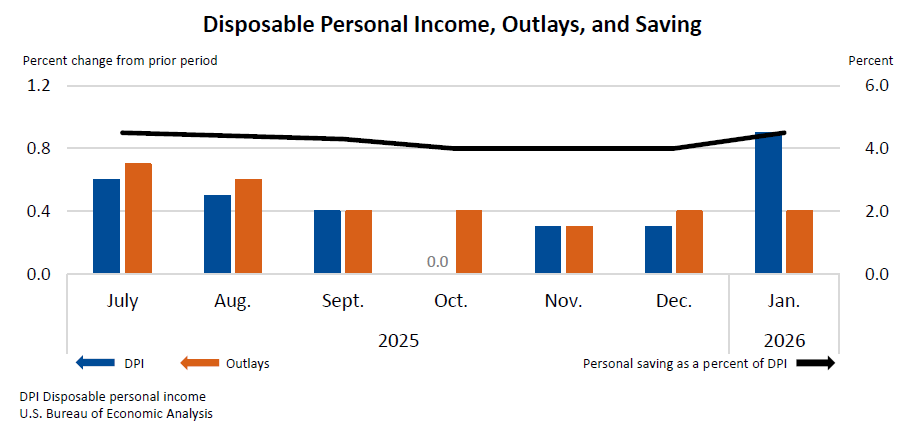

WASHINGTON D.C. – Personal income in the United States experienced a notable increase of $113.8 billion, or 0.4 percent at a monthly rate, in January, according to revised estimates released by the U.S. Bureau of Economic Analysis (BEA). This rise, primarily fueled by gains in compensation, personal dividend income, and personal current transfer receipts, signals continued economic momentum at the beginning of 2026. Concurrently, disposable personal income (DPI), the income remaining after taxes, saw a more substantial jump of $219.9 billion, or 0.9 percent, indicating a greater boost to households’ available funds.

The release of these crucial economic indicators for January 2026 was originally slated for February 26, 2026. However, the data submission and analysis timeline was significantly impacted by the protracted October-November 2025 government shutdown, which disrupted federal agency operations and data collection processes. This delay underscores the fragility of timely economic reporting in the face of governmental disruptions and highlights the challenges faced by agencies like the BEA in maintaining their regular release schedules.

In tandem with the income surge, personal consumption expenditures (PCE), a key measure of consumer spending, also expanded, increasing by $81.1 billion, or 0.4 percent. This growth in spending, while more subdued than the rise in disposable income, suggests that consumers are translating some of their increased earnings into economic activity. Personal outlays, which encompass PCE, personal interest payments, and personal current transfer payments, rose by $85.8 billion in January.

The personal saving rate, a critical gauge of household financial health and future spending capacity, stood at 4.5 percent in January, with personal saving totaling $1.05 trillion. While the saving rate remains a healthy level, the disparity between the growth in disposable income and the more modest increase in spending suggests a potential for further saving accumulation or a lag in consumer confidence translating fully into expenditure.

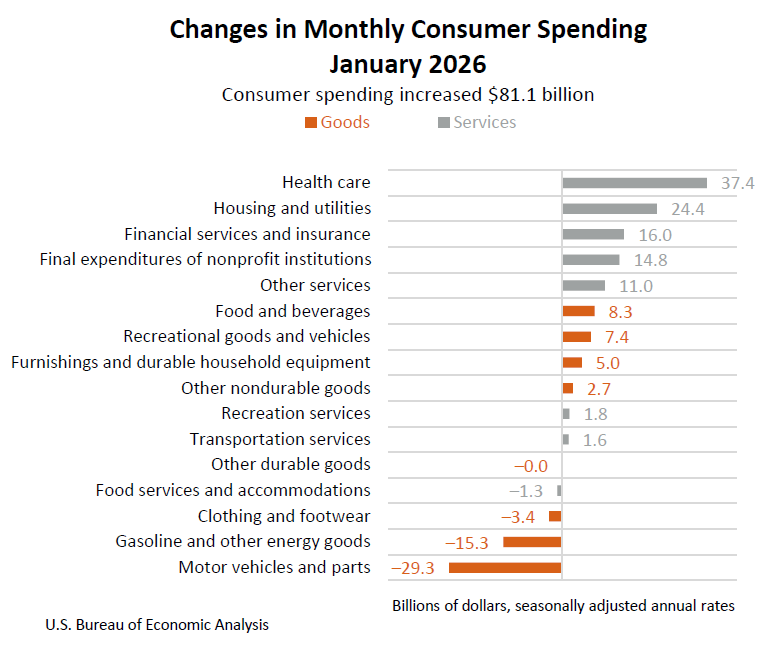

The January data also reveals a nuanced picture of consumer spending. The $81.1 billion increase in current-dollar PCE was largely driven by a $105.7 billion surge in spending on services. This expansion in the services sector, which includes areas like healthcare, recreation, and transportation, points to a resilient demand for these offerings. However, this growth was partially offset by a $24.6 billion decrease in spending on goods, suggesting a potential cooling or shift in consumer preferences away from tangible products.

On an inflation-adjusted basis, real PCE, which measures the volume of goods and services purchased, increased by $17.0 billion, or 0.1 percent, in January. This modest real spending growth indicates that while consumers are spending more in nominal terms, a portion of the increase is attributable to price changes.

Inflationary pressures, as measured by the Personal Consumption Expenditures (PCE) price index, showed a 0.3 percent increase in January compared to the preceding month. The core PCE price index, which excludes volatile food and energy prices and is closely watched by the Federal Reserve for underlying inflation trends, rose by 0.4 percent. These figures suggest that while inflation remains a concern, the pace of its increase may be moderating slightly in some categories.

Year-over-year, the PCE price index increased by 2.8 percent in January. The core PCE price index, excluding food and energy, saw a larger increase of 3.1 percent from the same month one year ago. These longer-term inflation figures indicate that while month-over-month increases might be stabilizing, overall price levels continue to be elevated compared to the previous year, posing an ongoing challenge for household purchasing power and monetary policy.

Impact of Government Shutdown on Data Release

The delayed release of the January 2026 Personal Income and Outlays report serves as a stark reminder of the potential economic consequences of governmental disruptions. The October-November 2025 government shutdown, which furloughed federal employees and halted non-essential government functions, created a ripple effect across various economic data collection and reporting cycles. The BEA, like many other federal agencies, faced significant operational challenges, including limited access to staff, data, and processing systems.

This delay not only postpones the availability of critical economic intelligence for policymakers, businesses, and the public but can also introduce a degree of uncertainty into economic forecasting. Timely and accurate data is paramount for informed decision-making, and any disruption to its flow can lead to a more reactive rather than proactive approach to economic management. The BEA has historically prioritized the accuracy and integrity of its data, and the rescheduling reflects a commitment to delivering reliable figures despite unforeseen circumstances.

Revisions to Past Data Reflect Enhanced Accuracy

In addition to the January figures, the BEA also released revised estimates for personal income from July through December 2025. These revisions are a routine part of the BEA’s statistical process, aimed at incorporating more comprehensive and up-to-date data as it becomes available. The incorporation of third-quarter wage and salary data from the Bureau of Labor Statistics (BLS) Quarterly Census of Employment and Wages program for the July-September period has refined estimates for compensation, personal taxes, and contributions for government social insurance. Furthermore, updated data from the BLS Current Employment Statistics (CES) program has informed the October-December estimates.

These revisions are crucial for providing a more accurate historical picture of economic activity and for ensuring the reliability of the current data. They demonstrate the BEA’s commitment to continuous improvement in its statistical methodologies and data sources, offering a more robust foundation for economic analysis.

Analysis of Key Economic Indicators

The January data presents a mixed but generally positive economic outlook. The robust growth in disposable personal income is a significant positive, suggesting that households have more funds at their disposal. The fact that this is outpacing the growth in consumer spending indicates that households may be either saving more, paying down debt, or are poised to increase spending in the coming months. The increase in personal saving to $1.05 trillion, while substantial, could be interpreted in multiple ways. It might reflect increased consumer confidence in future economic stability, allowing them to build a financial cushion. Alternatively, it could signal lingering caution due to persistent inflation or uncertainty about future income streams, prompting a more conservative approach to spending.

The divergence between the growth in services spending and the decline in goods spending is a noteworthy trend. This pattern has been observed in various economic cycles and can reflect a shift in consumer priorities. As economies mature and households become more affluent, there is often a greater allocation of resources towards experiences and services, such as travel, dining, and entertainment, rather than tangible goods. However, a sustained decline in goods spending could also signal concerns about the affordability of durable goods in an inflationary environment or saturation in certain consumer markets.

The PCE price index figures, particularly the core PCE, continue to be a focus for policymakers. While the month-over-month increase of 0.4 percent for the core index is not alarmingly high, it remains above the Federal Reserve’s target of 2 percent. The year-over-year increase of 3.1 percent for the core index reinforces the notion that inflation, though potentially moderating, is still a significant factor impacting the economy. This persistent inflation can erode purchasing power and necessitate continued vigilance from monetary authorities in managing interest rate policy.

Broader Economic Implications

The interplay between rising incomes, evolving consumer spending patterns, and persistent inflation has several implications for the broader economy. For businesses, understanding these trends is crucial for strategic planning. Companies in the services sector may see continued demand, while those focused on goods might need to adapt their product offerings or pricing strategies. The potential for increased consumer saving could also present opportunities for financial institutions and investment firms.

For policymakers, the data provides a complex landscape to navigate. The Federal Reserve will be closely monitoring inflation data, including the PCE price index, to inform its decisions on interest rates. A strong increase in disposable income, coupled with a moderate rise in real spending, might suggest that the economy can absorb current monetary policy without significant headwinds. However, persistent core inflation could warrant a more cautious approach to any easing of monetary policy.

Fiscal policymakers may also consider these trends. If consumer saving continues to rise, it could indicate less immediate need for broad-based fiscal stimulus. Conversely, if inflation continues to erode purchasing power, targeted relief measures for lower-income households might be considered.

The resilience of the U.S. economy, as evidenced by the continued growth in personal income and spending despite the challenges of a government shutdown, is a testament to its underlying strength. However, the persistent inflationary pressures and the nuanced shifts in consumer behavior highlight the ongoing need for careful economic management and informed policy responses.

Future Outlook and Next Steps

The next release of Personal Income and Outlays data, scheduled for April 9, 2026, at 8:30 a.m. EDT, will provide the February 2026 figures. This release will offer further insights into the continuation of these trends and any shifts in economic momentum. With the BEA’s ongoing modernization efforts, users are increasingly being directed to the agency’s Interactive Data Tables for the most up-to-date and comprehensive information, moving away from traditional PDF and Excel formats for news release tables. This transition aims to enhance accessibility and reduce data redundancy.

The BEA’s commitment to providing detailed breakdowns of personal income and consumption expenditures, including data on real versus nominal values and price indices, is essential for a thorough understanding of the U.S. economic landscape. As the economy continues to evolve, these timely and accurate reports will remain critical tools for assessing economic health and guiding future policy decisions. The integration of more comprehensive data through revisions and the strategic shift towards digital platforms underscore the BEA’s dedication to serving the needs of a data-driven economy.