As the global digital economy continues its rapid expansion, the proliferation of specialized online marketplaces has transformed from a niche trend into a dominant retail force. For entrepreneurs and enterprises transitioning from traditional single-seller models to multi-vendor platforms, the administrative complexities of sales tax compliance have emerged as a primary operational hurdle. Navigating the labyrinth of state-level regulations, marketplace facilitator laws, and the technical requirements of real-time tax calculation is no longer an optional secondary task but a foundational requirement for fiscal viability and legal standing in 2026.

An online marketplace, in its contemporary iteration, serves as a centralized digital hub where diverse third-party vendors list and transact goods or services. While giants such as Amazon, eBay, and Etsy have historically defined this space, the current market is characterized by a surge in "curated marketplaces"—platforms like 1stDibs for luxury furniture or Ruby Lane for vintage collectibles—that cater to specific consumer demographics. This shift toward decentralized commerce has forced a significant evolution in how tax authorities view the flow of capital, shifting the burden of tax collection from individual micro-sellers to the platform operators themselves.

The Historical Context: From Physical Nexus to Marketplace Facilitator Laws

The current state of sales tax for online marketplaces is the result of a decade of intense legal and legislative maneuvering. To understand the obligations of a marketplace provider in 2026, one must look back at the pivotal shifts in American tax law that eliminated the "physical presence" requirement for tax collection.

The chronology of this evolution began in earnest with the 1992 Supreme Court case Quill Corp. v. North Dakota, which ruled that states could only require businesses with a physical presence (such as a warehouse or office) to collect sales tax. However, the explosion of e-commerce rendered this standard obsolete. The turning point arrived in 2018 with South Dakota v. Wayfair, Inc., where the Supreme Court overturned Quill, allowing states to mandate tax collection based on "economic nexus"—a threshold of sales volume or transaction count within a state.

Following Wayfair, states rapidly enacted Marketplace Facilitator Laws. By 2024, nearly every U.S. state with a general sales tax had implemented statutes requiring marketplace providers to calculate, collect, and remit sales tax on behalf of their third-party sellers. This legislative wave effectively centralized the tax burden, making the platform operator the primary point of contact for state departments of revenue.

Strategic Compliance Models: Choosing an Operational Path

For modern marketplace operators, the decision on how to manage sales tax generally falls into two distinct strategic categories, each with its own set of risks and administrative requirements.

The "Seller of Record" Model

In the Seller of Record (SOR) framework, the marketplace platform assumes full legal responsibility for every transaction occurring on its site. From the perspective of the tax authorities, the marketplace is the entity selling the product, regardless of which third-party vendor fulfilled the order.

The primary advantage of this model is the enhanced user experience for vendors. Small-scale sellers are often drawn to SOR platforms because they are relieved of the daunting task of registering for tax permits in dozens of jurisdictions. However, for the marketplace operator, the SOR model represents a massive administrative undertaking. The platform must manage nexus in every state where its aggregate sales meet economic thresholds, register for permits, track varying taxability rules for different product categories, and manage complex filing schedules.

The Facilitator and Support Model

Alternatively, many platforms choose to act as facilitators, providing the technical infrastructure for sellers to manage their own tax obligations. Under this model, the marketplace provides integrated tools—often powered by sophisticated APIs—that allow sellers to set their own tax parameters based on where they have established nexus.

While this reduces the direct liability of the marketplace in some jurisdictions, it requires a robust technical integration to ensure that the tax calculated at checkout is accurate. In states with strict facilitator laws, the marketplace may still be required to collect and remit the tax, but the "Facilitator and Support" model allows for a more granular distribution of data and reporting responsibilities between the platform and the vendor.

Supporting Data: The Complexity of the Current Tax Environment

The necessity for automated tax solutions is underscored by the sheer volume of data involved in modern compliance. As of 2026, there are more than 11,000 different sales tax jurisdictions in the United States alone. These jurisdictions include not only state-level taxes but also county, city, and special district taxes, each with its own specific rate and set of exemptions.

Data from recent fiscal years indicates that:

- Compliance Costs: Small to mid-sized marketplaces spend an average of $60,000 to $100,000 annually on manual tax compliance efforts if they do not utilize automation.

- Audit Risks: States have increased their audit departments by an average of 15% since 2023, specifically targeting e-commerce platforms to close the "tax gap" left by unregistered remote sellers.

- Revenue Impact: Marketplace facilitator laws now account for over 70% of all remote sales tax revenue collected by states, highlighting the central role platforms play in public finance.

Furthermore, the taxability of items remains highly inconsistent. For example, a digital software subscription may be exempt in one state, taxed at a reduced rate in another, and fully taxable in a third. For a marketplace hosting thousands of diverse products, managing these "taxability rules" manually is statistically impossible without incurring significant error rates.

Industry Responses and Technical Integration

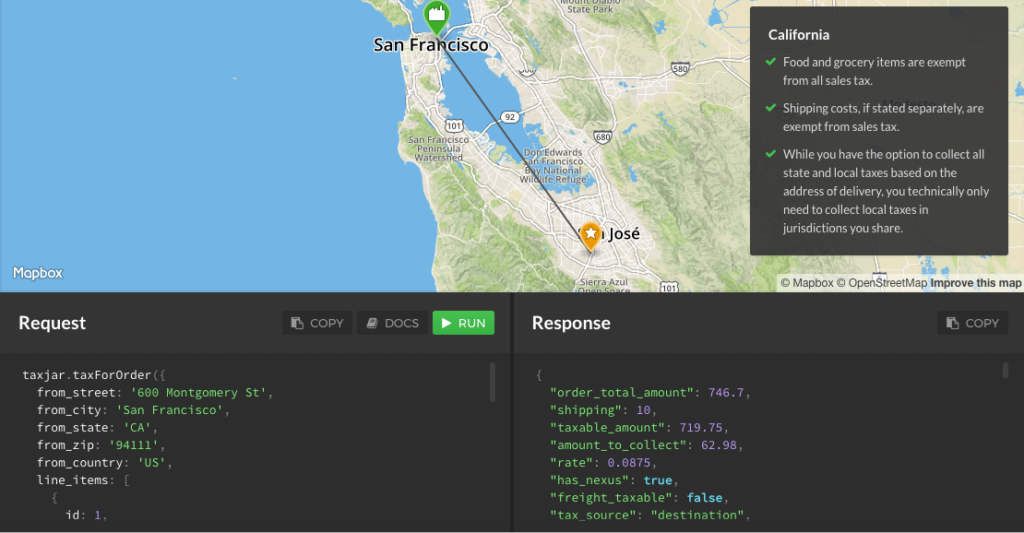

The tech industry has responded to these challenges by developing "Tax-as-a-Service" (TaaS) solutions. Platforms like TaxJar have pioneered the use of high-speed APIs that integrate directly into the marketplace’s checkout flow. When a customer enters their shipping address, the API calculates the precise tax due in milliseconds, factoring in the current jurisdictional rates and the specific taxability of the product category.

Industry experts emphasize that the "developer-first" approach is critical for 2026. "The goal for a marketplace founder should be to treat sales tax as a solved technical problem rather than a recurring accounting nightmare," says Sarah Jenkins, a senior consultant at a leading fintech advisory firm. "By leveraging APIs, marketplaces can scale from ten sellers to ten thousand without needing to exponentially grow their back-office tax department."

Moreover, the integration of automated reporting and filing (AutoFile) has become a standard requirement. These systems not only collect the tax but also aggregate the data into "return-ready" formats, ensuring that the marketplace or the individual seller can file accurate documents with state authorities on time, every time.

Broader Implications and Future Outlook

The implications of these tax structures extend beyond mere accounting. They are actively shaping the competitive landscape of the e-commerce industry. The high barrier to entry created by tax compliance requirements has led to a "flight to quality," where sellers prefer platforms that offer the most robust compliance support. Marketplaces that fail to provide seamless tax integration often see higher vendor churn and increased exposure to legal liability.

Looking forward, the trend toward "Real-Time Reporting" is expected to accelerate. Several states are currently exploring pilot programs that would require businesses to remit sales tax at the moment of transaction rather than at the end of a monthly or quarterly filing period. For marketplace operators, this will necessitate even tighter integration between payment processors and tax automation engines.

Furthermore, the international landscape is mirroring the U.S. model. The European Union’s VAT rules for marketplaces and similar "deemed supplier" regulations in the UK and Australia suggest a global consensus: the platform is the most efficient point of tax collection.

In conclusion, for online marketplace providers in 2026, sales tax is no longer a peripheral concern. It is a core component of the platform’s value proposition. Whether an operator chooses to be the Seller of Record or a facilitating partner, the use of automated, API-driven solutions is the only viable path to maintaining compliance in an increasingly scrutinized and complex global market. By prioritizing tax infrastructure early in the development lifecycle, marketplace owners can mitigate risk, attract high-quality vendors, and focus on the primary goal of scaling their digital ecosystem.