Individual income taxes continue to serve as a foundational pillar of state government finance across the United States, constituting approximately 33 percent of all state tax collections in fiscal year 2024, the most recent period for which comprehensive data are available. This significant revenue stream is unique in its direct engagement with citizens, as individuals are actively responsible for filing these taxes, a contrast to the often indirect nature of sales and excise tax payments. As of early 2026, the landscape of state individual income taxation is characterized by a dynamic interplay of rate adjustments, structural reforms, and evolving conformity with federal tax policies, reflecting a broader trend of fiscal reevaluation among states.

The Evolving Landscape of State Income Taxation

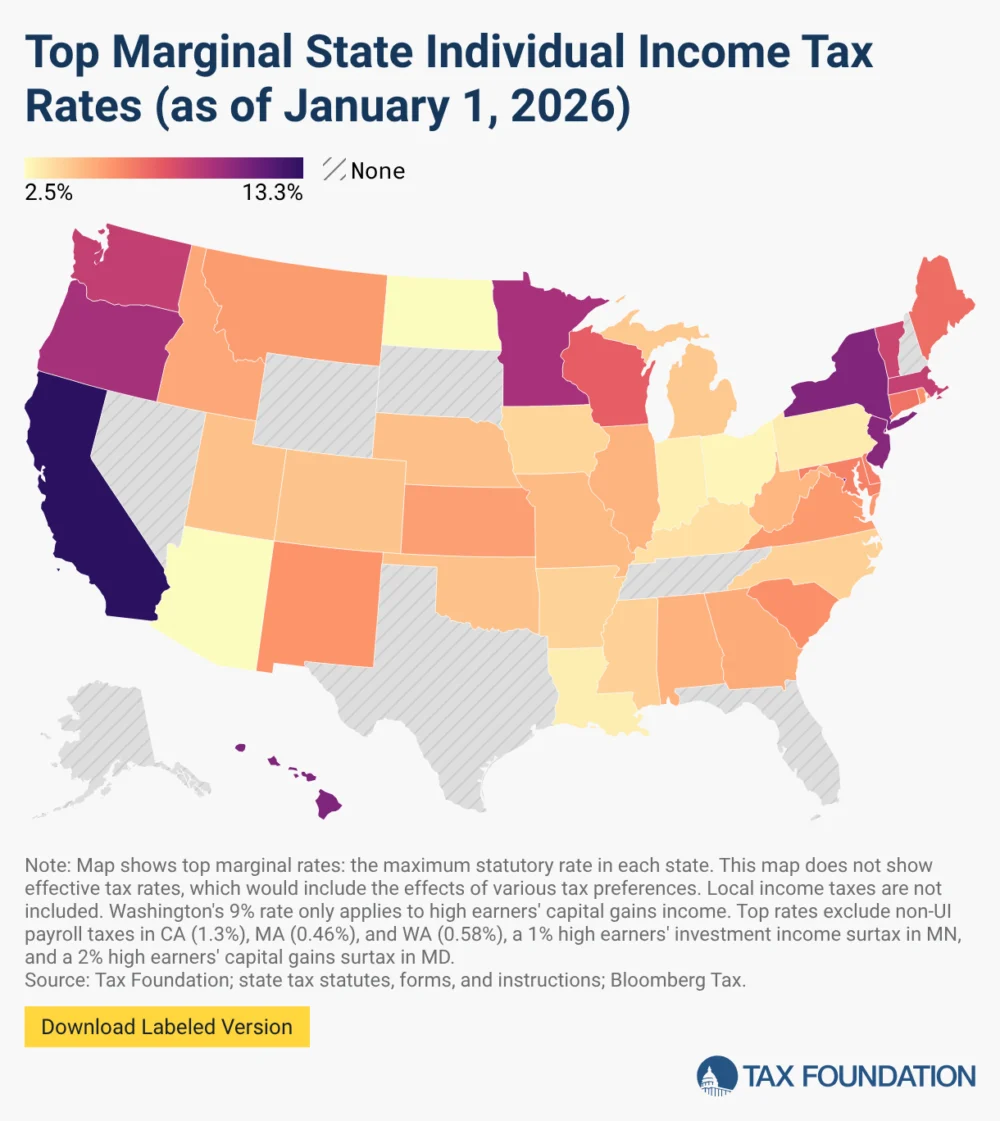

Forty-two states currently impose an individual income tax, with 41 of these specifically taxing wage and salary income. The remaining states either opt for no individual income tax whatsoever (eight states, including New Hampshire, which fully repealed its interest and dividends tax effective 2025) or apply it selectively. For instance, Washington state exclusively levies a tax on capital gains income for high earners, while Missouri explicitly exempts capital gains income from its state income tax, illustrating the diverse philosophical and practical approaches states adopt in their revenue strategies. This variation underscores a complex policy environment where states seek to balance revenue generation with economic competitiveness and perceived taxpayer fairness.

The structural diversity of state income tax systems is equally pronounced. Fifteen states have embraced single-rate tax structures, applying a uniform rate to all taxable income, simplifying compliance for many taxpayers and often championed for its perceived fairness and efficiency. Conversely, 26 states and the District of Columbia operate with graduated-rate income taxes, featuring multiple tax brackets where rates typically increase with income. The complexity of these graduated systems varies widely, from states like Arkansas, Kansas, Massachusetts, Montana, and North Dakota, which employ a streamlined two-bracket system, to Hawaii, which stands out with a robust 12-bracket structure. These differing approaches reflect diverse policy objectives, ranging from simplifying tax administration to implementing more progressive taxation designed to place a higher burden on wealthier individuals.

Top marginal income tax rates across the nation in 2026 span a considerable range, from a low of 2.5 percent in Arizona and North Dakota to a high of 13.3 percent in California. California’s effective top rate is even higher, reaching 14.4 percent when a 1.1 percent payroll tax on wage income, with no wage ceiling as of 2024, is factored in. This wide disparity in top rates highlights the competitive environment among states, where tax policy can significantly influence decisions related to residency, business location, and investment.

Beyond the number of brackets, states also differ in how these brackets are structured. Some states, like Virginia, feature a rapid progression through their brackets, with taxpayers reaching the highest marginal rate at a relatively modest income level (e.g., $17,000 in taxable income). In contrast, other states, including California (when considering its "millionaire’s tax" surcharge), Maryland, Massachusetts, New Jersey, New York, and the District of Columbia, reserve their top marginal rates for individuals earning $1 million or more in marginal income. These high-income thresholds reflect a policy choice to target substantial wealth, often with the goal of funding specific social programs or public services.

Key Tax Policy Design Elements and Federal Interplay

The intricacies of state income tax systems extend to other critical design elements. To mitigate the so-called "marriage penalty"—where a couple’s combined tax bill increases upon marriage due to bracket configurations—some states effectively double their single-filer bracket widths for married filers. Furthermore, the practice of indexing tax brackets, exemptions, and deductions for inflation varies significantly. While some states proactively adjust these parameters annually to prevent "bracket creep" (where inflation pushes taxpayers into higher brackets despite no real increase in purchasing power), many others do not, leading to a hidden tax increase over time.

A crucial aspect of state income tax administration is their conformity with the federal tax code. Most states utilize the federal tax code as a foundational starting point for their own income tax calculations. However, the degree and method of conformity differ. The federal Tax Cuts and Jobs Act of 2017 (TCJA) significantly altered the federal landscape by increasing the standard deduction and temporarily suspending the personal exemption, reducing it to $0 through 2025. This federal shift prompted many states to re-evaluate their own deductions and exemptions.

The subsequent enactment of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, further reshaped the federal framework. The OBBBA permanently extended the TCJA’s higher standard deduction, retroactively increasing it to $15,750 for single filers and $31,500 for joint filers for tax year 2025, and subsequently adjusted for inflation to $16,100 and $32,200, respectively, for tax year 2026. Critically, the OBBBA also permanently suspended the federal personal exemption.

This rapid succession of federal legislative changes has presented significant challenges for states, particularly those employing static conformity to the Internal Revenue Code (IRC). Many states’ 2025 legislative sessions concluded before the OBBBA was enacted, meaning their current statutes may conform to an outdated version of the IRC. Consequently, some states that generally conform to the federal standard deduction but haven’t updated their conformity dates to a post-OBBBA version of the IRC inadvertently revert to the pre-TCJA federal standard deduction amounts, which, adjusted for inflation, are $8,350 for single filers and $16,700 for joint filers for tax year 2026. This creates a risk of an unintended and unlegislated tax increase for residents in these states. Tax policy analysts anticipate that many of these states will prioritize legislation in their upcoming sessions to update their conformity dates and retroactively incorporate the higher OBBBA-mandated standard deduction amounts, ensuring consistency with federal intent and preventing unexpected tax burdens on their citizens.

Chronology of Notable 2026 State Individual Income Tax Changes

The year 2026 marks another significant period of evolution in state individual income tax policy, building on a robust trend of tax rate reductions observed since 2021. Over this period, 26 states have reduced their individual income tax rates, with 23 specifically lowering their top marginal rates. A notable shift has also seen seven states transition from graduated-rate to single-rate income tax structures. While the dominant trend has been towards lower taxes, a few jurisdictions, including Maryland, Massachusetts, New York, Washington, and the District of Columbia, have implemented increases to their top marginal rates. Michigan, which saw a temporary reduction to 4.05 percent in 2023, reverted to its 4.25 percent rate for 2024 and subsequent years.

The following are key individual income tax changes either taking effect on January 1, 2026, or retroactively applied for 2025 with ongoing implications:

-

Georgia: Following the momentum of tax cut triggers from H.B. 1015 (2024), H.B. 111 (enacted April 2025) accelerated these reductions. The state income tax rate decreased from 5.39 percent to 5.19 percent, retroactively effective to January 1, 2025. This legislative action signals Georgia’s commitment to a more competitive tax environment, with state statutes still allowing for further accelerated rate reductions if specific revenue conditions are met. Such measures are often cited by policymakers as crucial for fostering economic growth and attracting investment.

-

Idaho: House Bill 40, enacted in March 2025, retroactively lowered Idaho’s individual income tax rate from 5.695 percent to 5.3 percent. This reduction continues Idaho’s recent history of tax cuts aimed