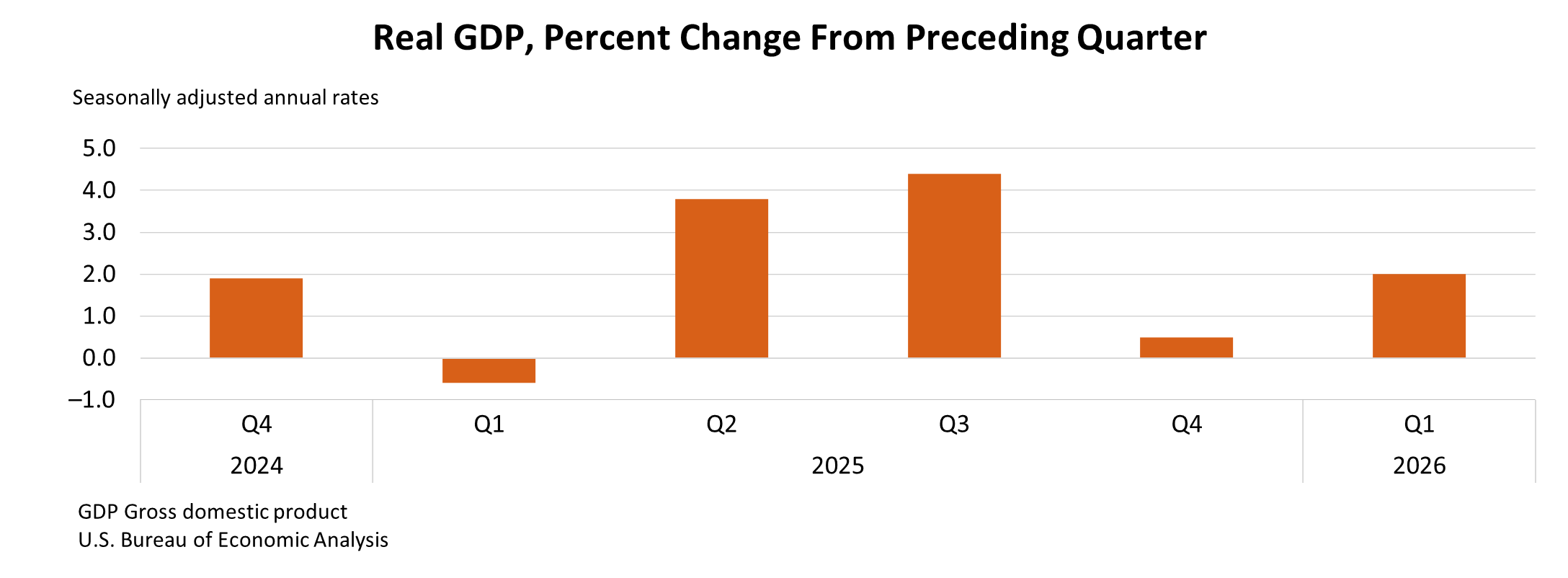

The United States economy demonstrated a significant rebound in the first quarter of 2026, with real gross domestic product (GDP) expanding at a brisk annual rate of 2.0 percent. This acceleration marks a notable improvement from the more modest 0.5 percent growth recorded in the final quarter of 2025, signaling renewed momentum across key sectors of the nation’s economic landscape. The advance estimate, released by the U.S. Bureau of Economic Analysis (BEA), paints a picture of a dynamic economy driven by a confluence of factors, including robust investment, increased exports, steady consumer spending, and a surge in government expenditures.

The BEA’s comprehensive report, drawing on a wide array of source data and economic indicators, highlighted the multifaceted nature of this first-quarter expansion. While consumer spending, a traditional engine of U.S. economic growth, experienced a deceleration in its rate of increase, this was more than compensated for by significant upturns in government spending and exports, alongside an acceleration in investment. Imports, which are a deduction in GDP calculations, also saw an increase, reflecting the interconnectedness of global trade and domestic demand.

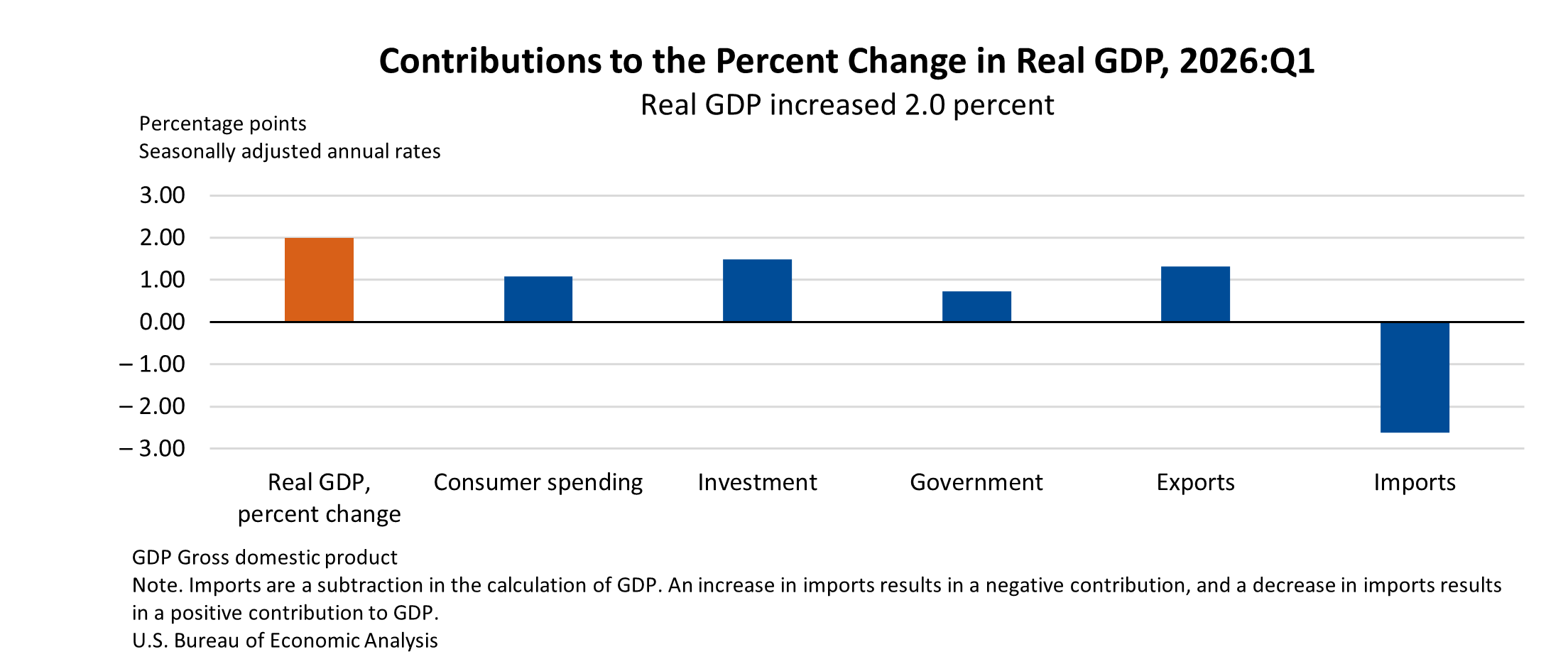

Economic Drivers of First-Quarter Growth

Breaking down the contributors to the GDP increase, the BEA’s detailed analysis revealed the pivotal roles played by various economic components. Investment, encompassing both residential and nonresidential fixed investment, along with changes in private inventories, emerged as a significant driver. Exports, representing goods and services sold to foreign buyers, also saw a substantial uplift, indicating a strengthening global demand for American products and services. Consumer spending, while decelerating, still contributed positively to overall growth, underscoring its enduring importance. Government spending, encompassing federal, state, and local outlays, provided a notable boost, reflecting increased public investment and consumption.

The BEA report provided specific figures that underscore these trends. Real final sales to private domestic purchasers, a key measure of demand from consumers and businesses excluding inventory changes, surged by 2.5 percent in the first quarter of 2026. This figure represents an increase from the 1.8 percent growth observed in the preceding quarter, further emphasizing the underlying strength of private sector demand.

Inflationary Landscape and Price Pressures

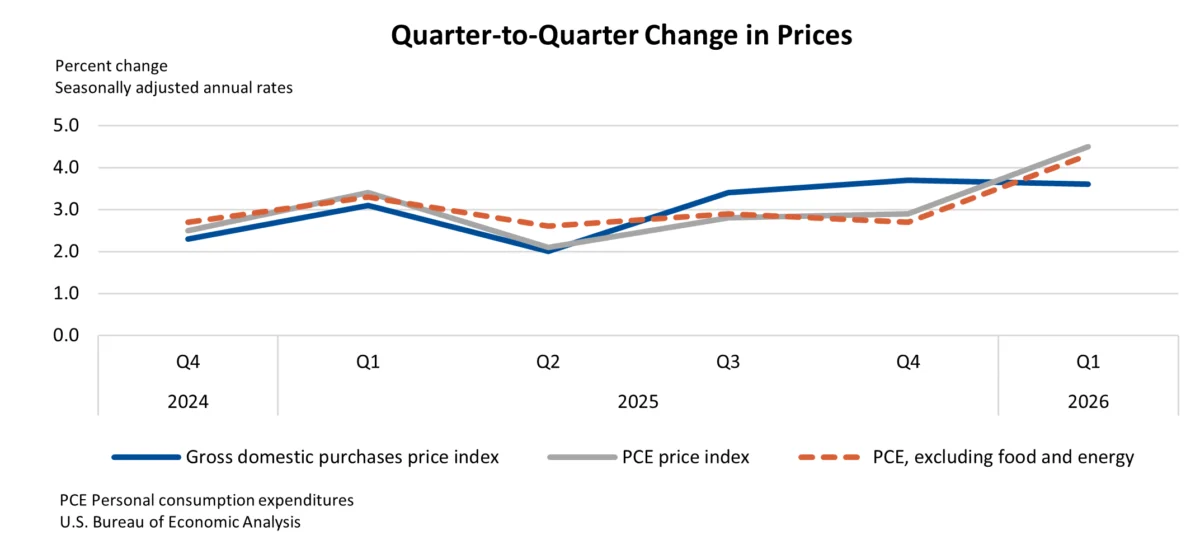

While the headline GDP growth figures were encouraging, the BEA also provided crucial data on inflation. The price index for gross domestic purchases, a broad measure of inflation for goods and services purchased domestically, registered an increase of 3.6 percent in the first quarter. This represents a slight moderation from the 3.7 percent increase seen in the fourth quarter of 2025, suggesting that inflationary pressures, while still present, may be beginning to stabilize.

Of particular interest to policymakers and consumers is the performance of the Personal Consumption Expenditures (PCE) price index, a key inflation gauge closely monitored by the Federal Reserve. The PCE price index saw a significant increase of 4.5 percent in the first quarter, a notable acceleration from the 2.9 percent rise in the previous quarter. The core PCE price index, which excludes volatile food and energy prices, also accelerated, rising by 4.3 percent compared to a 2.7 percent increase in the fourth quarter of 2025. These figures indicate that underlying inflationary pressures, particularly in core components, remain a focus for economic observers.

A Look Back: The Fourth Quarter of 2025

To fully appreciate the first-quarter rebound, it’s essential to contextualize it against the economic performance of the preceding period. The fourth quarter of 2025, while positive, presented a more subdued picture of economic activity. The 0.5 percent annual growth rate reflected a period where certain sectors may have been experiencing a slowdown or consolidation. The BEA’s advance estimate for that quarter indicated that consumer spending was a primary, albeit slower, contributor, with other components of GDP exhibiting more limited growth. The contrast between the fourth quarter’s modest expansion and the first quarter’s invigorated pace highlights the dynamic nature of economic cycles and the impact of various policy and market influences.

Technical Notes and Data Adjustments

The BEA’s release also included important technical notes that shed light on the methodologies and data adjustments employed in its estimations. One such note addressed adjustments made to the PCE price index for legal services in January and March 2026. These adjustments, the BEA clarified, are part of its ongoing efforts to ensure the accuracy and reliability of its economic statistics. The agency explained that such adjustments are made when source data require modifications to reflect real-world economic transactions more precisely.

Furthermore, the report detailed the treatment of refunds related to International Emergency Economic Powers Act (IEEPA) tariffs. In February 2026, a Supreme Court ruling mandated the refunding of certain tariffs deemed unlawful. The BEA clarified that these refunds are classified as capital transfers and, as such, do not directly impact the calculation of quarterly GDP. This distinction is crucial for understanding the composition of economic flows and the specific measures that contribute to GDP.

Implications for Policymakers and Markets

The robust first-quarter GDP growth, coupled with persistent core inflation, presents a nuanced picture for economic policymakers. The Federal Reserve, tasked with maintaining price stability and maximum employment, will likely scrutinize these figures closely. The acceleration in core PCE inflation may reinforce the case for a cautious approach to monetary policy, potentially delaying any significant easing of interest rates.

For businesses, the strong GDP growth suggests a generally favorable operating environment, with increased demand across various sectors. However, the persistent inflation could pose challenges, impacting input costs and potentially consumer purchasing power if not effectively managed. Investment, a key driver of future growth, appears to be on an upward trajectory, which is a positive signal for long-term economic health.

The upturn in exports signals a potential strengthening of international trade relationships and a positive outlook for export-oriented industries. This can provide a buffer against domestic economic fluctuations and contribute to job creation. The increase in government spending, while boosting immediate growth, also raises questions about fiscal sustainability and the long-term impact of public debt.

Future Outlook and Next Release

The BEA indicated that the next release, scheduled for May 28, 2026, at 8:30 a.m. EDT, will provide the second estimate for first-quarter GDP and will also include data on corporate profits. This subsequent release will offer a more refined picture of economic performance and may incorporate additional data that could lead to revisions of the initial advance estimate. Economic analysts will be keenly awaiting these updated figures to assess the durability of the first-quarter growth and to gain further insights into the inflationary trends.

The BEA’s commitment to providing timely and accurate economic data is vital for informed decision-making by government officials, businesses, and the public. The interactive data applications and archived data resources offered by the BEA enable researchers and interested parties to delve deeper into the complexities of the U.S. economy, fostering transparency and a deeper understanding of economic trends. The ongoing series of GDP releases serves as a critical barometer of the nation’s economic health, guiding policy responses and shaping market expectations.

Broader Economic Context and Historical Perspective

To fully grasp the significance of the 2.0 percent GDP growth in the first quarter of 2026, it is beneficial to place it within a broader historical context. While 2.0 percent represents a healthy expansion, the U.S. economy has experienced periods of both higher and lower growth rates in recent decades. For instance, the post-recession recovery periods have often seen higher GDP figures as the economy rebounds from significant downturns. Conversely, periods of global economic uncertainty or domestic policy shifts can lead to slower growth.

The BEA’s data also allows for a comparison of growth rates across different components of GDP over time. Understanding the long-term trends in consumer spending, investment, government spending, and net exports provides valuable insights into structural changes within the economy and the evolving drivers of growth. For example, a sustained shift towards a greater reliance on investment as a growth engine, or a growing contribution from exports, would signal significant transformations in the U.S. economic model.

The persistent inflationary pressures highlighted by the PCE price index figures also warrant historical comparison. While inflation is a natural component of a growing economy, the magnitude and persistence of price increases can significantly influence monetary policy decisions and consumer behavior. Policymakers aim to achieve a delicate balance, fostering economic growth without allowing inflation to erode purchasing power or destabilize the economy. The current figures suggest that this balancing act remains a central challenge.

The Role of Government Spending

The significant contribution of government spending to the first-quarter GDP growth is an element that merits particular attention. This can be attributed to a variety of factors, including increased infrastructure investments, defense spending, or other public sector initiatives. The BEA’s detailed tables, such as Table 1.5.2. Contributions to Percent Change in Real Gross Domestic Product, Expanded Detail, would offer a granular breakdown of which specific government expenditures contributed most significantly.

The impact of government spending on economic growth is a subject of ongoing debate among economists. Proponents argue that it can stimulate demand, create jobs, and address critical societal needs. Critics, however, often raise concerns about the potential for increased national debt, crowding out of private investment, and inefficiencies in public spending. The sustainability of government spending as a primary driver of growth will be a key consideration for fiscal policymakers in the coming years.

Consumer Spending Dynamics

Despite a deceleration in its growth rate, consumer spending remains the largest component of U.S. GDP and a crucial indicator of economic health. The fact that it continued to contribute positively to growth in the first quarter, even as other components accelerated, underscores its resilience. However, the deceleration itself warrants attention. Factors such as rising interest rates, concerns about inflation, or shifts in consumer confidence could be contributing to this trend.

Understanding the underlying reasons for the slowdown in consumer spending is vital for forecasting future economic performance. If this deceleration is driven by fundamental economic challenges, it could signal a potential headwind for overall growth. Conversely, if it is a temporary adjustment or a reflection of a shift towards more deliberate spending patterns, its impact may be less significant.

Conclusion: A Mixed but Promising Economic Landscape

The U.S. economy in the first quarter of 2026 presented a picture of renewed vitality, characterized by a significant acceleration in real GDP growth. The contributions from investment, exports, and government spending were particularly strong, compensating for a moderation in the pace of consumer spending. While inflationary pressures, especially in core components, remain a concern and will likely influence monetary policy decisions, the overall expansion signals a positive trajectory. The BEA’s detailed data and technical explanations provide crucial context for understanding these developments, allowing for informed analysis of the economic landscape and its future implications. The coming months will be critical in observing whether this growth momentum can be sustained and how policymakers will navigate the interplay of expansionary forces and inflationary headwinds.