The One Big Beautiful Bill Act (OBBBA), formally enacted in July 2025, represents the most substantial legislative overhaul of federal tax policy since the landmark Tax Cuts and Jobs Act (TCJA) of 2017. This sweeping legislation has been the subject of intensive analysis, with recent updates to economic modeling by the Tax Foundation in February 2026 further refining projections. These revisions, incorporating updated economic estimates and detailed guidance on the senior deduction phaseout, have collectively increased the average national tax cut by $60.61 for 2026. Concurrently, state-level full-time equivalent (FTE) jobs numbers in the accompanying analyses have been adjusted to align with the latest economic forecasts, providing a more precise picture of the law’s anticipated effects.

The Genesis of OBBBA: Addressing the TCJA’s Sunset Provisions

The journey to the OBBBA began years before its signing, rooted in the temporary nature of many provisions within the 2017 TCJA. While the TCJA significantly reshaped the U.S. tax landscape, many of its individual tax cuts were set to expire at the end of 2025, creating a looming "tax cliff" for millions of Americans. This impending expiration prompted widespread debate in Washington regarding the future of federal taxation. Lawmakers, economists, and advocacy groups engaged in extensive discussions about whether to extend, modify, or allow these provisions to sunset.

Against a backdrop of fluctuating economic indicators and heightened fiscal policy discussions, the OBBBA emerged as a legislative priority for the ruling party and its allies. Proponents argued that allowing the TCJA’s individual provisions to expire would lead to a significant tax increase for a majority of American households, potentially stifling economic growth and consumer spending. They emphasized the need for stability and predictability in the tax code, particularly for families and small businesses. The legislative process involved months of negotiations, committee hearings, and public discourse. While the specific details of its passage remain a matter of public record, the bill successfully navigated through Congress, culminating in its presidential assent in July 2025, cementing its place as a pivotal piece of tax reform. Its primary objective was to avert the scheduled tax hikes and introduce additional measures designed to stimulate the economy, support families, and incentivize business investment.

Core Provisions: Permanence, Deductions, and Business Incentives

A cornerstone of the OBBBA is the permanent extension of the individual tax changes initially established by the TCJA. This crucial aspect avoids a projected tax increase for an estimated 62 percent of tax filers in 2026, offering long-term certainty for millions of households. Beyond merely extending existing provisions, the OBBBA introduces a suite of new tax cuts aimed at individuals and businesses.

For individual taxpayers, the act ushers in new deductions for tipped and overtime income, acknowledging the unique economic circumstances of workers in service industries and those who work beyond standard hours. These deductions are designed to provide tangible relief, particularly for middle- and lower-income earners who often rely on these forms of income. Furthermore, the OBBBA expands the Child Tax Credit (CTC) and the standard deduction, two provisions widely recognized for their role in reducing tax burdens for families and simplifying tax filing for many. The expanded CTC aims to provide more financial support for raising children, while an increased standard deduction means a larger portion of income is shielded from taxation for those who do not itemize.

On the business front, the OBBBA enshrines the permanence of 100 percent bonus depreciation and domestic research and development (R&D) expensing. Bonus depreciation, which allows businesses to immediately deduct the full cost of eligible capital investments, is a powerful incentive for companies to upgrade equipment, expand operations, and invest in productivity-enhancing assets. By making this provision permanent, the OBBBA seeks to encourage sustained capital formation and foster a more dynamic business environment. Similarly, permanent domestic R&D expensing enables businesses to deduct their research and development costs in the year they are incurred, rather than amortizing them over several years. This measure is critical for fostering innovation, encouraging technological advancements, and enhancing the competitiveness of U.S. industries on a global scale. These business-focused provisions are expected to translate into increased investment, job creation, and overall economic growth.

Unveiling Geographic Disparities in Tax Benefits

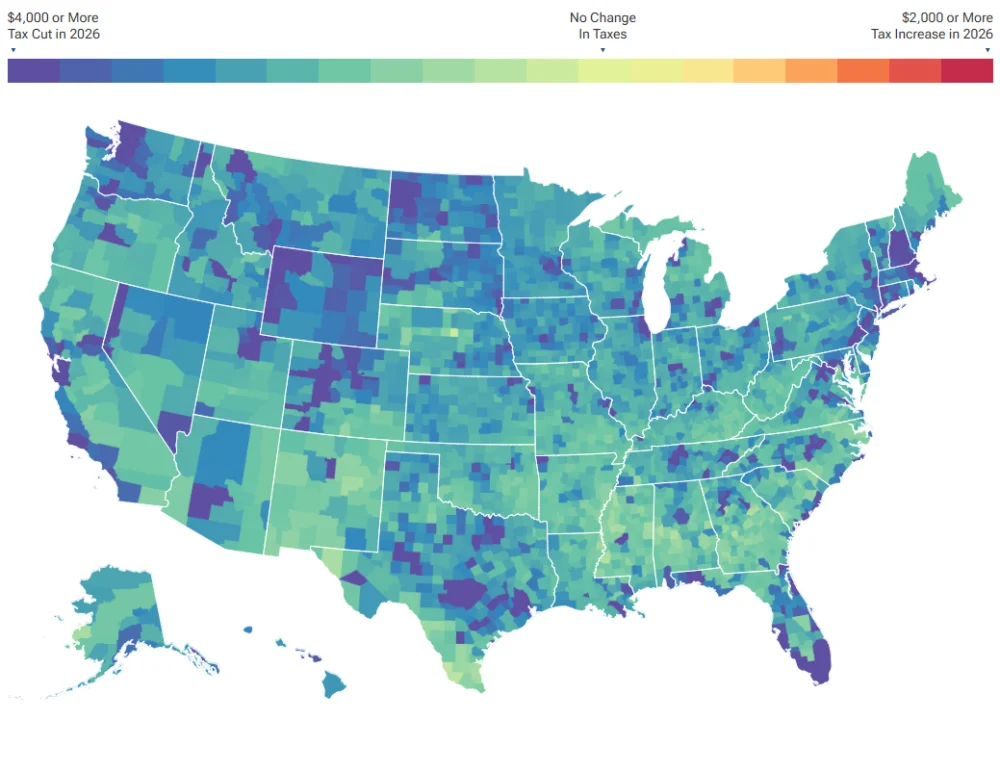

The Tax Foundation’s comprehensive modeling reveals significant geographic variation in the tax benefits conferred by the OBBBA. Analyzing the average change in taxes paid per individual taxpayer across every state and county from 2026 through 2035, the data highlights how the law’s provisions interact with diverse economic landscapes and income distributions. This analysis is conducted relative to a scenario where TCJA individual tax provisions expire, and business taxes increase as previously scheduled beginning in 2026, providing a clear counterfactual.

On a statewide level, the OBBBA is projected to reduce federal taxes for individual taxpayers in every state. However, the magnitude of these reductions varies considerably. In 2026, taxpayers in Wyoming, Washington, and Massachusetts are estimated to experience the largest average tax cuts, receiving $5,478, $5,445, and $5,259 respectively. This concentration of higher average cuts in states known for robust economies, higher average incomes, and significant business activity suggests that the combination of individual and business tax relief disproportionately benefits these regions. Conversely, taxpayers in West Virginia ($2,448) and Mississippi ($2,386) are projected to see the smallest average tax cuts this year. These states, typically characterized by lower average incomes and different industrial structures, may benefit less from provisions tied to higher earnings or extensive capital investments.

Delving into the county level, the disparities become even more pronounced. The largest average tax cuts are predominantly found in affluent mountain resort towns, which often serve as residences for high-net-worth individuals, business owners, and investors. Teton County, Wyoming, for instance, is projected to see an astounding average tax cut of $39,316 per taxpayer in 2026, making it the highest in the nation. Pitkin County, Colorado ($22,717), and Summit County, Utah ($15,477), follow closely, ranking second and third. These figures underscore how the benefits of certain tax provisions, particularly those related to capital income and business ownership, accrue significantly to high-earning taxpayers in specific locales. In stark contrast, rural counties exhibit the smallest average tax cuts. Loup County, Nebraska, for example, is estimated to have an average tax cut of just $731 in 2026, reflecting the lower income levels and less diverse economic activities prevalent in such areas.

Beyond overall averages, specific tax changes within the OBBBA also contribute to geographic variation. The state and local tax (SALT) deduction cap, set at $40,000 initially and then reverting to $10,000 post-2029, is expected to have a more pronounced impact on taxpayers residing in high-tax localities, particularly along the coastal regions of the United States. These areas typically have higher property taxes and state income taxes, making the cap a more significant factor in their overall tax liability compared to states with lower tax burdens.

Economic Ripple Effects: Jobs and Fiscal Trajectories

The OBBBA is not merely a revenue adjustment but a policy designed to foster broader economic growth. The Tax Foundation estimates that the act will lead to an increase of approximately 828,000 full-time equivalent jobs over the long run. This job creation is anticipated through various channels, including increased business investment spurred by bonus depreciation and R&D expensing, enhanced consumer spending resulting from individual tax cuts, and the overall boost to economic activity.

The distribution of these job gains also shows state-level variation, aligning with economic size and industrial composition. California, with its vast economy and diverse industries, is projected to see the largest increase, with over 116,000 new jobs. Texas, another economic powerhouse, is estimated to gain about 72,000 jobs. At the other end of the spectrum, smaller states like Vermont are expected to add around 1,500 new jobs. These figures illustrate the dynamic interplay between national tax policy and localized economic conditions, with larger and more economically complex states generally experiencing greater absolute job growth.

Across all individual tax filers nationally, the average tax cut is projected to be $3,813 in 2026. This average comprises $2,272 from individual tax changes and an additional $1,541 attributable to business tax cuts, reflecting the dual impact of the legislation. The trajectory of these tax cuts, however, is not linear. The average tax cut is projected to fall to $2,590 in 2030. This temporary dip is primarily due to the expiration of certain individual provisions, such as the deductions for tipped and overtime income, which are not made permanent beyond a specific timeframe. Subsequently, the average tax cut is expected to rise again, reaching $3,163 by 2035. This later increase is largely attributed to inflation, which magnifies the nominal value of the permanent tax cuts over time, effectively increasing their real-dollar impact as incomes and prices adjust.

Methodological Underpinnings and Analytical Caveats

The rigorous analysis conducted by the Tax Foundation relies on its General Equilibrium Model to generate conventional revenue estimates at the national level. These estimates form the basis for understanding the geographic distribution of tax changes under the OBBBA’s individual and business provisions. The allocation of these national estimates to individual tax filers within specific counties is achieved using data from the IRS Statistics of Income for individual tax returns from 2022, which provides detailed tax characteristics broken down by county. It is important to note that this specific modeling does not incorporate the impact of the OBBBA’s estate tax changes, focusing primarily on income and business taxation.

The accuracy of this county-level analysis is inherently limited by the granularity and scope of available IRS data, especially concerning newer and more narrowly targeted provisions like the deduction for tipped income. For the business provisions of the OBBBA, the analysis incorporates widely accepted economic incidence assumptions. It posits that the corporate tax burden initially falls predominantly on capital income (90 percent in the first year), gradually shifting towards an even split between capital and labor income in the long run (50 percent capital and 50 percent labor income by the fifth year and beyond). This nuanced approach acknowledges that while businesses nominally pay corporate taxes, the economic burden is ultimately borne by individuals through reduced wages, lower returns on investment, or higher prices. The state-level jobs impacts are allocated based on national job estimates from the Tax Foundation’s General Equilibrium Model, further distributed according to the distribution of labor and capital income across states.

Broader Implications and Future Outlook

The OBBBA’s enactment signifies a critical moment in U.S. fiscal policy, solidifying many of the tax reforms initiated by the TCJA and introducing new measures designed to stimulate economic activity and provide relief to specific taxpayer groups. Proponents of the act laud its potential to enhance economic competitiveness, encourage domestic investment, and offer stability to businesses and families. They argue that by making key provisions permanent, the OBBBA removes uncertainty, fostering an environment conducive to long-term planning and growth. Industry leaders and business associations have largely welcomed the permanence of bonus depreciation and R&D expensing, anticipating a sustained boost in innovation and job creation.

However, the act is not without its critics. Concerns have been raised regarding the distributional equity of the tax cuts, particularly the disproportionate benefits observed in high-income regions and for wealthier taxpayers. Some economists and advocacy groups have pointed to the potential for increased national debt, depending on the dynamic scoring and the long-term revenue implications of the permanent tax reductions. There are also ongoing discussions about the complexity introduced by new deductions and the regional impacts of provisions like the SALT cap, which continue to generate debate about fairness and state sovereignty.

As the OBBBA continues to be implemented and its effects unfold, policymakers, economists, and the public will closely monitor its impact on the national economy, income distribution, and federal revenues. The Tax Foundation’s ongoing analysis, including future updates and detailed breakdowns, will remain an invaluable resource for understanding the multifaceted consequences of this significant tax reform. The long-term success of the OBBBA will ultimately be measured by its ability to deliver sustained economic growth, ensure broad-based prosperity, and maintain fiscal responsibility in the years to come.