The Internal Revenue Service (IRS) has officially released Schedule 1-A for the 2025 tax year, along with its comprehensive instructions, marking a significant step in implementing tax relief measures introduced by the "One Big Beautiful Bill Act" (OBBBA) passed in July. This new schedule provides a dedicated pathway for eligible taxpayers to claim a suite of new deductions, including those for qualified tips, overtime compensation, interest paid on certain auto loans, and an enhanced deduction specifically for senior citizens. The finalized version, published on a Monday, follows a draft release of Schedule 1-A in September 2025, allowing tax professionals and the public ample time to review and prepare for its application.

The introduction of Schedule 1-A signifies a proactive effort by the IRS to operationalize key provisions of the OBBBA, aiming to provide tangible financial benefits to a broad spectrum of taxpayers. The legislation, designed to stimulate economic activity and provide targeted relief, has now been translated into actionable tax forms, empowering individuals to reduce their tax liabilities through these newly available deductions. The IRS’s timely release of the finalized schedule and instructions underscores the agency’s commitment to facilitating compliance and ensuring taxpayers can fully leverage the legislative benefits.

A Closer Look at the New Deductions

Schedule 1-A is divided into several parts, each addressing a specific category of tax benefit. These sections are designed to guide taxpayers through the eligibility requirements, calculation methods, and documentation necessary to claim their respective deductions.

Deduction for Qualified Tips

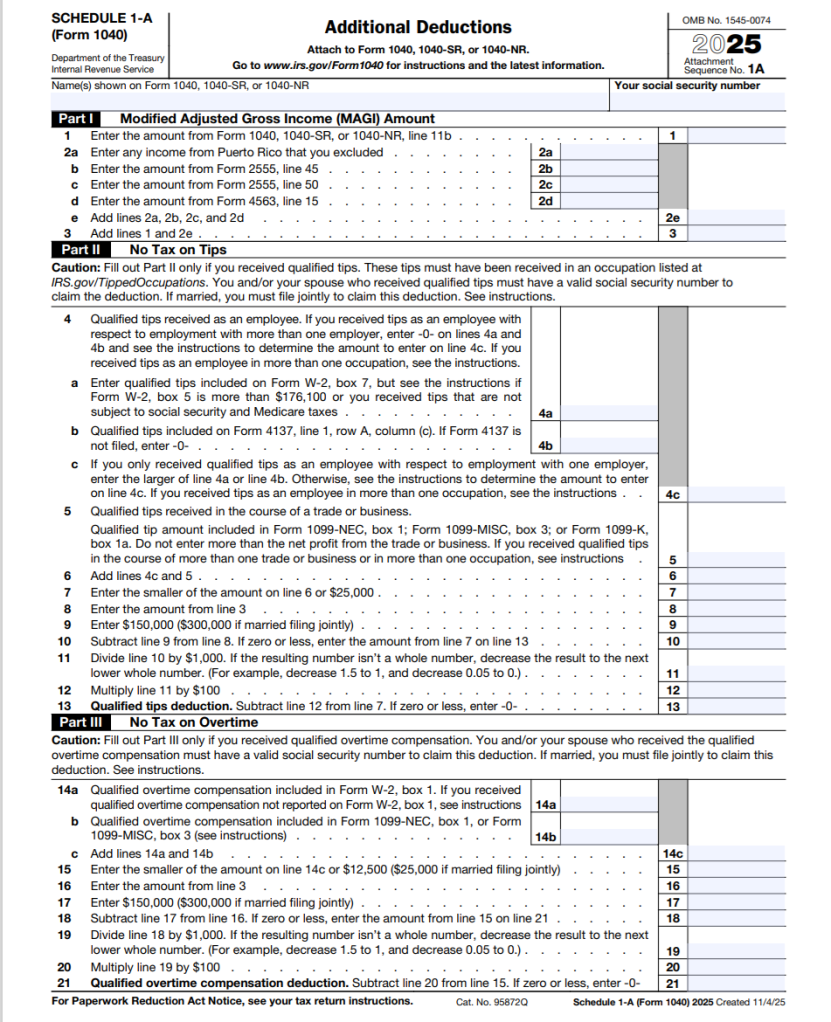

Part II of the Schedule 1-A instructions details the process for claiming a deduction on qualified tips. This provision aims to alleviate the tax burden on workers who receive a significant portion of their income through gratuities, a common practice in industries such as hospitality, food service, and personal care. Eligible taxpayers can claim a deduction of up to $25,000 for qualified tips. However, this deduction is subject to a Modified Adjusted Gross Income (MAGI) phaseout. For single filers, the deduction begins to phase out when MAGI exceeds $150,000. For those married filing jointly, this threshold is doubled to $300,000.

Crucially, to claim this deduction, tips must have been reported to employers. This emphasizes the importance of accurate record-keeping and transparent reporting by both employees and employers. The instructions provide a detailed breakdown of what constitutes "qualified tips," offering clarity on the types of gratuities that qualify for this deduction. Furthermore, the IRS has included illustrative examples and worksheets designed to assist tipped workers in calculating their eligible deduction, particularly for those who may not have a formal background in tax preparation. The guidance also lists common occupations where tipping is customary and regular, serving as a helpful reference for potential claimants.

The ability to claim the tips deduction regardless of whether a taxpayer opts for the standard deduction or itemizes their deductions offers broad accessibility. This flexibility ensures that a wide range of tipped workers, from those who benefit most from the standard deduction to those who itemize, can potentially reduce their tax obligations. This is a significant enhancement, as many tax benefits are often tied to itemization, which not all taxpayers utilize.

Deduction for Overtime Compensation

Part III of the instructions addresses a deduction for overtime compensation, a benefit designed to recognize and reward workers who contribute extra hours to their jobs. This deduction is available to certain workers who receive overtime pay as mandated by the Fair Labor Standards Act of 1938 (FLSA). The legislation defines qualified overtime compensation as any overtime pay that exceeds an employee’s regular rate of pay, specifically referring to the "half" portion of "time-and-a-half" wages. Employers may report this as "overtime premium" or "FLSA Overtime Premium" on wage statements.

Married taxpayers must file a joint return to be eligible for this deduction. The maximum deduction allowed is $12,500 per individual, with a combined limit of $25,000 for married couples filing jointly. Similar to the tips deduction, the overtime compensation deduction is subject to a MAGI phaseout. For single filers, the phaseout begins when MAGI exceeds $150,000, and for married couples filing jointly, it starts at $300,000. The instructions also clarify that this deduction can be claimed irrespective of whether the taxpayer takes the standard deduction or itemizes.

The inclusion of this deduction acknowledges the financial pressures often faced by individuals working extended hours and aims to provide some tax relief. The detailed definition of qualified overtime compensation, along with provided examples and worksheets, is intended to demystify the calculation process and encourage accurate claiming. This measure could potentially incentivize workers to undertake additional shifts, knowing that a portion of their overtime earnings may be shielded from federal income tax.

Deduction for Auto Loan Interest

Part IV of the Schedule 1-A instructions introduces a deduction for interest paid on qualified passenger vehicle loans. This provision offers a new avenue for taxpayers to reduce their tax burden, particularly for those who have financed the purchase of a vehicle. The deduction is available to taxpayers who claim the standard deduction as well as those who itemize.

The instructions provide clear definitions for key terms such as "qualified passenger vehicle loan interest," "applicable passenger vehicle," "final assembly in the United States," and "personal use." These definitions are crucial for taxpayers to determine their eligibility. The requirement for "final assembly in the United States" suggests a potential alignment with broader policy goals of promoting domestic manufacturing and economic development. This aspect of the deduction could encourage the purchase of vehicles manufactured within the U.S., thereby supporting American jobs and industries.

By allowing this deduction regardless of itemization status, the IRS ensures that a wider range of vehicle owners can benefit. This is particularly relevant given the increasing reliance on personal vehicles for commuting and daily life in many parts of the country. The economic implications could be a slight boost in consumer spending on vehicles that meet the criteria, as the after-tax cost of ownership is reduced for those who qualify.

Enhanced Deduction for Senior Citizens

Part V of the instructions outlines the enhanced deduction for senior citizens, a significant benefit designed to support older Americans. This deduction can be claimed by individuals who opt for either the standard deduction or itemization. However, married couples seeking to claim this deduction must file jointly.

To qualify for this enhanced deduction, taxpayers (and their spouses, if filing jointly) must have been born before January 2, 1961. Additionally, the taxpayer, and each spouse claiming the deduction on a joint return, must possess a valid Social Security number. The maximum enhanced deduction is set at $6,000 per person. For married couples filing jointly, where both spouses meet the age and Social Security number requirements, the total deduction can reach $12,000.

This enhanced deduction is also subject to a MAGI phaseout. For single filers, the deduction begins to decrease when MAGI exceeds $75,000. For married couples filing jointly, this threshold is $150,000. This provision acknowledges the often-fixed incomes of senior citizens and aims to provide them with additional financial relief, potentially easing the burden of rising living costs and healthcare expenses. The age criterion, tied to a specific birthdate, ensures that this benefit is targeted towards a defined demographic within the senior population.

Context and Chronology of the OBBBA and Schedule 1-A

The "One Big Beautiful Bill Act" (OBBBA) was enacted in July of the preceding year, representing a significant legislative effort to address various economic and social priorities. The bill’s passage was the culmination of extensive debate and negotiation, with proponents highlighting its potential to stimulate economic growth, provide relief to middle- and lower-income households, and incentivize certain consumer behaviors. The inclusion of specific tax deductions for tips, overtime, auto loans, and seniors was a key feature, designed to offer targeted financial assistance.

Following the OBBBA’s enactment, the IRS was tasked with developing the necessary forms and guidance to implement these new provisions. The agency began this process by releasing a draft version of Schedule 1-A in September 2025. This draft served as an important checkpoint, allowing tax professionals, software developers, and the public to review the proposed structure and content of the form and its associated instructions. Feedback gathered during this period likely informed the final revisions and clarifications incorporated into the officially published version.

The final release of Schedule 1-A and its instructions on a Monday signifies the completion of this implementation phase. Taxpayers can now rely on these finalized documents for the upcoming tax filing season, ensuring compliance and maximizing their potential tax benefits. The timeline demonstrates a coordinated effort between the legislative branch, which created the new tax provisions, and the executive branch, through the IRS, which is responsible for their administration.

Broader Impact and Implications

The introduction of Schedule 1-A and its associated deductions has several potential implications for the U.S. tax landscape and the economy. For individual taxpayers, the most direct impact will be a reduction in their overall tax liability, leading to increased disposable income. This could translate into higher consumer spending, particularly for those who benefit from the auto loan interest deduction or the enhanced senior deduction, potentially stimulating economic activity.

For workers in tipped professions, the new deduction offers a tangible recognition of their often-underreported income, encouraging more accurate reporting and potentially reducing the tax burden on a significant segment of the workforce. Similarly, the overtime deduction acknowledges the contributions of those who work beyond standard hours, providing a financial incentive for extended work.

The auto loan interest deduction, with its requirement for U.S. final assembly, introduces an element of industrial policy into the tax code, potentially influencing consumer choices and supporting domestic automotive manufacturing. This could lead to increased demand for vehicles produced in the United States.

The enhanced deduction for senior citizens is a direct response to the financial challenges faced by older Americans, many of whom live on fixed incomes. This provision aims to provide greater financial security and alleviate the impact of inflation and healthcare costs.

From a broader economic perspective, these deductions collectively represent a significant fiscal measure. The IRS will be closely monitoring the utilization of these deductions to assess their impact on tax revenue and economic indicators. Tax professionals will play a crucial role in educating their clients about these new opportunities, ensuring that eligible taxpayers can benefit from the provisions of the OBBBA. The complexity of some of the deductions, particularly the MAGI phaseouts and definitions, will necessitate careful guidance and accurate record-keeping to avoid errors or misinterpretations.

The IRS’s release of Schedule 1-A is a pivotal moment in the implementation of the One Big Beautiful Bill Act. It provides the necessary tools for taxpayers to access new tax benefits, underscoring the legislative intent to provide targeted financial relief and support various economic sectors. As the tax filing season approaches, the focus will shift to how effectively taxpayers and their advisors navigate these new provisions and realize the intended benefits.