The latest edition of the European Tax Policy Scorecard (ETPS) for 2025 reveals Estonia’s continued leadership in fostering a competitive and neutral tax environment, a critical asset as the European Union navigates an era of significant fiscal challenges and strategic priorities. This comprehensive evaluation, which assesses 32 European countries, underscores the profound impact of national tax codes on economic performance and highlights both exemplary models and areas urgently needing reform across the continent. The findings arrive at a pivotal moment for the EU, with Member States facing mounting pressure to increase defense spending in response to Russia’s ongoing war in Ukraine, accelerate the green and digital transitions, accommodate potential enlargement, and manage the escalating debt payments from the NextGenerationEU recovery package.

The Evolving Fiscal Landscape of the European Union

The economic dynamics of national tax systems extend to the supranational level, profoundly influencing the EU’s collective ability to achieve its ambitious political and economic objectives. While taxation remains primarily a national prerogative, the Union’s long-term goals necessitate robust and stable government revenues, coupled with substantial private capital investment. The commitment to enhance defense capabilities, for instance, requires significant financial resources that can only be sustainably generated through efficient and growth-oriented tax systems. Similarly, the ambitious targets for green and digital transformations, aimed at future-proofing Europe’s economy, depend heavily on creating an attractive environment for private sector innovation and investment, which competitive tax policies can greatly facilitate.

Moreover, the prospect of EU enlargement, potentially incorporating new members, will place further demands on the Union’s budget and institutional frameworks, emphasizing the need for robust fiscal foundations. Adding to these pressures is the increasing burden of debt payments associated with the NextGenerationEU package, a crucial financial instrument adopted to mitigate the economic fallout of the COVID-19 pandemic. As the EU increasingly asserts an active role in both direct and indirect taxation, exploring new "Own Resources" for its budget, and even contemplating a harmonized "28th corporate tax regime" to deepen the Single Market, the imperative for data-driven policymaking, as provided by the ETPS, becomes undeniably clear. The Treaty on the Functioning of the European Union (TFEU) explicitly links tax policy to the smooth functioning of the single market, suggesting that harmonization, when principled and not merely a "least common denominator" compromise, can yield significant benefits.

The European Tax Policy Scorecard: A Framework for Evaluation

The European Tax Policy Scorecard serves as a vital analytical tool, measuring the extent to which a country’s tax system embodies the twin pillars of sound tax policy: competitiveness and neutrality. A competitive tax code is characterized by low marginal tax rates, recognizing capital’s high mobility in a globalized economy. Businesses actively seek jurisdictions where investment yields the highest after-tax returns. Exorbitant tax rates risk deterring foreign direct investment, impeding domestic capital formation, and ultimately stifling economic growth. High marginal rates can also inadvertently foster tax avoidance strategies.

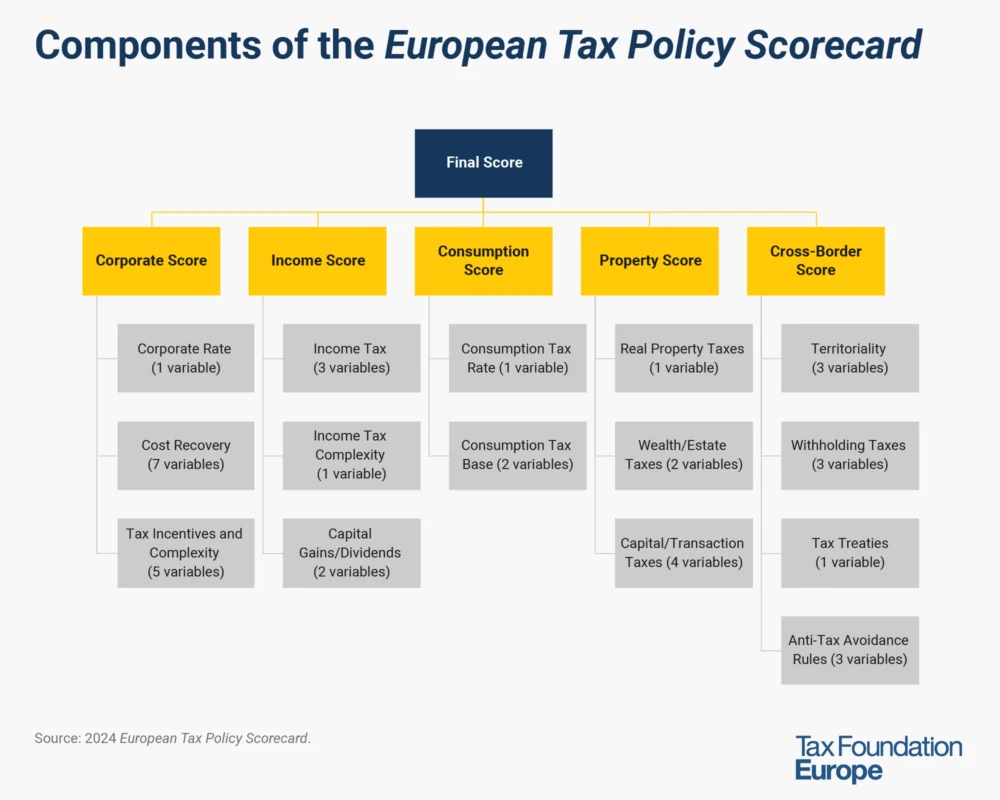

Neutrality, on the other hand, describes a tax code designed to maximize revenue with minimal economic distortions. This means avoiding biases that favor consumption over saving or certain activities over others. Complex tax laws, replete with targeted breaks or incentives, invariably undermine neutrality, creating opportunities for some businesses or individuals to gain tax advantages by altering their economic behavior. Research from the OECD consistently indicates that corporate taxes are the most detrimental to economic growth, followed by personal income and consumption taxes, while taxes on immovable property have the least impact. The ETPS, by examining 40 tax policy variables across five categories—corporate income taxes, individual income taxes, consumption taxes, property taxes, and cross-border tax rules—provides a comprehensive, data-driven overview.

The scorecard’s scope extends beyond EU Member States to include key European OECD countries like Iceland, Norway, Switzerland, Turkey, and the United Kingdom. This broader perspective offers Brussels policymakers invaluable insights into the tax policies of crucial regional partners and the potential ripple effects of their own decisions. The 2025 edition incorporates the most up-to-date data available as of July 2025, though rapid reforms enacted by some countries might not yet be fully reflected.

Estonia’s Enduring Leadership and Other Top Performers

For 2025, Estonia once again secures the highest ranking in the ETPS, a testament to its remarkably competitive and neutral tax system. This top score is underpinned by several distinctive features:

- A flat 22 percent corporate income tax rate applied exclusively to distributed profits, effectively deferring taxation until profits are paid out.

- A flat 22 percent individual income tax that notably exempts personal dividend income, further reducing the burden on capital.

- A property tax system that applies solely to the value of land, avoiding disincentives for improvements to real property or capital.

- A robust territorial tax system, which fully exempts 100 percent of foreign profits earned by domestic corporations from domestic taxation, with minimal restrictions.

These features collectively position Estonia as a beacon for pro-growth tax policy, demonstrating how simplicity and low marginal rates can attract investment and foster economic dynamism.

Following Estonia, Cyprus ranks second, largely due to its low corporate tax rate of 12.5 percent and the provision of an allowance for corporate equity (ACE), which helps to neutralize the debt-equity bias. Cyprus also boasts a broad-based consumption tax, while notably refraining from levying property taxes and taxes on capital gains from listed shares. Its low 3 percent withholding tax on dividends further enhances its appeal to investors.

Switzerland, securing the third position, impresses with a relatively low corporate tax rate of 19.6 percent and a broad-based value-added tax with a modest standard rate of 8.1 percent. Its individual income tax system partially exempts capital gains from taxation, contributing to its strong performance.

Other top-ranking countries, such as Latvia (4th), Malta (5th), and Bulgaria (6th), also achieve high scores through excellence in one or more major tax categories, illustrating diverse pathways to competitiveness and neutrality. Latvia, for instance, leads in corporate tax rankings, while Bulgaria excels in individual taxation with a low, flat rate.

Bottom Rankings: Identifying Systemic Weaknesses

Conversely, the ETPS identifies Italy and France as having the least competitive tax systems among the evaluated countries, primarily due to significant structural flaws and a high degree of complexity.

Italy, ranking last (32nd), struggles with multiple distortionary property taxes, including separate levies on real estate transfers, estates, and financial transactions, alongside a wealth tax on selected assets. Furthermore, Italy’s relatively high VAT rate of 22 percent is applied to a narrow consumption base, covering only 43 percent of total consumption, indicative of both policy shortcomings and enforcement challenges.

France, placing 31st, mirrors Italy’s issues with multiple distortionary property taxes, featuring levies on estates, bank assets, and financial transactions, complemented by a wealth tax on real estate. Critically, France imposes the highest top marginal corporate tax rate at 36.1 percent, a figure inflated by several surtaxes. The substantial tax burden on labor, with an average single worker facing a 47 percent levy, further diminishes its competitiveness.

The bottom-ranking countries generally exhibit higher-than-average combined corporate tax rates, typically ranging from 25 percent to 36.1 percent, and are plagued by complex tax rules. Four of the five lowest-ranked countries display this trend. Ireland, despite its often-cited low corporate tax rate, ranks poorly (27th) due to high personal income taxes, including a staggering 51 percent top dividends rate, and a relatively narrow VAT base. A common thread among these countries is the prevalence of complex corporate tax incentives, with the five lowest-ranking nations employing between two and six alternative corporate rates, significantly higher than the ETPS average of 1.8 percent. They also tend to have narrow VAT bases (43-56% of final consumption) and higher-than-average capital gains tax rates (26-34%, compared to an ETPS average of 17.7%).

Key Reforms and Notable Changes in 2025

The 2025 ETPS report highlights several significant tax reforms implemented by European countries in the past year, showcasing a dynamic policy landscape.

- Croatia (Improved from 17th to 15th): Croatia streamlined its personal income tax system by abolishing its municipal surtax and reducing the top rate from over 35 percent to 33 percent. It also introduced recurrent property taxes and broadened its VAT base, signaling a move towards a more balanced and efficient tax structure.

- France (Fell from 30th to 31st): France’s ranking deteriorated due to the introduction of a temporary surtax on corporate income for high-revenue companies, pushing its top marginal corporate rate to an alarming 36.1 percent—the highest in both Europe and the developed world. This move, likely driven by immediate revenue needs, risks undermining long-term competitiveness.

- Germany (Fell from 24th to 26th): Germany reinstated its accelerated depreciation schedule for machinery and equipment at a higher rate in mid-2025 and plans to reduce its corporate tax rate by 5 percentage points over five years starting in 2028. Concurrently, it expanded R&D tax subsidies. While some changes aim to boost investment, the complexity and temporary nature of some provisions, combined with the fall in rank, suggest a less coherent reform trajectory.

- Ireland (Improved from 28th to 27th): Ireland adopted a participation exemption for dividends received from abroad, transitioning towards a more territorial tax system. This significant reform aims to enhance its attractiveness for multinational corporations and align its international tax rules with global best practices.

- Portugal (Rose from 31st to 29th): Portugal implemented several positive changes, including lowering its long-term capital gains tax rate from 28 percent to 19.6 percent and reducing its top corporate tax rate from 31.5 percent to 30.5 percent. Additionally, it made its notional interest deduction more generous, indicating an effort to improve capital formation incentives.

- Slovak Republic (Fell from 10th to 14th): The Slovak Republic saw a notable decline in its ranking, primarily due to an increase in its corporate tax rate from 21 percent to 24 percent, an increased VAT registration threshold, and the introduction of a financial transaction tax. These measures, while potentially boosting revenue in the short term, are likely to dampen its competitiveness.

These shifts illustrate the ongoing tug-of-war between national revenue requirements and the desire to maintain or enhance economic competitiveness within the broader European context. Policymakers across the continent are continuously re-evaluating their tax regimes in light of both domestic pressures and international trends.

Deep Dive into ETPS Categories

Corporate Income Tax:

The ETPS assesses corporate tax systems based on their rates, cost recovery provisions, and the presence of distorting incentives and complexity. The average combined corporate income tax rate across ETPS countries in 2025 is 21.9 percent. France leads with the highest top corporate income tax rate at 36.1 percent, while Hungary boasts the lowest at 9 percent, followed by Bulgaria (10 percent) and Cyprus and Ireland (both 12.5 percent).

Cost recovery mechanisms, such as loss offset rules (carryforwards and carrybacks) and depreciation schedules, are crucial for accurately taxing profits rather than revenue. Ideally, tax codes allow unlimited loss carryforwards and provide accelerated depreciation. Currently, 18 of 32 ETPS countries allow indefinite loss carryforwards, though 12 limit the amount of taxable income that can be offset. Only Estonia and Latvia implicitly allow unlimited carrybacks due to their cash-flow corporate tax systems. The ETPS also evaluates capital allowances for machinery, industrial buildings, and intangibles, noting that countries like the UK and Lithuania are moving towards permanent full expensing for certain assets, while others like Finland and Germany have temporary provisions, creating uncertainty.

Tax incentives and complexity, such as patent boxes and R&D tax subsidies, are scrutinized for their potential to distort economic decisions. Sixteen ETPS countries operate patent box regimes, which, despite aims to attract intellectual property, are often criticized for shifting income rather than genuinely fostering innovation. Similarly, R&D tax incentives, while supporting innovation, can lead to inefficient resource allocation. Iceland offers the highest implied tax subsidy rate on R&D (36.5 percent), suggesting significant preferential treatment. The ETPS also penalizes countries with digital services taxes (DSTs), which are implemented by 11 ETPS countries, and those with multiple corporate tax rates or surtaxes, such as Portugal with its six different rates.

Individual Taxes:

Individual tax systems are evaluated based on the rate and progressivity of wage taxation, complexity, and the extent of double taxation on corporate income. Denmark imposes the highest top personal income tax rate at 55.9 percent (set to rise to 60.5% in 2026), followed by France (55.4 percent) and Austria (55 percent). Bulgaria and Romania maintain the lowest rates at 10 percent. The ETPS also considers the income level at which the top rate applies and the economic cost of labor taxation, measured by the marginal tax wedge ratio. Hungary’s flat tax system results in a ratio of 1, indicating uniform tax burden, while Spain, the Netherlands, and Italy exhibit the highest ratios, suggesting a greater impact on individuals’ decisions to earn additional income. Surtaxes on personal income, such as those in Germany and Luxembourg, contribute to complexity and are penalized by the scorecard.

Capital gains and dividends taxes represent a second layer of taxation on corporate profits. Ireland levies the highest dividend tax rate at 51 percent, whereas Estonia and Latvia have 0 percent rates due to their cash-flow corporate tax systems. Denmark has the highest capital gains tax rate at 42 percent, while several countries, including Cyprus and Switzerland, do not tax long-term capital gains from listed shares.

Consumption Taxes:

Consumption taxes, primarily VATs, are assessed on their rates and bases. The average general consumption tax rate in the ETPS is 21.5 percent. Hungary has the highest rate at 27 percent, while Switzerland boasts the lowest at 8.1 percent. The breadth of the consumption tax base is measured by the VAT revenue ratio, which indicates the efficiency of collection. Luxembourg has the broadest base, covering 82.2 percent of total consumption, while Turkey, Greece, and Italy have the narrowest (around 41-43 percent), pointing to significant exemptions or non-compliance. High VAT exemption thresholds, such as Romania’s, are also penalized for narrowing the tax base.

Property Taxes:

Property taxes encompass recurrent real property taxes, wealth and estate taxes, and various capital and transaction taxes on businesses. While generally considered efficient, real property taxes can become distortionary if they apply to structures and buildings in addition to land value. Estonia is the only country in the ETPS that exclusively taxes the value of land. Many countries, including Norway, Spain, and Switzerland, levy wealth taxes, and 23 countries impose estate, inheritance, or gift taxes, which are often criticized for their complexity and disincentives to saving. Taxes on property transfers, corporate assets, capital duties, and financial transactions (present in 14 ETPS countries, including France and the UK) further add to the cost of capital and impede market efficiency.

Cross-Border Tax Rules:

In a globalized economy, cross-border tax rules significantly influence investment. Territorial tax systems, which exempt foreign-earned income from domestic taxation, are generally favored over worldwide systems for their competitive advantages. Twenty-six ETPS countries fully exempt foreign-sourced dividends, and 25 fully exclude foreign-sourced capital gains, demonstrating a strong trend towards territoriality. Ireland’s recent adoption of a participation exemption for dividends marks a significant step in this direction. However, restrictions on eligible countries (present in 19 countries), such as blacklists or minimum tax rate requirements, introduce complexity.

Withholding taxes on dividends, interest, and royalties paid to foreign entities can increase investment costs. While Switzerland has high withholding rates, Estonia, Hungary, Latvia, and Malta levy no withholding taxes on dividends or interest. The size of a country’s tax treaty network is also a factor, as treaties reduce double taxation and withholding rates. The UK boasts the broadest network with 132 treaties, while Iceland has the smallest with 47. Finally, anti-avoidance rules, such as Controlled Foreign Corporation (CFC) rules and interest deduction limitations, aim to prevent aggressive tax planning but can add significant complexity. CFC rules are present in 31 of 32 ETPS countries, with Switzerland being the sole exception, reflecting a widespread effort to combat profit shifting.

Broader Implications and Future Outlook

The 2025 European Tax Policy Scorecard serves as a critical diagnostic tool, offering a detailed snapshot of Europe’s diverse tax landscapes. Its findings underscore the urgent need for policymakers to embrace tax reforms that prioritize competitiveness and neutrality, especially as the EU confronts a confluence of profound challenges. The Union’s strategic objectives – from bolstering defense capabilities and accelerating the green and digital transitions to managing substantial debt and contemplating future enlargement – are inextricably linked to the fiscal health and efficiency of its Member States.

The continued prominence of Estonia and other top-ranking countries demonstrates that simplified, lower-rate tax systems can effectively attract investment and foster economic growth without compromising revenue stability. Conversely, the struggles of countries like Italy and France highlight the pitfalls of overly complex, distortionary tax regimes that can deter capital and burden labor.

The ongoing debate within the EU regarding tax harmonization versus national sovereignty will undoubtedly be informed by these findings. While full harmonization remains a distant prospect, the ETPS provides a common framework for understanding best practices and identifying areas where coordinated reforms could yield collective benefits for the Single Market. Policymakers are increasingly recognizing that tax systems are not merely revenue-generating mechanisms but powerful levers for economic development. A data-driven approach, such as that provided by the ETPS, is indispensable for designing policies that balance the imperative for sufficient public funds with the critical need to stimulate private sector investment and sustainable growth. The future prosperity and strategic autonomy of the European Union will depend, in no small measure, on its ability to cultivate tax environments that are both robust and conducive to economic flourishing.