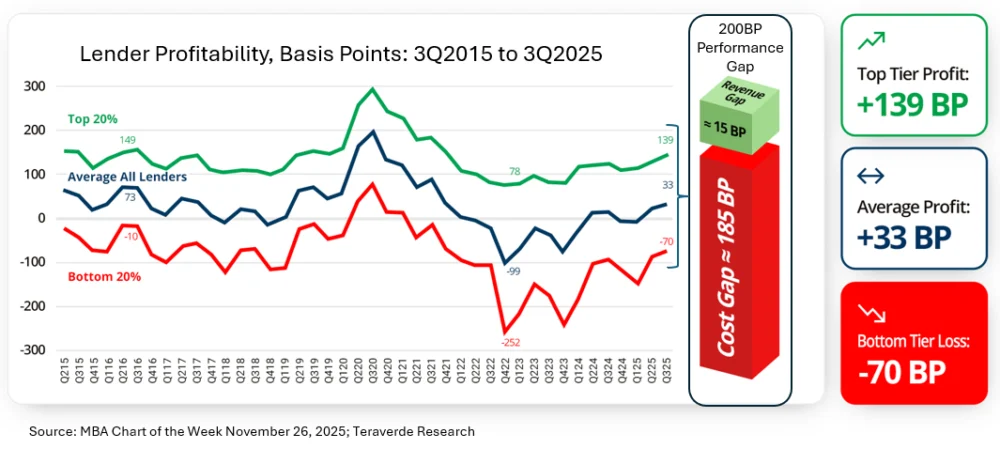

A decade of meticulous MBA Quarterly Performance Reports has laid bare a persistent and deeply concerning reality within the mortgage industry: a widening performance chasm between top-tier and bottom-tier lenders, a gap that has remained stubbornly fixed at approximately 200 basis points. This isn’t a fleeting market fluctuation; the data, spanning numerous economic cycles and market conditions, points to a fundamental structural issue that many industry players have yet to fully confront or effectively address. As of the quarter ending September 30, 2025, the top 20% of lenders, often referred to as "TopTier®" performers, consistently achieved a pre-tax production income of 139 basis points. In stark contrast, the average lender scraped by with a mere 33 basis points, while the bottom 20% found themselves operating at a deficit, losing an average of 70 basis points on their production.

This enduring disparity, documented over ten years of comprehensive data analysis by the Mortgage Bankers Association (MBA), suggests a systemic problem that transcends the cyclical nature of interest rates or market demand. It highlights a fundamental divergence in operational efficiency, strategic execution, and profitability models that distinguishes the industry’s elite from the struggling majority. The implications are profound, suggesting that the challenges faced by the average and underperforming lenders are not temporary setbacks but rather deeply ingrained issues that require more than just cyclical market recovery for resolution.

The Unforgiving Landscape of Mortgage Origination Profitability

The latest MBA data for the third quarter of 2025 paints a stark picture of the current profitability landscape. The industry-average pre-tax production profit stood at a modest 33 basis points, translating to approximately $1,201 per loan. While this figure might appear acceptable at first glance, it falls short of the long-run quarterly average since 2008, which hovers around 40 basis points. Furthermore, this current average emerges from an unprecedented period of sustained losses. The industry endured nine consecutive quarters of net production losses within a three-year span. In 2023 alone, the average lender experienced a loss of $1,056 on every single loan originated. Even as recently as the first quarter of 2025, the industry average remained in negative territory, with lenders losing an average of $28 per loan.

Adding to this challenging environment, a recent study on the "Cost to Originate" conducted by Freddie Mac for the second quarter of 2025 revealed that the average retail-only lender incurred approximately $11,800 in expenses to produce a single mortgage. This figure represents a significant escalation, with origination costs rising by roughly 35% over the preceding three years.

In plain terms, these financial metrics reveal a critical imbalance. The average lender is spending nearly $12,000 to originate a loan, only to pocket approximately $1,200 in pre-tax profit. This leaves a razor-thin margin for error and reinvestment. Meanwhile, the top-performing quintile of lenders are not only covering these costs but are generating profits that are multiples of this average figure. Conversely, the bottom quintile is effectively subsidizing their operations through losses, a financially unsustainable model that forces them to "write a check" simply to remain in business. This ongoing financial drain on underperforming lenders raises significant concerns about their long-term viability and the potential for market consolidation.

The Internal Divide: Performance Gaps Within Every Organization

Beyond the aggregate industry figures, a more uncomfortable and consequential truth emerges: the performance stratification observed at the industry level is often replicated within individual lending institutions. This internal performance gap, though less frequently discussed, is arguably more impactful on a company’s bottom line.

When contribution margin is meticulously tracked at the loan officer level – which involves comparing the all-in net revenue generated by a producer against their total compensation and associated downstream costs – a consistent pattern surfaces. The top 20% of originators and operations staff, the "TopTier®" contributors, are disproportionately responsible for generating the vast majority of a company’s profits. The middle tier of employees typically operates at or near break-even economics, contributing neither significantly to profits nor losses. The bottom tier, however, consistently underperforms. This underperformance manifests in various ways, including low unit volume, aggressive pricing concessions to win business, a higher incidence of defects and rework, loan fallout, and low pull-through rates (the percentage of locked loans that ultimately close).

A particularly counterintuitive and often overlooked finding is that the loan officers generating the highest volume are not always the most profitable. While high volume is readily visible and can create a sense of accomplishment, it does not inherently translate to superior profitability. Contribution margin per loan, while less emotionally satisfying and more difficult to track, is the true determinant of a company’s financial success. It is this metric, rather than sheer volume, that dictates whether a company achieves top-quintile returns or inadvertently subsidizes its underperforming staff by leveraging the efforts of its most productive individuals. This dynamic can create internal friction and resentment if not properly managed and incentivized.

The Structural Trap: Escalating Costs Amidst Declining Volume

The persistent cost pressures faced by mortgage lenders can be traced back to fundamental shifts in the industry’s cost structure, particularly concerning compensation and operational expenses. For the past decade, compensation has consistently represented between 65% and 70% of the total direct cost associated with originating a residential mortgage. This ratio has remained remarkably stable, even as market conditions have fluctuated dramatically.

Compounding this issue is the structural imbalance between workforce size and origination volume. The Bureau of Labor Statistics estimates that approximately 295,000 individuals are currently employed in core mortgage lending and brokerage roles. While this number has declined from its peak during the boom years of 2020-2021, the reduction has not been proportionate to the significant drop in origination volume. Industry origination volume, which surpassed $4 trillion in 2021, is now forecasted by the MBA to be around $2.2 trillion for 2026 – roughly half of its peak.

The arithmetic is straightforward: when two-thirds of the cost base is compensation, and unit volume is halved, with headcount lagging behind this decline, the cost per loan inevitably rises. This is precisely what has occurred. MBA data indicates that total production expenses per loan have surged to $11,109 in Q3 2025, a substantial increase from the long-run average of $7,799 since 2008. Critically, non-commission costs – including technology investments, compliance expenditures, operational overhead, and general administrative expenses – have grown at a disproportionately faster rate than originator compensation per loan. This suggests that efficiency gains and cost management in these ancillary areas have not kept pace with the need to absorb fixed compensation costs across a reduced volume of loans.

When industry leaders articulate a need for "more revenue per loan," the underlying message often translates to a simpler, and perhaps less sophisticated, demand: borrowers must be charged higher interest rates and fees. This strategy is frequently employed not because of a genuine increase in the value proposition or a surge in market demand, but because lenders have failed to adequately restructure their cost base to align with the new volume realities. This approach can alienate borrowers and create competitive disadvantages, especially in a market where price sensitivity is high.

Strategies of the Top Quintile: Operational Discipline and Unit Economics

The top 20% of lenders, those consistently achieving top-quintile performance, are not immune to the external pressures that affect the entire industry. They face the same economic cycles, interest rate volatility, and regulatory scrutiny as their peers. However, their sustained success stems from a distinct advantage: an unwavering commitment to operational discipline applied at the unit-economic level.

While specific strategies may vary, several common threads define their approach:

- Rigorous Cost Management: Top-tier lenders demonstrate an exceptional ability to control and optimize their cost structure. This involves not just monitoring compensation but also aggressively managing operational expenses, technology investments, and overhead. They actively seek efficiencies and regularly re-evaluate vendor contracts and internal processes to eliminate waste.

- Focus on Contribution Margin: Unlike many competitors who prioritize gross volume, top performers meticulously track and optimize their contribution margin per loan. This focus ensures that every loan originated is not only profitable but contributes meaningfully to the company’s overall financial health. They understand the nuances of pricing, borrower acquisition costs, and operational expenses for each loan.

- Strategic Technology Adoption: Leading lenders leverage technology not merely for automation but for enhanced efficiency, improved customer experience, and better data analytics. This includes sophisticated loan origination systems (LOS), customer relationship management (CRM) tools, and business intelligence platforms that provide real-time insights into performance metrics.

- Optimized Workforce Management: Top performers understand that high volume does not always equate to high profitability. They focus on building and retaining a high-performing team, often by implementing performance-based compensation structures that reward profitability per loan, not just origination numbers. They also invest in training and development to ensure their staff possesses the skills necessary to originate profitable business.

- Disciplined Pricing Strategies: While competitive, top lenders avoid the race to the bottom on pricing. They understand their cost base and market position to set prices that reflect value and ensure profitability, rather than simply trying to undercut competitors. This often involves offering value-added services or niche products that justify higher rates or fees.

- Efficient Operational Workflows: Streamlined and efficient operational processes are a hallmark of top lenders. This includes effective pipeline management, reduced cycle times, minimized rework, and robust quality control measures to reduce defects and loan fallout.

The Choice: Confronting the Mirror or Awaiting the Next Cycle

The evidence is clear: mortgage lending is not inherently a low-margin business. The performance of "TopTier®" lenders, consistently demonstrated over a decade that encompassed both a historic origination boom and a severe market contraction, proves that sustained profitability is achievable in any interest rate environment. The persistent 200-basis point performance gap is not an enigma; it is a tangible consequence of operational shortcomings, flawed compensation designs, and, ultimately, leadership that has failed to adequately address these challenges.

The data necessary to identify these performance issues is readily available, and the methods for correcting them are demonstrable. The critical question facing the remaining 80% of the mortgage industry is whether they will confront the reality of their internal disparities and operational inefficiencies – looking critically in the mirror – or continue to passively await the next market cycle, hoping it will magically resolve the problems that a decade of data has so clearly illuminated. The choice between proactive adaptation and passive waiting will likely define the future success or failure of countless lending institutions.

Jim Deitch is the CEO and Founder of Teraverde. This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.