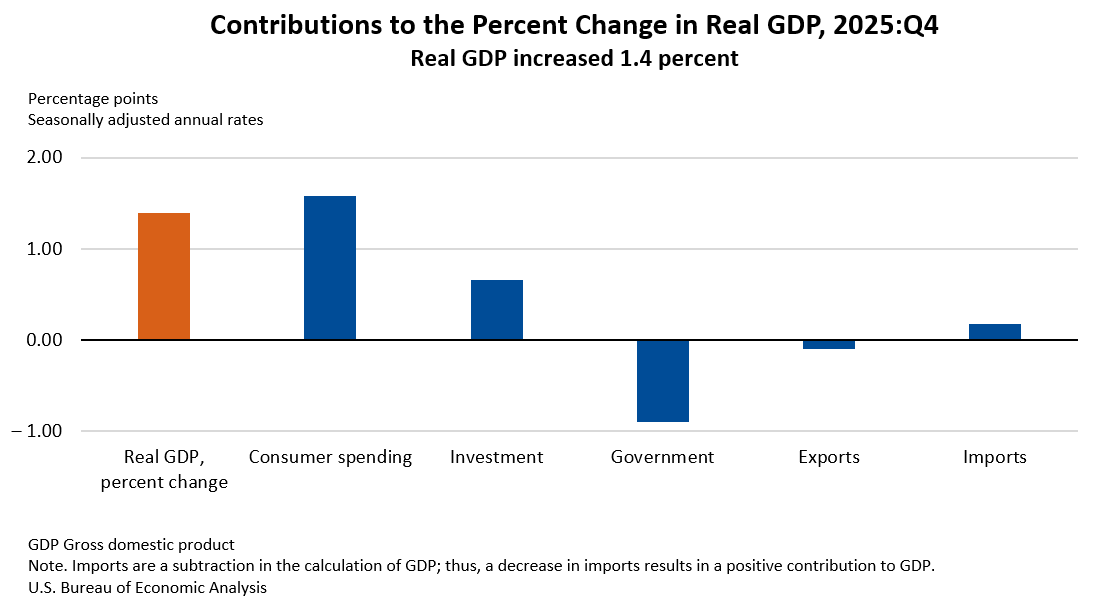

The slowdown in GDP growth during the final quarter of 2025 was influenced by a confluence of factors. While consumer spending and investment provided upward momentum, these were partially counteracted by declines in government expenditures and exports. Notably, imports, which are subtracted in the calculation of GDP, also decreased, further contributing to the net growth figure. This pattern of growth, with private sector demand being a primary driver but government and international trade sectors showing contraction, paints a complex picture of the economic landscape at the close of 2025.

Economic Performance in the Fourth Quarter of 2025

The 1.4 percent annual growth rate in real GDP for the fourth quarter of 2025 represents a notable shift from the preceding quarter’s performance. In the third quarter, the economy had surged by 4.4 percent, indicating a strong post-summer economic expansion. The deceleration in the fourth quarter suggests a recalibration of economic forces, with some sectors experiencing headwinds.

Key components of the GDP calculation revealed specific trends. Consumer spending, a cornerstone of the U.S. economy, continued to contribute positively, as did investment. However, the extent of their contribution was tempered by contractions in government spending and a decrease in the value of exports. Imports, which represent spending on foreign goods and services by domestic consumers and businesses, also declined. This reduction in imports, while contributing positively to the GDP calculation as a subtraction, also signals potentially softer domestic demand or shifts in global supply chains.

The BEA’s report highlighted that the deceleration from the third to the fourth quarter was largely due to downturns in government spending and exports, coupled with a slower pace of consumer spending growth. Conversely, investment experienced an acceleration, providing a partial offset to the moderating factors. The decrease in imports was less pronounced than in the prior quarter, indicating a stabilization in this component.

Real Final Sales to Private Domestic Purchasers

A closely watched metric that gauges the underlying strength of domestic demand is real final sales to private domestic purchasers. This measure, which comprises consumer spending and gross private fixed investment, provides a clearer view of the economy’s performance independent of inventory fluctuations and international trade. In the fourth quarter of 2025, real final sales to private domestic purchasers increased by 2.4 percent. While this represents continued expansion, it also shows a deceleration from the 2.9 percent increase observed in the third quarter, reinforcing the narrative of a slowing economic tempo.

Inflationary Pressures

Alongside the GDP figures, the BEA also reported on price developments. The price index for gross domestic purchases, which measures price changes for goods and services purchased by domestic entities, rose by 3.7 percent in the fourth quarter. This represents an acceleration from the 3.4 percent increase seen in the third quarter, indicating a pickup in inflationary pressures.

The Personal Consumption Expenditures (PCE) price index, a key inflation gauge closely monitored by the Federal Reserve, increased by 2.9 percent in the fourth quarter, up from 2.8 percent in the third quarter. This suggests a slight uptick in consumer price inflation. However, when excluding the volatile food and energy components, the core PCE price index saw a deceleration, increasing by 2.7 percent compared to 2.9 percent in the prior quarter. This divergence between headline and core inflation figures could present a nuanced challenge for policymakers.

Annual Economic Performance in 2025

Looking at the full year 2025, real GDP increased by 2.2 percent compared to the 2.8 percent growth recorded in 2024. This annual slowdown indicates a moderation in the economy’s overall expansion trajectory over the course of the year. The primary drivers for the 2025 annual growth were again attributed to increases in consumer spending and investment.

On the inflation front, the price index for gross domestic purchases increased by 2.6 percent in 2025, a slight acceleration from the 2.4 percent increase in 2024. The PCE price index also saw a 2.6 percent increase, mirroring the inflation rate from the previous year. The core PCE price index, however, showed a slight deceleration, rising by 2.8 percent in 2025 compared to 2.9 percent in 2024, suggesting some easing of underlying inflationary pressures in the broader economic context.

Impact of the Government Shutdown

The government shutdown, which commenced in October 2025 and lasted until mid-November, cast a significant shadow over the economic data collection and reporting process. The delay in the GDP release, initially scheduled for January 29, 2026, was a direct consequence of this federal impasse. Beyond the logistical challenges, the shutdown had tangible economic implications.

The BEA’s technical notes revealed that the shutdown’s effects on the fourth-quarter estimates were embedded within the source data and could not be entirely isolated. However, the BEA did estimate the impact of a reduction in labor services provided by federal employees. This reduction in government services is estimated to have subtracted approximately 1.0 percentage point from the real GDP growth in the fourth quarter. This suggests that without the disruption of the shutdown, the reported 1.4 percent GDP growth could have been significantly higher, potentially reaching closer to 2.4 percent. The back pay received by furloughed federal employees meant that the shutdown had no impact on current-dollar federal compensation, though it was reflected as a temporary increase in the prices paid for federal employee compensation.

The shutdown also affected the collection of price data. The Bureau of Labor Statistics (BLS) was unable to collect October 2025 Consumer Price Index (CPI) data due to the lapse in federal appropriations. To address this, the BEA imputed missing October price indexes using the geometric mean of the September and November CPIs for seasonally adjusted data, and by applying seasonal adjustment factors from October 2024 to the imputed seasonally adjusted values for October 2025 for non-seasonally adjusted data. These imputation methods are designed to provide the most accurate estimates possible under challenging circumstances, though they introduce a degree of estimation uncertainty.

Analysis and Implications

The 1.4 percent GDP growth in the fourth quarter of 2025, while positive, signals a cooling of economic momentum from the preceding quarter. The interplay of robust consumer spending and investment, counterbalanced by contractions in government activity and exports, highlights the evolving dynamics of the U.S. economy. The impact of the government shutdown, estimated to have shaved a full percentage point off growth, underscores the fragility of economic data dissemination and the real-world economic consequences of political instability.

The pickup in headline inflation, as measured by the gross domestic purchases price index and the PCE price index, warrants attention. While the core PCE price index showed some moderation, the overall inflationary trend could influence monetary policy decisions by the Federal Reserve. Policymakers will be closely observing whether the current inflationary pressures are transitory or indicative of more persistent trends.

The moderation in annual GDP growth for 2025, from 2.8 percent in 2024 to 2.2 percent, suggests a gradual return to a more sustainable growth path after a period of potentially stronger recovery. This slower pace could be interpreted as a sign of economic maturity or a response to prevailing economic headwinds, including persistent inflation and the lingering effects of the government shutdown.

The BEA’s ongoing efforts to modernize its news release packages, including the transition to online interactive data tables and the discontinuation of PDF and Excel tables, reflect a commitment to efficiency and accessibility. This shift aims to provide users with direct access to the most up-to-date and comprehensive data, streamlining the dissemination process for critical economic indicators.

Future Outlook and Next Steps

The economic outlook for the initial months of 2026 will be closely tied to the resolution of lingering economic challenges and the effectiveness of policy responses. The BEA’s next release, the second estimate for the fourth quarter of 2025 and the full year 2025, is scheduled for March 13, 2026. This release will incorporate additional data and provide a more refined picture of the economic performance during the final quarter of the year. Subsequent releases will continue to offer insights into the ongoing economic trajectory, with particular attention being paid to inflation trends, consumer spending patterns, and the impact of any future legislative or policy developments. The ability of the U.S. economy to navigate these complexities and maintain a stable, albeit moderated, growth trajectory will be a key focus for economists, policymakers, and investors in the coming year.