The vaping industry has grown rapidly in recent decades, transforming from a niche market into a well-established product sector that provides a less harmful alternative to cigarettes for those wishing to consume nicotine or to quit smoking. This evolution has presented a complex challenge for policymakers, particularly concerning taxation, where a patchwork of state-level approaches reflects an ongoing debate over public health objectives, revenue generation, and the principle of harm reduction. As of January 2026, 34 states and the District of Columbia levy an excise tax on vaping products, yet the diversity in rates and structures creates a highly uneven and often contradictory regulatory environment across the United States.

The Evolving Vaping Market and Regulatory Scrutiny

The market for vapor products, also known as electronic nicotine delivery systems (ENDS), is diverse. Open system devices offer users flexibility, allowing them to refill tanks with various e-liquids, customize flavors, and control nicotine strength. This customization has historically appealed to experienced vapers. Conversely, closed system products, characterized by pre-filled, disposable cartridges or pods, prioritize convenience and ease of use. Their simplicity has driven their increasing popularity among consumers, but a significant portion of these products sold in the US have not received authorization for sale by the Food and Drug Administration (FDA). This regulatory divide creates a tension between consumer demand, industry innovation, and public health oversight.

The FDA’s journey to regulate vaping products began formally with its "deeming rule" in 2016, which brought e-cigarettes and other ENDS under the agency’s authority. This rule mandated that all vaping products introduced to the market after February 15, 2007, would need to undergo a rigorous Premarket Tobacco Product Application (PMTA) process to remain on sale. The PMTA requires manufacturers to demonstrate that their products are "appropriate for the protection of public health," a high bar that includes assessing the product’s risks and benefits to the population as a whole, considering both users and non-users, and accounting for the likelihood of youth initiation. The slow pace of PMTA authorizations has meant that many popular closed-system products, especially flavored ones, remain in a legal gray area, often sold without explicit FDA approval, further complicating the taxation and enforcement landscape.

A Chronology of Vaping Taxation in the U.S.

The emergence of vaping products in the early 2000s initially flew under the radar of most state tax authorities. As the market grew and public health concerns, particularly regarding youth use, began to mount, states started to consider taxation.

- 2010s: Early Adopters and Diverse Approaches: The first states to implement excise taxes on vaping products began doing so in the mid-2010s. Minnesota was an early mover, imposing a substantial 95 percent wholesale tax in 2014, a rate that predated much of the harm reduction debate and was largely aligned with existing tobacco taxes. Other states followed, but without a federal blueprint, each jurisdiction developed its own approach. Some chose ad valorem taxes based on wholesale or retail price, while others opted for volume-based taxes (per milliliter of e-liquid) or even per-cartridge taxes. This early divergence laid the foundation for the complex system observed today.

- Late 2010s: Acceleration of Taxation: As concerns about youth vaping reached a crescendo, particularly with the rise of pod-based systems, more states enacted taxes. By 2019-2020, the number of states taxing vaping products had significantly increased, often driven by dual objectives: discouraging youth use and generating revenue. Flavor bans also became a contentious issue during this period, often enacted alongside or independently of new taxes, further shaping the market.

- Early 2020s to Present: Refinement and Expansion: The trend of states implementing vaping taxes continued, albeit with ongoing debates about the optimal structure and rate. The number of states with excise taxes on vaping products grew steadily, reaching 34 states and the District of Columbia by January 2026. The challenges of comparing these disparate systems became more apparent, prompting analyses like the one discussed here to attempt to standardize the tax burden. The FDA’s PMTA process continued to unfold, creating an environment where many products remained available but unauthorized, presenting a challenge for tax collection on both legal and potentially illicit sales.

The Kaleidoscope of State Tax Structures

The variety in state taxes on vaping products is significant, reflecting differing legislative priorities and administrative capabilities. Some states levy an ad valorem tax on the manufacturer, wholesale, or retail price. This structure means the tax amount fluctuates with the product’s price, often benefiting from price increases but also susceptible to market fluctuations. Other states tax based on the product volume (e.g., per milliliter of e-liquid) or the number of cartridges. Volume-based taxes offer more predictability in revenue collection but can disproportionately impact lower-cost, higher-volume products. A few states even apply a bifurcated system, with different structures and rates for open and closed systems, attempting to account for differences in product type, use patterns, or perceived risk.

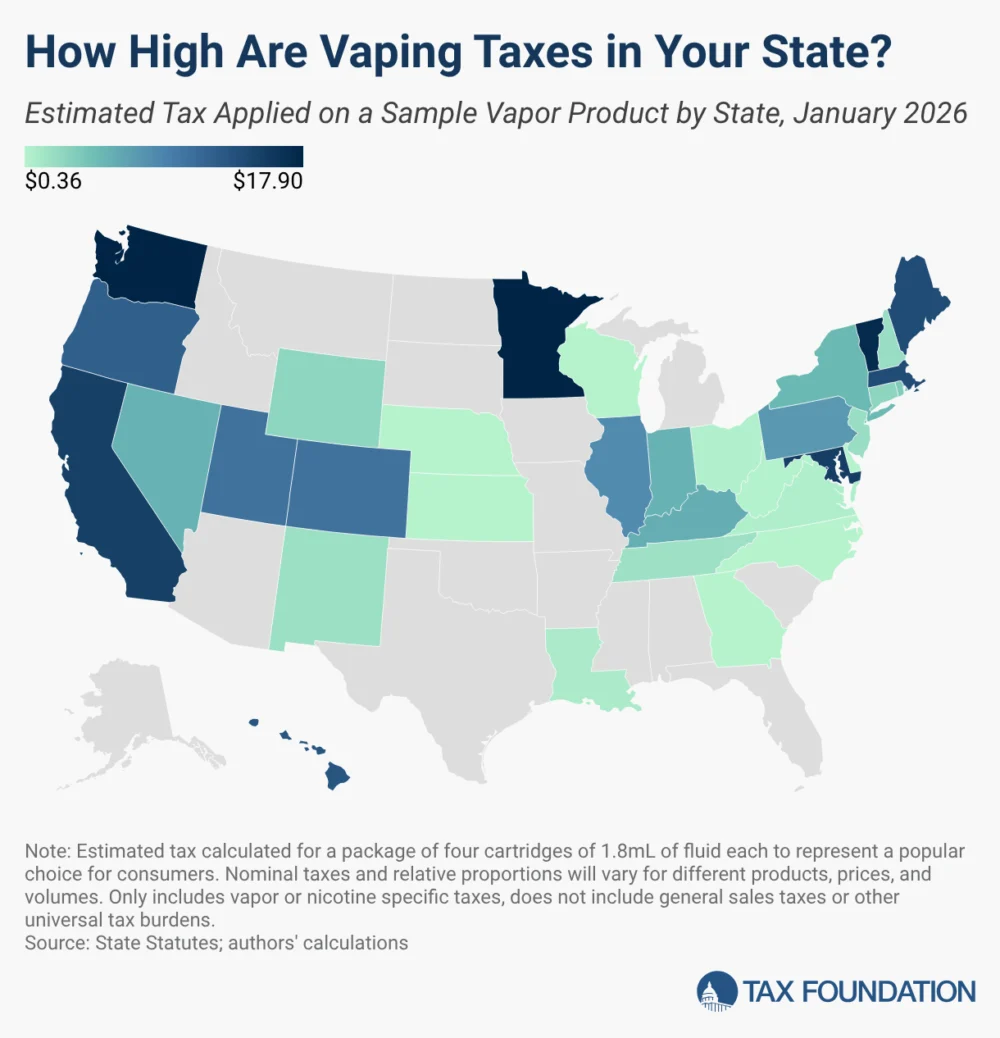

This vast array of tax structures makes a direct comparison of the overall tax burden between states exceedingly difficult. For instance, a 50 percent wholesale tax in one state might translate to a different consumer price impact than a $0.25 per mL tax in another, depending on product pricing, markups, and e-liquid volume. To provide a standardized comparison, a common analytical approach involves calculating the tax each state would charge on a specific, popular vaping product. For illustrative purposes, considering a package of four 1.8mL vaping cartridges with a wholesale price of $18.84, assuming a 5 percent wholesale price markup and a 30 percent retail price markup for determining taxes charged at different points in the production and distribution process, reveals the stark disparities.

Measuring the Burden: Highest and Lowest Taxes

Based on such standardized calculations, the burden of vaping taxes varies dramatically across the nation. Minnesota and Washington impose the heaviest wholesale tax, both at 95 percent, creating a substantial financial barrier. Vermont follows closely with a 92 percent wholesale tax. On the opposite end of the spectrum for wholesale taxes on open systems, Georgia levies a comparatively low 7 percent, and New Hampshire an 8 percent tax. Retail taxes can reach as high as 60 percent in Maryland, while California, despite its 54.27 percent wholesale tax, adds a 12.5 percent retail tax, illustrating how layered taxation can become.

For volume-based taxes, Rhode Island leads at $0.50 per mL, followed by Connecticut at $0.40 per mL. New Hampshire and New Jersey both impose $0.30 per mL on closed systems. States like Kentucky and New Mexico opt for a per-cartridge tax, at $1.50 and $0.50 per cartridge respectively.

When assessing the overall tax burden using the standardized product example, Minnesota and Washington emerge with the greatest burden at $17.90 (equivalent to approximately $2.49 per mL) due to their high wholesale taxes. In stark contrast, Delaware, Georgia, Kansas, Nebraska, North Carolina, and Wisconsin tie for the lowest overall tax levied at $0.36 (corresponding to a $0.05 per mL tax). It is crucial to note that these relative burdens would shift with different products, as ad valorem taxes react to varying prices, and industry markups can fluctuate between states and product types. This highlights the inherent complexity and the potential for unintended consequences when applying diverse tax structures across a dynamic market.

Vaping and Public Health: The Imperative of Harm Reduction

The debate over vaping taxation is inextricably linked to its public health implications, particularly the concept of harm reduction. Vaping products facilitate the delivery of nicotine, the addictive component of cigarettes and tobacco products, without the combustion and inhalation of tar and thousands of other toxic chemicals inherent to traditional cigarettes. While ongoing research into the long-term effects of vaping is still needed, the present scientific consensus is that vapor products are significantly less harmful than traditional combustible cigarettes.

Authoritative bodies have consistently affirmed this differential in harm. The English Ministry for Health, through Public Health England (now UK Health Security Agency), famously concluded in 2015 that vaping is around 95 percent less harmful than cigarettes. This finding was later corroborated by independent research, with King’s College London confirming a substantial reduction in exposure to toxicants from vaping rather than smoking in one of the largest reviews of its kind.

This significant disparity in health effects underscores the critical importance of integrating harm reduction principles into the design of excise taxes on vapor products. While not entirely harmless, vaping serves as a much less harmful alternative for adult smokers struggling to quit nicotine. Harm reduction refers to the pragmatic public health approach that prioritizes reducing the negative consequences associated with using certain products rather than attempting to eliminate that harm entirely through potentially counterproductive policies like ineffective bans or excessively punitive levels of taxation. From a public health perspective, the goal should be to encourage smokers to transition to less harmful alternatives, and tax policy plays a crucial role in shaping consumer behavior.

Economic Implications and Behavioral Responses

Nicotine-containing products, including combustible cigarettes and vapor products, are economic substitutes. This means that changes in the price or availability of one can influence the consumption of the other. Lower tax rates on vaping products, relative to cigarettes, are designed to encourage consumers to switch from more harmful combustibles. Conversely, high excise taxes on less harmful alternatives risk harming public health by making vaping less accessible or affordable, potentially pressuring vapers back to smoking or deterring smokers from attempting to switch.

Empirical evidence supports this concern. A study on Minnesota’s implementation of a 95 percent tax on vapor products found that it deterred approximately 32,400 smokers in the state from quitting cigarettes. This demonstrates a direct, adverse public health outcome stemming from a punitive tax policy. Such findings highlight the tension between the desire to tax nicotine products generally and the specific public health goal of reducing smoking-related illness and death. If the primary goal of taxing cigarettes is to encourage cessation, then vapor taxation must be considered as an integral part of that broader policy design, differentiating based on relative harm.

The Rise of Illicit Markets and Revenue Loss

The current regulatory regime, particularly the FDA’s slow authorization process and some individual states’ bans on certain vapor devices (especially flavored products), has inadvertently created conditions ripe for illicit markets. When authorized, regulated, and taxed products are unavailable or excessively expensive, consumers are often pushed towards unregulated, untaxed, and potentially more dangerous illicit vapes.

This not only undermines public health efforts by exposing consumers to products of unknown quality and safety but also precludes significant revenue collection for states. The illicit market operates outside the tax system, meaning states lose out on potential excise tax revenue that could otherwise fund public health programs, education, or other government services. Policy reform in this area represents a prime opportunity to bolster public health by reducing lives lost to smoking, generate more tax revenue through a well-regulated market, and enable growth in a market that consumers clearly support.

Stakeholder Perspectives and the Path Forward

The complexity of vaping taxation elicits diverse perspectives from various stakeholders:

- Public Health Organizations (e.g., CDC, American Lung Association): Often advocate for higher taxes on all nicotine products, including vaping, to discourage youth initiation and reduce overall nicotine use. While acknowledging harm reduction, they may prioritize a precautionary principle, especially concerning youth. They might push for taxes that align vaping with traditional tobacco products or for flavor bans.

- Vaping Industry and Consumer Advocates: Emphasize the harm reduction potential of vaping, advocating for significantly lower taxes on vapor products compared to combustible cigarettes to encourage switching. They often criticize stringent regulations and high taxes as counterproductive, arguing they drive consumers back to smoking or into black markets. They also call for a more streamlined and transparent FDA authorization process.

- State Tax Authorities: Primarily focused on stable revenue generation and administrative feasibility. They face the challenge of implementing and enforcing complex tax structures on a rapidly evolving product category, often grappling with issues of compliance and illicit trade.

- FDA: Focused on public health protection, particularly preventing youth initiation, and ensuring that products marketed are "appropriate for the protection of public health" through the PMTA process. Their stance on taxation is generally indirect, but their regulatory decisions profoundly impact market dynamics and, consequently, tax bases.

Ideal tax design for vapor products and other alternative nicotine products should account for the relative harms of each alternative. This often means a tiered tax system where products posing the greatest harm (combustible cigarettes) are taxed most heavily, and less harmful alternatives (like vapor products) are taxed at significantly lower rates. Such a system would align economic incentives with public health goals, encouraging smokers to transition away from the deadliest form of nicotine consumption.

Furthermore, a more coherent federal framework or at least greater state coordination on taxation could reduce administrative burdens and diminish the incentives for cross-border illicit trade. Policy discussions must move beyond a simple "tax all nicotine" approach to embrace a nuanced understanding of product differences and their implications for public health.

In conclusion, the current landscape of vaping taxation in the United States is a convoluted tapestry of disparate state policies, driven by a mix of revenue needs, public health concerns, and varying interpretations of harm reduction. As the scientific understanding of vaping evolves, and as the market continues to innovate, it is imperative for policymakers to develop a rational, evidence-based approach to taxation that prioritizes public health by encouraging smokers to switch to less harmful alternatives, while also ensuring robust revenue collection and mitigating the growth of dangerous illicit markets. The opportunity to save lives, generate revenue, and support consumer choice hinges on a thoughtful and integrated policy reform.