The vaping industry has experienced explosive growth in recent decades, solidifying its position as a significant market player that offers a less harmful alternative to traditional combustible cigarettes for individuals seeking to consume nicotine or transition away from smoking. This rapid expansion, however, has outpaced consistent regulatory and taxation frameworks, leading to a complex and often contradictory landscape across the United States. As of January 2026, 34 states and the District of Columbia have implemented excise taxes on vaping products, yet the structures and rates of these levies vary wildly, creating significant disparities in consumer cost and, consequently, in the effectiveness of these products as a harm reduction tool.

The Evolution of Vaping and its Regulatory Context

Vapor products, or electronic nicotine delivery systems (ENDS), first emerged in the early 2000s, initially as niche devices. Over time, they have evolved into a diverse category, encompassing a wide array of devices tailored to different user preferences. Open system devices, for instance, offer users considerable customization, allowing them to refill tanks with their chosen vaping liquids and select from a vast spectrum of flavors and nicotine strengths. This flexibility appeals to experienced users who appreciate the control over their vaping experience. In contrast, closed system products, characterized by pre-filled, disposable cartridges or pods, prioritize simplicity and convenience. These non-refillable units have gained immense popularity due to their ease of use, particularly among newer users. However, a significant challenge within the closed system market is that many of these products sold in the U.S. have not received authorization for sale from the Food and Drug Administration (FDA), creating a grey area in regulation and consumer access.

The FDA’s journey to regulate vaping products began in earnest with the Deeming Rule in 2016, which brought e-cigarettes and other ENDS under the agency’s authority, similar to traditional tobacco products. This rule mandated that all vaping products introduced after February 15, 2007, undergo a rigorous Premarket Tobacco Application (PMTA) process to demonstrate that they are "appropriate for the protection of public health." This extensive and costly application process has been a major hurdle for many manufacturers, particularly smaller businesses, limiting the range of FDA-authorized products available on the market. The slow pace of PMTA approvals, coupled with state-level bans on flavored products, has inadvertently contributed to the proliferation of unauthorized products and the growth of illicit markets, undermining both public health objectives and potential tax revenue collection.

A Patchwork of State Taxation

The fiscal landscape for vaping products is highly fragmented. State taxes on ENDS products vary significantly not only in their rates but also in their underlying structures. This variability makes it exceedingly difficult for consumers, retailers, and policymakers alike to compare the true cost burden across state lines. Some states opt for an ad valorem tax, levying a percentage on the manufacturer’s, wholesale, or retail price. This approach links the tax burden directly to the product’s value. Other states employ volume-based taxes, charging per milliliter of vaping liquid, or a per-cartridge tax, which directly correlates with the quantity of product. A few states have adopted a bifurcated system, applying different structures and rates for open and closed systems, acknowledging the distinct characteristics and market dynamics of each.

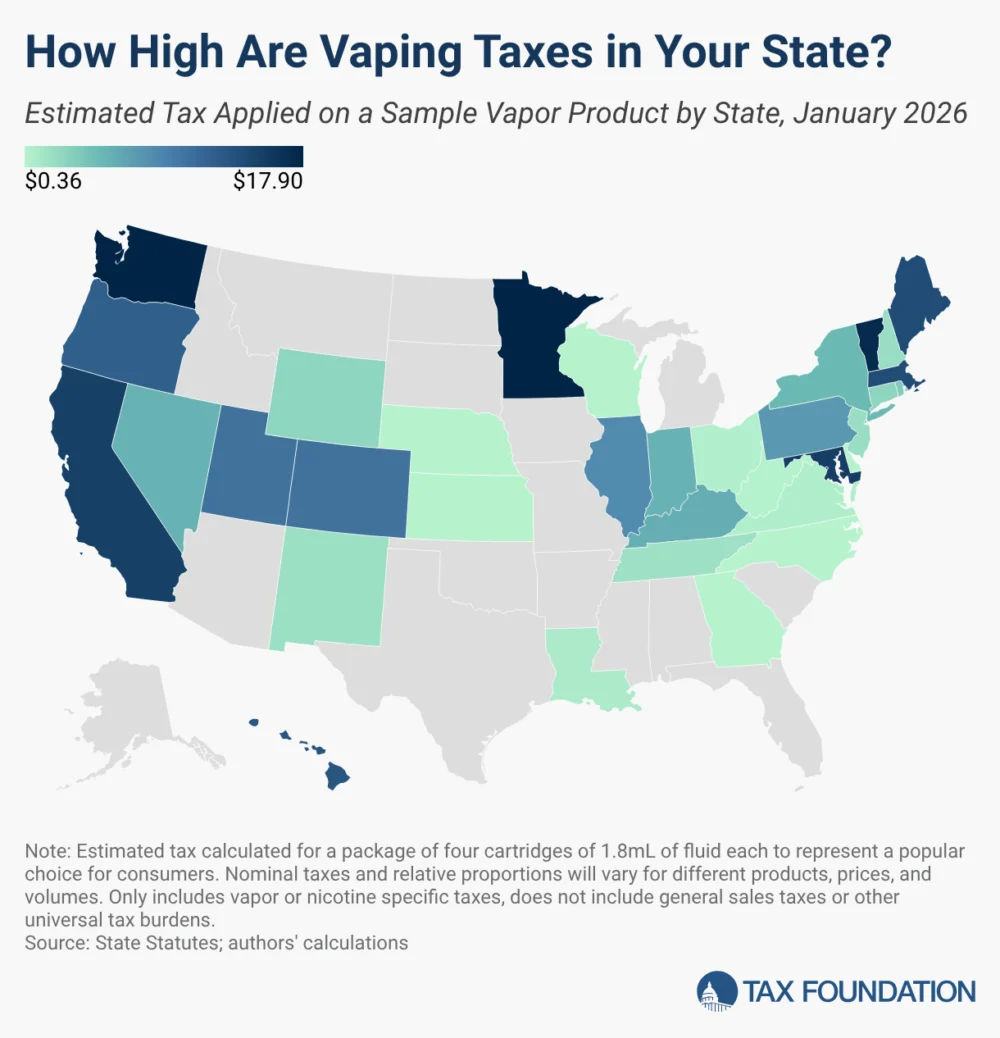

To provide a comparable assessment of the tax burden, analysts often calculate the tax on a standardized product. For instance, using a popular closed system product – a package of four 1.8mL vaping cartridges with a wholesale price of $18.84 – and assuming a 5 percent wholesale price markup and a 30 percent retail price markup, allows for a more direct comparison of state tax liabilities. This methodology reveals stark differences.

Specific Tax Burdens Across the Nation

The data as of early 2026 highlights a wide range of tax burdens. Minnesota and Washington currently impose the heaviest wholesale tax, a substantial 95 percent, closely followed by Vermont at 92 percent. These rates translate into significant consumer costs, potentially diminishing the appeal of vaping as a less expensive alternative to cigarettes. Conversely, some states apply notably lower wholesale taxes, particularly on open systems, such as Georgia at 7 percent and New Hampshire at 8 percent, reflecting a more lenient approach to taxation for these customizable products.

Retail taxes also show considerable variation. Maryland levies a high retail tax of 60 percent, while California’s retail tax stands at 12.5 percent, though this is in addition to a substantial 54.27 percent wholesale tax. This layering of taxes can create a complex pricing environment that is not immediately apparent to consumers.

Volume-based taxes present another dimension of this disparate landscape. Rhode Island leads with a tax of $0.50 per milliliter, followed by Connecticut at $0.40 per milliliter. New Hampshire and New Jersey impose $0.30 per milliliter on closed systems. States like Kentucky and New Mexico opt for a per-cartridge tax, at $1.50 and $0.50 per cartridge, respectively. These specific charges can accumulate quickly, particularly for frequent users.

When considering the overall tax burden, Minnesota and Washington emerge as having the greatest cumulative tax, reaching $17.90 for the benchmark product, which is equivalent to $2.49 per milliliter. This high burden is largely driven by their 95 percent wholesale tax. On the other end of the spectrum, states like Delaware, Georgia, Kansas, Nebraska, North Carolina, and Wisconsin tie for the lowest overall tax, at $0.36 for the same product, corresponding to a modest $0.05 per milliliter tax. It is crucial to note, however, that these relative burdens can shift depending on the specific product, as ad valorem taxes react to different price points, and industry markups can vary geographically.

The Public Health Imperative: Harm Reduction

Beyond revenue generation, the taxation of vaping products is inextricably linked to public health objectives, particularly the concept of harm reduction. Vaping products facilitate the delivery of nicotine, the addictive component found in cigarettes, without the combustion and inhalation of tar and thousands of other toxic chemicals inherent to traditional combustible cigarettes. While ongoing research into the long-term effects of vaping is essential, the overwhelming present scientific consensus indicates that vapor products are significantly less harmful than traditional cigarettes.

This consensus is reinforced by international public health bodies. Public Health England, part of the English Ministry for Health, famously concluded in 2015 that e-cigarettes are around 95 percent less harmful than tobacco. This finding was later corroborated by King’s College London, which, through the largest review of its kind, confirmed a substantial reduction in exposure to toxicants from vaping compared to smoking.

The stark disparity in health effects between vaping and smoking underscores the critical importance of integrating harm reduction principles into the design of excise taxes on vapor products. Harm reduction posits that it is more practical and effective to mitigate the harm associated with product use rather than attempting to eliminate that harm entirely through counterproductive policies such as ineffective bans or punitive levels of taxation. Vaping, while not entirely without risk, offers a dramatically less harmful pathway for nicotine consumption.

Economic Consequences and Behavioral Shifts

The economic relationship between traditional cigarettes and vaping products is crucial for policy design. Nicotine-containing products are economic substitutes; changes in the price or availability of one can directly influence the consumption of the other. Consequently, lower tax rates on vaping products can serve as an incentive for smokers to switch from more harmful combustible products. Conversely, excessively high excise taxes on these less harmful alternatives risk harming public health by creating a financial disincentive for vapers to maintain their switch, potentially pressuring them back to smoking.

A compelling case study illustrating this effect comes from Minnesota. Following the implementation of a 95 percent tax on vapor products, research found that this punitive tax deterred an estimated 32,400 smokers in the state from quitting cigarettes. This data point highlights a significant unintended consequence of high taxation: rather than encouraging cessation, it can inadvertently maintain or even increase smoking rates, thereby increasing the burden of smoking-related diseases.

Regulatory Quagmire and the Path Forward

The current regulatory landscape, characterized by the FDA’s stringent PMTA process and various state-level bans on unauthorized or flavored products, presents a significant impediment to realizing the full public health potential of harm reduction. These policies, while often well-intentioned to protect public health, particularly youth, can create unintended consequences. By limiting the availability of diverse, regulated products, they inadvertently foster the growth of illicit markets. Consumers, unable to access their preferred products legally, may turn to unregulated and untaxed illicit vapes, which pose unknown health risks dueade of any quality control. This not only undermines public health but also precludes significant tax revenue collection that could otherwise be channeled into health programs or other public services.

Industry representatives often argue that overly restrictive policies stifle innovation and consumer choice, pushing users towards riskier options. From a public health perspective, experts advocating for harm reduction emphasize the need for a balanced approach that protects youth while ensuring adult smokers have accessible, regulated, and appealing alternatives to deadly cigarettes. State treasury officials, on the other hand, face the ongoing challenge of generating revenue while navigating public health directives and a complex, evolving market.

Policy reform in this area represents a prime opportunity to bolster public health outcomes. By adopting more nuanced regulatory approaches that prioritize authorized, less harmful products and by designing tax structures that are proportionate to risk, states could simultaneously reduce lives lost to smoking, generate more stable and substantial tax revenue, and enable responsible growth in a market that consumers clearly support.

Designing an Equitable and Effective Tax System

Ultimately, if the overarching goal of taxing cigarettes is to encourage cessation and improve public health, then the taxation of vapor products must be considered an integral part of that broader policy design. An ideal tax structure for vapor products and other alternative nicotine products should fundamentally account for the relative harms of each alternative. This means implementing lower tax rates on products scientifically proven to be significantly less harmful than combustible cigarettes.

Such an approach would align economic incentives with public health objectives, encouraging a migration away from the most dangerous forms of nicotine consumption. It would also necessitate ongoing scientific review and adaptation of tax policies as new evidence emerges. Furthermore, effective tax design should prioritize simplicity, ease of administration, and robust enforcement mechanisms to minimize opportunities for illicit trade.

The ongoing debate surrounding vaping taxation is a microcosm of the broader challenge in public health policy: how to balance individual liberty and consumer choice with population-level health protection, particularly when dealing with addictive substances and evolving scientific understanding. As the vaping industry continues to mature and scientific evidence accumulates, policymakers face the critical task of developing cohesive, evidence-based regulatory and taxation frameworks that truly serve the public’s health in the long run.