The architecture of a nation’s tax code profoundly shapes its economic trajectory, influencing everything from compliance ease to investment attractiveness and revenue generation for public priorities. A well-designed tax system can catalyze economic development, ensuring adequate funding for governmental initiatives, whereas a poorly structured one can impose significant costs, distort economic decisions, and hinder domestic growth. These fundamental economic principles extend to the supranational sphere, particularly within the European Union, where an increasingly complex fiscal environment necessitates a data-driven approach to tax policy.

The Broader EU Fiscal Imperative

While taxation remains primarily a competence of individual EU Member States, the Union’s overarching political and economic objectives are becoming increasingly demanding and financially intensive. Facing escalating geopolitical tensions, exemplified by Russia’s ongoing conflict in Ukraine, the imperative for increased defense spending across Europe has become paramount. Simultaneously, the EU is committed to facilitating ambitious green and digital transitions, which require substantial public and private capital investment. Furthermore, the prospect of potential enlargement of the Union introduces additional fiscal considerations, and the repayment obligations for the NextGenerationEU pandemic recovery package will place considerable strain on national budgets in the coming years.

In response to these multifaceted challenges, the EU is adopting a more proactive stance on both indirect and direct taxation. This includes exploring new "Own Resource" ideas for the EU budget and developing a potential 28th corporate tax regime aimed at enhancing the efficiency and fairness of the Single Market. Such initiatives underscore the critical need for policymakers to base their decisions on robust, comparable data to avoid unintended consequences and ensure policy effectiveness. The Treaty on the Functioning of the European Union (TFEU) already guides EU tax policy towards the smooth functioning of the single market, implying that harmonization efforts should strive for principled policies that offer net benefits, rather than merely settling for the lowest common denominator among diverse national approaches. Understanding existing Member State policies is crucial to designing reforms that create more winners than losers.

Understanding the Metrics: Competitiveness and Neutrality

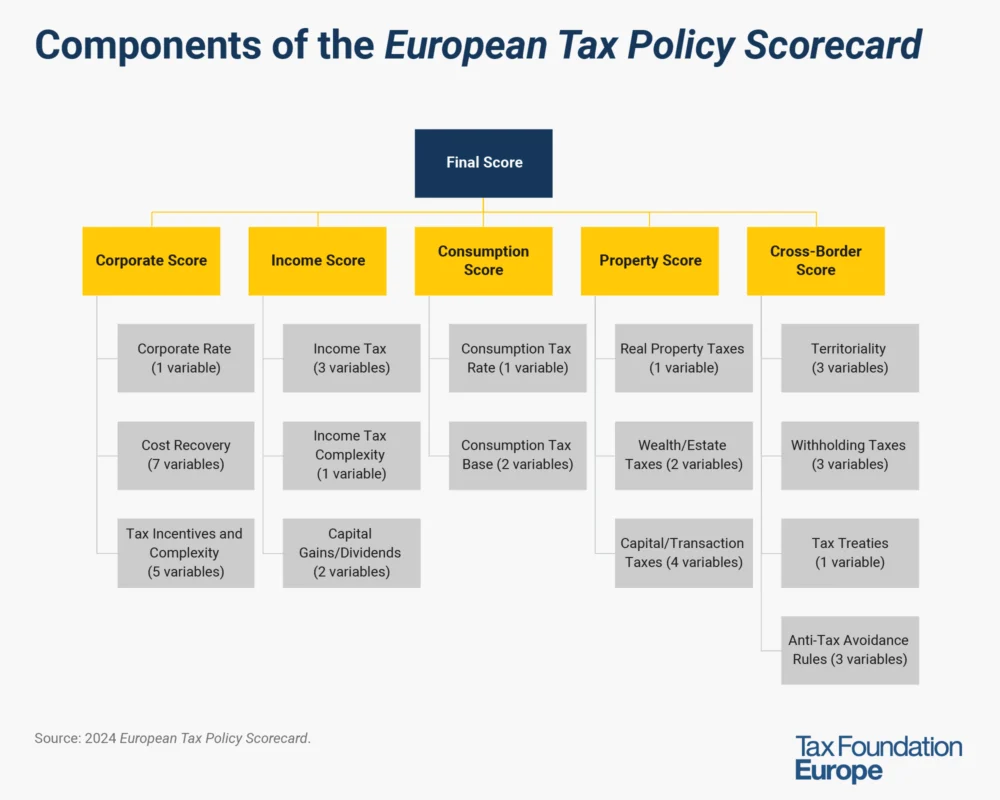

To provide this essential data-driven perspective, the European Tax Policy Scorecard (ETPS) offers a relative comparison of European countries’ tax systems. The ETPS evaluates tax systems based on two foundational aspects of sound tax policy: competitiveness and neutrality.

A competitive tax code is characterized by low marginal tax rates. In today’s highly globalized economy, capital is exceptionally mobile. Businesses have the flexibility to allocate investments across various countries in pursuit of the highest after-tax rate of return. Consequently, nations with excessively high tax rates on investment risk deterring capital, leading to slower economic growth and potentially encouraging tax avoidance. Competitive tax rates are thus crucial for attracting and retaining domestic and foreign investment. Research from the Organisation for Economic Co-operation and Development (OECD) consistently highlights corporate taxes as the most detrimental to economic growth, followed by personal income and consumption taxes, with recurrent taxes on immovable property having the least impact.

A neutral tax code, conversely, aims to maximize revenue generation while minimizing economic distortions. This implies a tax system that does not unfairly favor certain economic activities over others, such as consumption over saving (as wealth and investment taxes often do), and avoids granting targeted tax breaks to specific businesses or individuals. As tax laws grow in complexity, their neutrality often diminishes. If a tax system’s rules allow certain groups to alter their behavior to gain a tax advantage, it undermines the system’s inherent fairness and efficiency.

A tax code that successfully combines competitiveness and neutrality fosters sustainable economic growth and investment, all while securing sufficient revenue for governmental priorities. While many non-tax factors influence a country’s economic performance, taxation undeniably plays a pivotal role in a nation’s economic health. The ETPS utilizes 40 tax policy variables, scrutinizing not just tax rates but also tax structure across corporate, individual income, consumption, property, and cross-border tax rules. This comprehensive analysis offers a detailed comparative overview, identifying models for reform and providing critical insights for tax policy discussions. The ETPS primarily focuses on EU Member States but also includes key European OECD countries like Iceland, Norway, Switzerland, Turkey, and the United Kingdom, recognizing their significant economic ties with the EU.

2025 Rankings: Leaders and Laggards

For 2025, Estonia maintains its position at the top of the ETPS rankings, achieving a perfect score of 100. Its leading performance is underpinned by several distinctive features: a 22 percent corporate income tax rate applied only to distributed profits, a flat 22 percent individual income tax rate that exempts personal dividend income, a property tax levied solely on land value (excluding buildings or capital), and a robust territorial tax system that fully exempts foreign profits earned by domestic corporations with minimal restrictions.

Other top-performing countries achieve high scores through excellence in specific tax categories. Cyprus (rank 2) benefits from a low 12.5 percent corporate tax rate, an allowance for corporate equity (ACE), a broad-based consumption tax, and exemptions from property taxes and capital gains on listed shares. Its withholding tax on dividends is a mere 3 percent. Switzerland (rank 3) is noted for its relatively low corporate tax rate (19.6 percent), a broad-based value-added tax (VAT) at 8.1 percent, and an individual income tax system that partially exempts capital gains. Latvia (rank 4) and Malta (rank 5) also feature prominently, demonstrating strong performance in corporate and property tax categories, respectively.

Conversely, the least competitive tax systems in the ETPS are marked by significant flaws across one or more major categories. Italy ranks last (32nd) due to a multitude of distortionary property taxes, including levies on real estate transfers, estates, financial transactions, and a wealth tax on selected assets. Its 22 percent VAT rate is applied to a narrow consumption base, covering only 43 percent of consumption, indicative of both policy and enforcement deficiencies.

France (31st) follows closely with similarly distortionary property taxes, encompassing estates, bank assets, and financial transactions, alongside a wealth tax on real estate. France also imposes Europe’s highest top marginal corporate tax rate at 36.1 percent, exacerbated by several surtaxes. The burden of labor taxation in France, at 47 percent for an average single worker, is among the highest in ETPS countries.

Common characteristics among poorly ranked countries often include high marginal corporate tax rates and overly complex tax rules. Four of the bottom five countries exhibit combined corporate tax rates ranging from 25 to 36.1 percent, exceeding the ETPS average. Interestingly, Ireland (27th) ranks poorly despite its low corporate tax rate, primarily due to high personal income taxes, including a top dividend rate of 51 percent, and a relatively narrow VAT base. The five lowest-ranking countries also tend to employ unusually complex corporate tax incentive structures, with between two and six alternative corporate rates, significantly higher than the ETPS average of 1.8 percent. These nations also typically feature narrow VAT bases (covering only 43-56 percent of final consumption) and higher-than-average capital gains tax rates (26-34 percent, compared to an ETPS average of 17.7 percent).

Key Policy Shifts and Their Impact

The 2025 rankings reflect various policy changes implemented by European nations, impacting their relative standing.

Croatia saw its rank improve from 17th to 15th after simplifying its personal income tax system in 2025. It eliminated municipal surtaxes, reduced the top personal income tax rate to 33 percent (from over 35 percent), introduced recurrent property taxes, and broadened its VAT base.

France experienced a decline from 30th to 31st place. This was primarily driven by the introduction of a temporary surtax on corporate income for high-revenue companies, which pushed its top marginal corporate rate to an astounding 36.1 percent for 2025 – the highest in Europe and the developed world.

Germany dropped from 24th to 26th. While it reinstated an accelerated depreciation schedule for machinery and equipment at a higher rate in mid-2025 and plans to reduce its corporate tax rate by 5 percentage points starting in 2028, these positive changes were somewhat offset by an expansion in R&D tax subsidies, which the ETPS views as distortive incentives.

Ireland moved up from 28th to 27th, a notable improvement due to its adoption of a participation exemption for dividends received from abroad, signaling a shift towards a more territorial tax system.

Portugal improved its rank from 31st to 29th. This was attributed to a reduction in its long-term capital gains tax rate from 28 to 19.6 percent, a decrease in the top corporate tax rate from 31.5 to 30.5 percent, and a more generous notional interest deduction in 2025.

Conversely, the Slovak Republic fell significantly from 10th to 14th place. This was a direct result of increasing its corporate tax rate from 21 to 24 percent, raising its VAT registration threshold, and introducing a financial transaction tax in 2025.

Deep Dive into Tax Categories

Corporate Taxation: Rates, Recovery, and Incentives

Corporate income taxes, levied on business profits, exhibit substantial variations across European countries in terms of rates and bases. The ETPS evaluates these systems based on the combined top marginal corporate income tax rate, cost recovery provisions, and the presence of tax incentives and complexities. France’s 36.1 percent corporate rate stands out as the highest, while Hungary’s 9 percent is the lowest. The average rate across ETPS countries is 21.9 percent.

Cost recovery mechanisms, such as loss offset rules (carryforwards and carrybacks) and capital allowances (depreciation for machinery, industrial buildings, and intangibles), are crucial for ensuring that businesses are taxed on true profits rather than inflated income. While many countries allow indefinite loss carryforwards, restrictions on taxable income offset or time limits are common. Estonia and Latvia, with their cash-flow corporate tax systems, implicitly allow unlimited loss carryforwards and carrybacks. Accelerated depreciation, like the UK’s permanent full expensing for machinery or Lithuania’s upcoming full expensing, improves cost recovery and boosts investment. The choice of inventory accounting methods (LIFO, average cost, FIFO) also impacts taxable income, with LIFO generally preferred for its economic neutrality. Allowances for corporate equity (ACE), adopted by Cyprus, Malta, Poland, Portugal, and Turkey, aim to reduce the debt-equity bias by allowing a deduction for a "notional" return on equity.

However, the ETPS also scrutinizes distortive tax incentives. Patent boxes, which offer lower tax rates on intellectual property income, can encourage profit shifting rather than genuine R&D. Sixteen ETPS countries currently operate such regimes. Similarly, expenditure-based R&D tax subsidies, while intended to foster innovation, can distort investment decisions and introduce complexity. Iceland, Portugal, and France offer the most generous R&D subsidies, while Bulgaria, Latvia, Luxembourg, Malta, and Switzerland provide minimal expenditure-based relief. Digital Services Taxes (DSTs), implemented by 11 ETPS countries, are also considered distortive as they target specific revenue streams of large digital businesses. Complexity, measured by multiple corporate tax rates and surtaxes, further reduces a system’s neutrality. France, Germany, and Luxembourg apply surtaxes, while Portugal leads in complexity with six different rates applying to corporate income.

Individual Income Taxation: Progressivity and Capital Treatment

Individual income taxes, often coupled with payroll taxes (social security contributions), fund general government operations. The ETPS assesses these systems based on the rate and progressivity of wage taxation, income tax complexity, and the extent of double taxation on corporate income. Denmark (55.9 percent), France (55.4 percent), and Austria (55 percent) have the highest top personal income tax rates, while Bulgaria and Romania both stand at 10 percent. The income level at which the top rate applies is also considered, with flat-tax countries like Bulgaria and Hungary applying their top rates from the first euro. The economic cost of labor taxation, measured by the ratio of marginal to average tax wedges, highlights the efficiency of the system in influencing work incentives. Hungary’s ratio of 1 indicates a perfectly flat system, while Spain, the Netherlands, and Italy have the highest ratios, suggesting greater distortions at higher income levels.

Complexity is also measured by the presence of surtaxes on personal income, such as Germany’s solidarity surcharge or Luxembourg’s solidarity tax. Croatia notably abolished its municipal surtax in 2025, decentralizing income tax rate setting. Capital gains and dividends taxes represent a second layer of taxation on corporate profits. High rates in these areas can discourage saving and investment. Denmark has the highest capital gains tax rate at 42 percent, while several countries, including Cyprus and Switzerland, do not tax long-term capital gains from listed shares. Similarly, Ireland has the highest dividend tax rate at 51 percent, contrasting sharply with Estonia and Latvia, which have 0 percent dividend tax rates due to their cash-flow corporate tax systems.

Consumption Taxes: Rates and Base Efficiency

Consumption taxes, predominantly the Value-Added Tax (VAT) in the EU, are levied on goods and services. They are considered one of the most economically efficient ways to raise revenue if broadly applied. The ETPS evaluates consumption taxes based on their rate, base, and complexity. Hungary has the highest VAT rate at 27 percent, while Switzerland has the lowest at 8.1 percent. The average rate is 21.5 percent.

The breadth of the consumption tax base is crucial. Many countries exempt or apply reduced rates to certain goods and services, narrowing the base. Exemption thresholds for businesses also vary, with countries like Spain and Turkey having no general VAT exemption threshold, receiving better scores. The VAT revenue ratio, which compares actual collected VAT revenue to potential revenue under a fully comprehensive base, highlights policy and compliance gaps. Luxembourg boasts the broadest base (82.2 percent of total consumption), while Turkey, Greece, and Italy have the narrowest (around 41-43 percent).

Property Taxes: From Real Estate to Wealth and Transactions

Property taxes, levied on individual or business assets, vary widely in their structure and economic impact. Recurrent real property taxes, particularly those solely on land value (like Estonia’s), are considered efficient. However, many countries tax both land and structures, which can deter capital formation and property improvements. Most ETPS countries apply recurrent taxes to real property, with 25 allowing deductions against corporate taxable income, mitigating double taxation.

Wealth and estate taxes, including inheritance and gift taxes, can reduce incentives to save and invest and often incur significant compliance costs for limited revenue. Norway, Spain, and Switzerland levy net wealth taxes, while Belgium, France, and Italy impose them on selected assets. Nine ETPS countries, including Austria and Estonia, have no estate, inheritance, or gift taxes. Additionally, various taxes on businesses’ assets and fixed capital, such as property transfer taxes, corporate asset taxes (often on banks), capital duties (on stock issuance), and financial transaction taxes, directly increase the cost of capital and hinder investment. Fourteen ETPS countries have financial transaction taxes, including France and the United Kingdom, while 18 do not.

Cross-Border Tax Rules: Facilitating Global Commerce

In a globalized economy, cross-border tax rules are vital for multinational businesses. The ETPS assesses these based on territoriality (dividend and capital gains exemptions), withholding taxes, tax treaty networks, and anti-tax avoidance rules.

A territorial tax system, which generally exempts foreign-earned corporate income from domestic taxation, is preferred for competitiveness. Twenty-six ETPS countries fully exempt foreign-sourced dividends, with Ireland being the latest to adopt such a participation exemption. Similarly, 25 countries fully exclude foreign-sourced capital gains. However, many countries impose restrictions on these exemptions, often based on blacklists of countries or minimum tax rate requirements, adding complexity and distorting investment decisions.

Withholding taxes on dividends, interest, and royalties paid to foreign investors or businesses increase investment costs. Estonia, Hungary, Latvia, and Malta do not levy withholding taxes on dividends or interest. The strength of a country’s tax treaty network, which reduces or eliminates withholding taxes, is also a key factor in attracting foreign investment. The United Kingdom boasts the broadest network (132 countries), while Iceland has the smallest (47).

Finally, anti-avoidance rules, such as Controlled Foreign Corporation (CFC) rules and interest deduction limitations, aim to prevent aggressive tax planning. While designed to curb profit shifting, these rules can introduce significant complexity. CFC rules, now adopted by all EU Member States following a 2016 directive, vary in scope, applying to passive or active income. Interest deduction limitations, present in all 32 ETPS countries, aim to address debt bias but can also create new distortions. General Anti-Tax Avoidance Rules (GAARs), like the UK’s diverted profits tax, further add complexity and compliance burdens, potentially leading to double taxation.

Implications for EU Policymaking

The 2025 European Tax Policy Scorecard offers invaluable insights for EU policymakers grappling with the evolving fiscal landscape. The persistent top performance of Estonia underscores the benefits of a streamlined, neutral tax system focused on cash flow, while the struggles of Italy and France highlight the pitfalls of complex, distortionary tax structures.

As the EU pursues ambitious goals like increased defense spending, green and digital transitions, and debt repayment, ensuring stable and sufficient government revenues is paramount. The scorecard strongly suggests that this revenue should be raised through competitive and neutral tax policies that foster private capital investment, rather than impeding it. Harmonization efforts within the EU must therefore prioritize these principles, moving beyond simply finding a "least common denominator" to actively designing policies that are demonstrably pro-growth. For instance, the discussion around a potential 28th corporate tax regime for the Single Market could benefit from examining models like Estonia’s distributed profits taxation, which demonstrably enhances competitiveness.

The findings indicate that countries that simplify their tax codes, reduce marginal rates, and broaden tax bases tend to perform better. Conversely, policies that introduce multiple layers of complexity, targeted incentives, or excessive taxes on capital and transactions tend to deter investment and growth. Policymakers across Europe are increasingly recognizing the need to balance fiscal needs with economic dynamism. The ETPS serves as a vital diagnostic tool, guiding nations toward reforms that can bolster their competitiveness and neutrality, ultimately contributing to a more robust and prosperous European economy.

Conclusion

The 2025 European Tax Policy Scorecard reinforces the enduring truth that a country’s tax system is a critical determinant of its economic health. As Europe navigates a period of profound geopolitical and economic transformation, the imperative for competitive and neutral tax policies has never been stronger. The scorecard provides a clear roadmap for reform, demonstrating that simplicity, low marginal rates, and broad bases are key to fostering investment, driving economic growth, and securing the fiscal future of the continent.