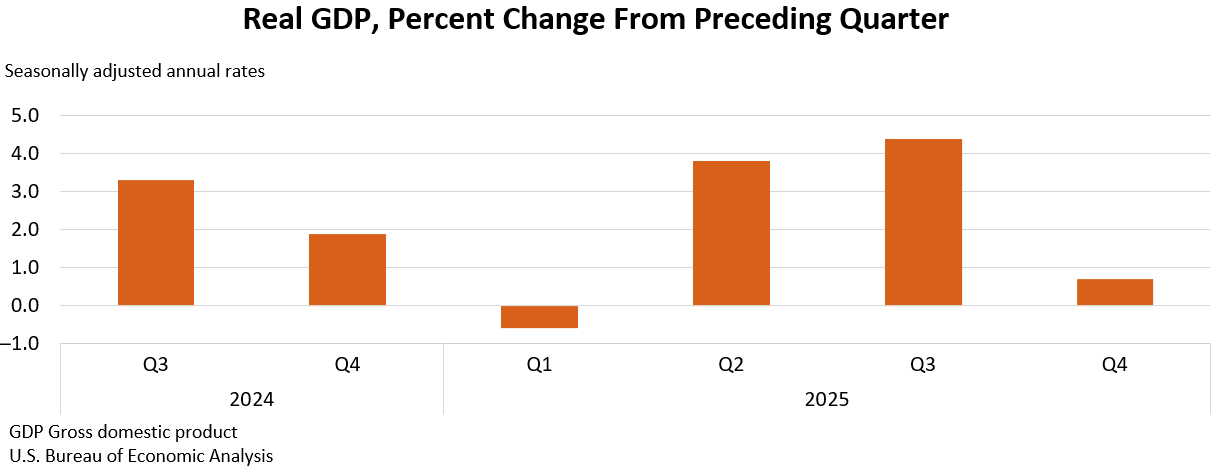

The U.S. economy demonstrated a notable slowdown in the fourth quarter of 2025, with real gross domestic product (GDP) expanding at a revised annual rate of just 0.7 percent. This figure, released by the U.S. Bureau of Economic Analysis (BEA) in its second estimate, represents a significant deceleration from the robust 4.4 percent growth recorded in the preceding third quarter. The downward revision from the advance estimate, coupled with the lingering effects of a prolonged government shutdown, paints a picture of an economy navigating a more challenging landscape as the year concluded.

The official release of the second GDP estimate for the fourth quarter of 2025, originally slated for February 26, 2026, experienced a delay. This postponement was directly attributed to the federal government shutdown that spanned October and November of 2025. The extended closure of various federal agencies disrupted data collection and processing, necessitating a rescheduled release to ensure the most accurate and comprehensive figures were presented. This unforeseen event introduced an element of uncertainty into the economic reporting calendar, underscoring the interconnectedness of government operations and economic indicators.

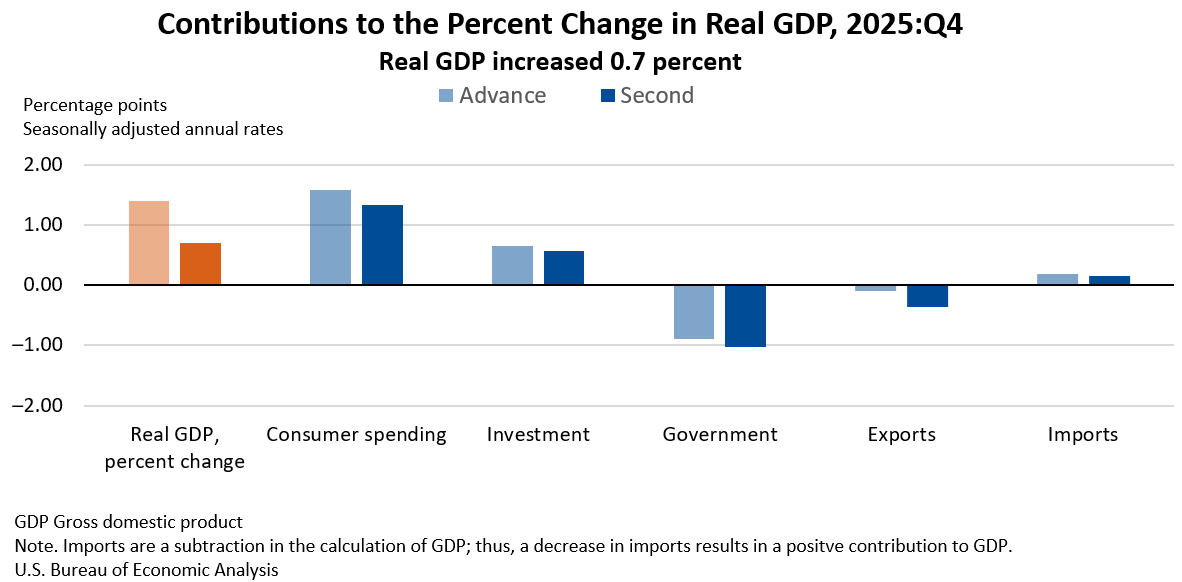

Driving the modest growth in the fourth quarter were increases in consumer spending and investment. These positive contributions, however, were significantly tempered by declines in government spending and exports. Imports, which are subtracted in the calculation of GDP, also decreased, further influencing the overall growth trajectory. The BEA’s second estimate revised real GDP downward by 0.7 percentage point from the initial advance estimate. This recalibration was largely due to downward adjustments in the figures for exports, consumer spending, government spending, and investment. Conversely, the decrease in imports was found to be less pronounced than initially reported, offering a slight counterbalancing effect.

A Quarter Marked by Deceleration and Shifting Dynamics

The marked deceleration in real GDP growth from the third quarter to the fourth quarter of 2025 can be attributed to several key shifts in economic activity. Downturns in government spending and exports played a substantial role in dampening overall growth. Furthermore, the pace of consumer spending, while still contributing positively, slowed compared to the previous quarter. Investment, on the other hand, experienced an acceleration, providing a partial offset to the broader slowdown. The reduction in imports, while a subtraction from GDP, was less significant in the fourth quarter than in the third quarter, indicating a potential stabilization or slight rebound in imported goods.

Real final sales to private domestic purchasers, a critical measure reflecting the demand from consumers and businesses for goods and services within the U.S., increased by 1.9 percent in the fourth quarter. This figure also saw a downward revision of 0.5 percentage point from the previous estimate, suggesting a slightly softer underlying demand than initially perceived. This metric is often viewed as a more stable indicator of domestic economic health, as it excludes the volatility often associated with exports and inventories.

Inflationary Pressures and Consumer Price Trends

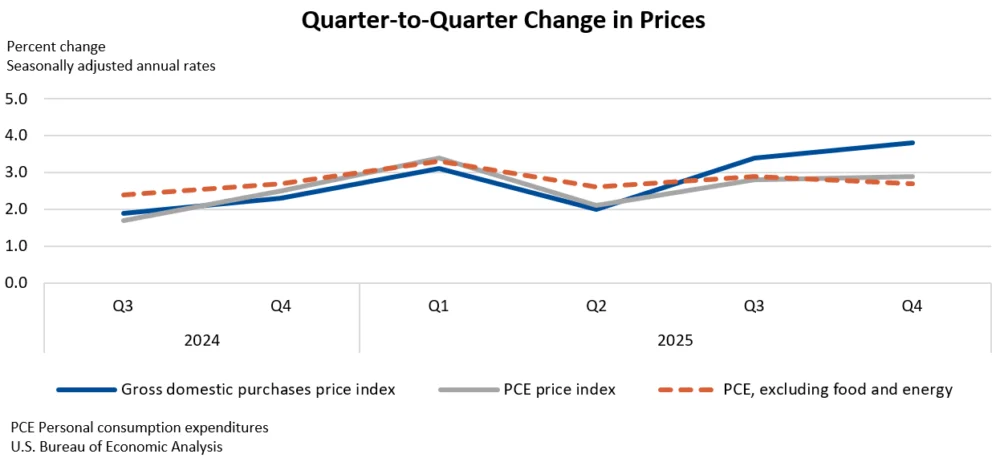

On the inflation front, the price index for gross domestic purchases, which measures price changes for all goods and services purchased by domestic entities, rose by 3.8 percent in the fourth quarter. This represented a slight upward revision of 0.1 percentage point from the advance estimate. The personal consumption expenditures (PCE) price index, a key inflation gauge closely monitored by the Federal Reserve, increased by 2.9 percent, remaining consistent with the initial estimate. Furthermore, the core PCE price index, which excludes volatile food and energy prices, also held steady at a 2.7 percent increase.

The BEA’s methodology for imputing missing price data for October 2025, due to the government shutdown affecting the Bureau of Labor Statistics’ (BLS) data collection, played a role in these estimates. The BEA derived October prices by using the geometric mean of the September and November Consumer Price Index (CPI) data. For non-seasonally adjusted prices, seasonal adjustment factors from October 2024 were applied to the imputed seasonally adjusted values for October 2025. This adjustment process is crucial for maintaining the integrity of the GDP estimates during periods of data disruption.

Annual Economic Performance in 2025

Looking at the full year of 2025, real GDP experienced an increase of 2.1 percent when comparing the annual average for 2025 to the annual average for 2024. This annual growth rate was revised downward by 0.1 percentage point from the previous estimate. The primary drivers of this annual expansion were the sustained increases in consumer spending and investment throughout the year.

The price index for gross domestic purchases for the full year 2025 increased by 2.6 percent, aligning with previous estimates. Similarly, the PCE price index also recorded a 2.6 percent increase for the year, and the core PCE price index (excluding food and energy) rose by 2.8 percent, both remaining consistent with earlier projections. These figures indicate a moderate inflationary environment for the year, with the Federal Reserve’s target of 2 percent for core PCE inflation remaining a key focus.

The Shadow of the Government Shutdown

The federal government shutdown, which extended from October 1 to November 12, 2025, cast a discernible shadow over the fourth-quarter economic data. While the full, granular impact of the shutdown on all sectors of the economy is inherently difficult to isolate, the BEA did provide an estimate for its effect on the labor services provided by federal employees. The agency estimated that a reduction in these services subtracted approximately 1.0 percentage point from real GDP growth during the fourth quarter.

Crucially, furloughed federal employees received back pay for the period of their furlough. This meant that the shutdown did not negatively impact current-dollar federal compensation. However, it was reflected as a temporary increase in the prices paid for federal employee compensation, as the government continued to incur costs for services not rendered during the shutdown. The BEA’s FAQ on how government shutdowns are reflected in GDP estimation methodologies provides further clarity on these complex accounting adjustments.

The disruption caused by the shutdown also extended to data collection processes, as noted with the BLS’s inability to collect October CPI data. The BEA’s reliance on imputation methods for missing data underscores the challenges faced in producing timely and accurate economic statistics during periods of government disruption. This event serves as a stark reminder of the potential economic ramifications of political impasses and their direct impact on the availability and reliability of crucial economic information.

Contributing Factors to GDP Changes in Q4 2025

The BEA’s detailed breakdown of contributions to real GDP growth in the fourth quarter reveals a mixed picture:

- Consumer Spending: Remained a positive contributor, though its pace decelerated compared to the third quarter. This suggests that while consumers continued to spend, their rate of expenditure growth softened. Factors influencing this could include persistent inflation, tighter credit conditions, or shifting consumer confidence.

- Investment: Showed an acceleration, indicating a rebound or increased business confidence in capital expenditures. This could be driven by factors such as technological advancements, anticipation of future demand, or strategic restocking efforts.

- Government Spending: Experienced a decrease, contributing negatively to GDP growth. This decline could reflect a winding down of pandemic-related stimulus measures, fiscal consolidation efforts, or the direct impact of the government shutdown on federal expenditures.

- Exports: Declined, acting as a drag on GDP. This could be attributed to a variety of global economic factors, including slower growth in major trading partners, currency fluctuations, or increased trade protectionism.

- Imports: Decreased, which, as a subtraction in GDP calculations, had a positive effect on the net GDP figure. However, the smaller decrease compared to previous estimates suggests a potential stabilization or a less severe contraction in import activity.

Broader Economic Implications and Outlook

The subdued GDP growth in the fourth quarter of 2025, coupled with the downward revisions, signals a more cautious economic environment as the year drew to a close. The deceleration, while partly explained by the extraordinary circumstances of the government shutdown, also points to underlying trends that may warrant closer observation.

The moderation in consumer spending, even with its continued positive contribution, could indicate a shift in household behavior as economic conditions evolve. The acceleration in investment, however, offers a more optimistic note, suggesting that businesses may be positioning for future growth. The interplay of these factors will be critical in shaping the economic outlook for 2026.

Inflationary pressures, as indicated by the price indexes, remained a significant consideration. While core PCE inflation showed stability, the overall gross domestic purchases price index saw a slight upward revision. The Federal Reserve’s monetary policy decisions will undoubtedly be influenced by these inflation trends and the broader trajectory of economic growth.

The BEA’s commitment to modernizing its news release packages, including the shift towards online interactive data tables and the discontinuation of PDF and Excel tables, aims to improve accessibility and efficiency for data users. This transition reflects a broader trend towards digital dissemination of economic information.

The next release of GDP data, scheduled for April 9, 2026, will provide the third estimate for the fourth quarter and full year 2025, along with GDP by Industry and Corporate Profits. This upcoming report will offer further insights into the accuracy of the current estimates and any subsequent adjustments that may be necessary, especially in light of the complexities introduced by the government shutdown and its impact on data collection. Economists and policymakers will be closely watching these figures to gauge the resilience of the U.S. economy and anticipate future trends in the face of evolving domestic and global economic forces. The ability of the economy to rebound from the disruptions of late 2025 and sustain a healthy growth trajectory will be a key narrative for the year ahead.