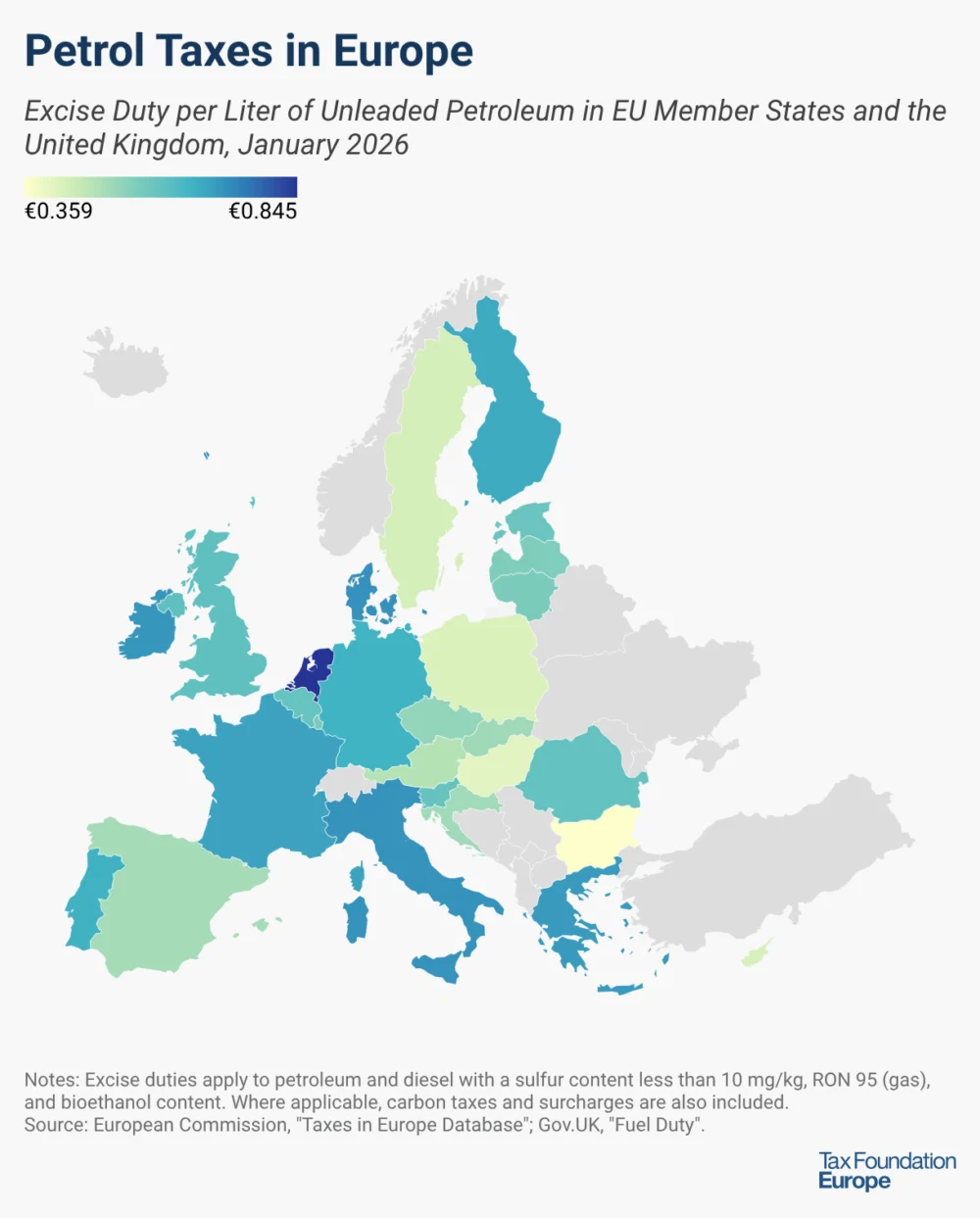

The landscape of energy taxation across the European Union and the United Kingdom sees a critical juncture on January 1, 2026, as excise duties on gas and diesel continue to play a pivotal role in national fiscal policies and broader environmental strategies. These duties, specifically applied to petroleum and diesel with a sulphur content of less than 10 mg/kg, RON 95 (unleaded petroleum), and factoring in bioethanol content, are designed not only to generate substantial government revenue but also to steer consumer behaviour towards more sustainable choices. Crucially, where applicable, these excise duties also incorporate carbon taxes and surcharges, reflecting a growing emphasis on environmental costs within fuel pricing. For the purpose of international comparison, these duties are converted into USD using the January 1, 2026, exchange rate of 1 EUR to 1.1747 USD, a standard practice for cross-jurisdictional financial analysis.

The Role and Evolution of Excise Duties

Excise duties are indirect taxes levied on the sale or consumption of specific goods, such as fuel, tobacco, and alcohol. Unlike Value Added Tax (VAT), which is a percentage of the final sale price, excise duties are typically fixed amounts per unit (e.g., per litre of fuel). Their significance extends beyond mere revenue generation; they serve as powerful policy instruments. Historically, fuel excise duties were primarily a means to fund infrastructure development and maintain road networks. However, in the 21st century, their mandate has expanded considerably to include environmental protection, public health objectives, and energy security.

The European Union has long sought to harmonise aspects of energy taxation through directives, most notably the Energy Taxation Directive (ETD), originally adopted in 2003. This directive sets minimum rates for excise duties on various energy products, including motor fuels, across all member states. The intention behind the ETD was to prevent distortions of competition within the single market and to contribute to the EU’s environmental and energy policy goals. However, the original ETD has been widely criticised for being outdated, failing to adequately reflect climate objectives, and allowing for significant disparities between member states.

Chronology of Policy Development Leading to 2026

The path to the taxation framework observed in January 2026 is marked by significant policy shifts and legislative proposals, particularly within the EU.

Early 2000s: The Energy Taxation Directive (ETD)

The ETD’s adoption in 2003 established the foundational structure for energy taxation in the EU, setting minimum rates that member states had to respect. While a step towards harmonisation, it left considerable flexibility for national governments to set higher rates, leading to wide variations.

Mid-2010s: Growing Climate Ambition

As global awareness of climate change intensified, the EU committed to ambitious decarbonisation targets. This period saw increased discussions about reforming the ETD to better align with these goals, particularly the Paris Agreement targets. Many member states began introducing national carbon taxes or surcharges on fuel to supplement existing excise duties.

July 2021: The "Fit for 55" Package

A pivotal moment came with the European Commission’s proposal for the "Fit for 55" package. This comprehensive legislative initiative aimed to reduce net greenhouse gas emissions by at least 55% by 2030, compared to 1990 levels. A key component of this package was the revision of the ETD. The proposed revisions sought to:

- Update minimum tax rates for fuels to better reflect their energy content and environmental performance.

- Introduce new tax categories for sustainable fuels and electricity to incentivise their uptake.

- Phase out outdated exemptions and reductions for fossil fuels.

- Align energy taxation with the EU Emissions Trading System (ETS) principles.

Post-Brexit United Kingdom: Divergence and Domestic Policy

Following its departure from the European Union, the United Kingdom gained full autonomy over its taxation policies, including fuel duties. While historically influenced by EU directives, the UK now sets its own rates and framework. For many years leading up to 2026, the UK government has implemented a freeze on fuel duty rates, citing cost-of-living pressures and a desire to support businesses and households. However, the UK also has its own legally binding net-zero targets by 2050, prompting ongoing debates about how fuel taxation can contribute to these goals without unduly burdening consumers. Discussions around alternative road pricing mechanisms to replace dwindling fuel duty revenues (due to EV adoption) have also gained prominence.

Leading up to January 1, 2026:

By this date, it is anticipated that legislative processes within the EU regarding the revised ETD will have progressed significantly, if not concluded, leading to a renewed framework for energy taxation. Even if final adoption of all "Fit for 55" elements is still ongoing, the direction of travel for increased environmental taxation through excise duties will be firmly established. Similarly, the UK will have had further opportunities to review its own fuel duty strategy in light of its fiscal needs, environmental commitments, and economic conditions. The January 1, 2026, snapshot thus represents a point where these evolving policy landscapes converge, presenting specific excise duty structures across the EU and UK.

Components and Technical Specifications of Fuel Excise Duties

The detailed note provided highlights several critical aspects that define the application of excise duties:

- Sulphur Content (< 10 mg/kg): This specification underscores a commitment to cleaner fuels. Low-sulphur fuels are essential for reducing harmful emissions such as sulphur dioxide (SO2), which contributes to acid rain and respiratory problems. Modern diesel and petrol engines are designed for these cleaner fuels, and their use is mandated by environmental regulations across Europe.

- RON 95 (Unleaded Petroleum): Research Octane Number (RON) 95 is a common grade of unleaded petrol widely used in most conventional passenger vehicles. Specifying this grade ensures clarity on which type of petrol the duty rates apply to, as different octane levels (e.g., RON 98) might have slightly different duty structures in some jurisdictions.

- Bioethanol Content: The inclusion of bioethanol content is a direct nod to renewable energy policies. Bioethanol is an alcohol produced from biomass and is blended with petrol to reduce reliance on fossil fuels and lower carbon emissions. Tax policies often differentiate duties based on the percentage of bioethanol or other biofuels present, frequently offering lower rates for higher biofuel blends to incentivise their use. This aligns with the EU’s Renewable Energy Directive targets.

- Carbon Taxes and Surcharges: These are increasingly integrated into fuel excise duties. A carbon tax directly places a price on carbon emissions, aiming to make carbon-intensive activities more expensive and thereby encourage a shift towards lower-carbon alternatives. Surcharges might also be applied for various reasons, such as funding specific environmental projects or contributing to national energy transition funds. Their inclusion signifies a move beyond simple volumetric taxation towards a more nuanced approach that internalises environmental externalities.

The conversion rate of 1 EUR to 1.1747 USD is crucial for comparing rates across different currencies, providing a standardised metric for international analysis. It allows policymakers, businesses, and consumers to understand the relative cost of fuel taxation in a global context.

Inferred Statements and Reactions

While specific statements for January 2026 are not available, reactions from various stakeholders can be logically inferred based on ongoing debates and policy directions:

European Commission Officials: "The updated Energy Taxation Directive, central to our ‘Fit for 55’ agenda, ensures that our taxation framework is genuinely aligned with our climate ambitions. By adjusting minimum rates and better reflecting environmental performance, we are sending a clear signal to markets and consumers: the polluter pays. This is not just about revenue; it’s about accelerating our transition to a climate-neutral economy by 2050."

National Finance Ministers (EU): "Balancing our fiscal needs with environmental targets and the cost of living remains a complex challenge. The revised ETD provides a common framework, but national flexibility is essential to address specific economic realities and social impacts. We are committed to a fair transition, ensuring that green taxes do not disproportionately burden households and businesses, particularly in our rural areas."

UK Government Spokesperson: "Our approach to fuel duty prioritises supporting families and businesses while remaining steadfast in our commitment to net zero. We continue to monitor global energy markets and the impact of fuel costs. As we transition away from fossil fuels, we are actively exploring sustainable long-term solutions for road funding, including potential alternatives to traditional fuel duties, to ensure fairness and future-proof our infrastructure."

Transport Industry Representatives: "Increases in fuel excise duties, particularly without adequate support for fleet decarbonisation, directly translate into higher operational costs for logistics and transport companies. This inevitably impacts supply chains and consumer prices. While we understand the environmental imperative, a gradual and predictable transition, coupled with investments in charging infrastructure and alternative fuel technologies, is vital to avoid undermining economic competitiveness."

Environmental NGOs: "These excise duties are a fundamental tool in the fight against climate change. The inclusion of carbon taxes and incentives for biofuels is a step in the right direction. However, to truly drive change, rates must adequately reflect the true environmental cost of fossil fuels, and governments must resist pressure to freeze or reduce duties based solely on short-term economic fluctuations. The focus must be on accelerating the shift to electric vehicles and sustainable public transport."

Broader Impact and Implications

The excise duty framework in place as of January 1, 2026, carries multifaceted implications across economic, environmental, and social dimensions.

Economic Implications:

- Consumer Costs and Inflation: Higher excise duties directly increase fuel prices at the pump, impacting household budgets, particularly for those reliant on private vehicles for commuting or lacking access to public transport. This can contribute to inflationary pressures, especially in sectors like food and goods transport.

- Business Competitiveness: For industries heavily dependent on road transport (e.g., logistics, agriculture, construction), increased fuel costs can erode profit margins and potentially reduce competitiveness. Businesses may pass these costs onto consumers, contributing to higher prices, or seek to absorb them, impacting investment.

- Government Revenue: Fuel excise duties remain a significant source of revenue for national governments, funding public services and infrastructure. However, as vehicle fleets transition towards electric and alternative fuels, this revenue stream is projected to decline, necessitating a re-evaluation of public finance models.

- Cross-Border Shopping: Significant disparities in fuel duty rates between neighbouring countries can lead to "fuel tourism," where drivers cross borders to purchase cheaper fuel, impacting local businesses and government revenues in higher-taxing regions.

Environmental Implications:

- Emission Reduction: By increasing the cost of fossil fuels, excise duties incentivise reduced consumption, more fuel-efficient driving, and the adoption of lower-emission vehicles and alternative fuels. The inclusion of carbon taxes directly targets greenhouse gas emissions.

- Promotion of Sustainable Fuels: Differentiated duties that favour biofuels or electricity actively promote their uptake, aligning with renewable energy targets and reducing the carbon intensity of the transport sector.

- Air Quality Improvement: The focus on low-sulphur fuels contributes to better urban air quality by reducing pollutants that cause respiratory illnesses and smog.

Social Implications:

- Regressive Nature: Fuel taxes are often criticised for being regressive, meaning they disproportionately affect lower-income households who spend a larger percentage of their income on essential transport, especially in areas with limited public transport options.

- Rural vs. Urban Divide: Rural communities, which often have longer commuting distances and fewer public transport alternatives, can be more heavily impacted by higher fuel duties than urban populations.

- Investment in Alternatives: The revenue generated from fuel duties, or the policy impetus they create, can be channelled into developing sustainable transport infrastructure, such as public transport networks, cycling infrastructure, and electric vehicle charging points, which can help mitigate the social impacts of higher fuel costs.

Future Outlook and Challenges

Looking beyond January 2026, the trajectory of fuel excise duties in the EU and UK faces several fundamental challenges and potential transformations. The rapid electrification of transport poses the most significant long-term threat to traditional fuel duty revenue models. As internal combustion engine vehicles are phased out, governments will need to find alternative ways to tax road use and fund infrastructure. Road pricing schemes, based on distance travelled, vehicle type, or time of day, are increasingly being explored as viable alternatives.

Furthermore, the ongoing debate within the EU regarding the final shape of the revised Energy Taxation Directive will continue to influence national policies. While the "Fit for 55" package aims for greater environmental alignment, achieving consensus among 27 member states, each with unique economic circumstances and energy mixes, remains a complex task. The UK, free from EU directives, has the flexibility to innovate its own taxation approach, potentially allowing for more dynamic responses to technological changes and consumer behaviour.

In conclusion, the excise duties on gas and diesel in the EU and UK as of January 1, 2026, are more than just taxes; they are integral components of a complex policy framework designed to balance fiscal needs, environmental imperatives, and social considerations. They represent a snapshot in an ongoing evolution towards a greener, more sustainable, and economically resilient transport sector, constantly adapting to new technologies, changing climate targets, and shifting societal expectations.