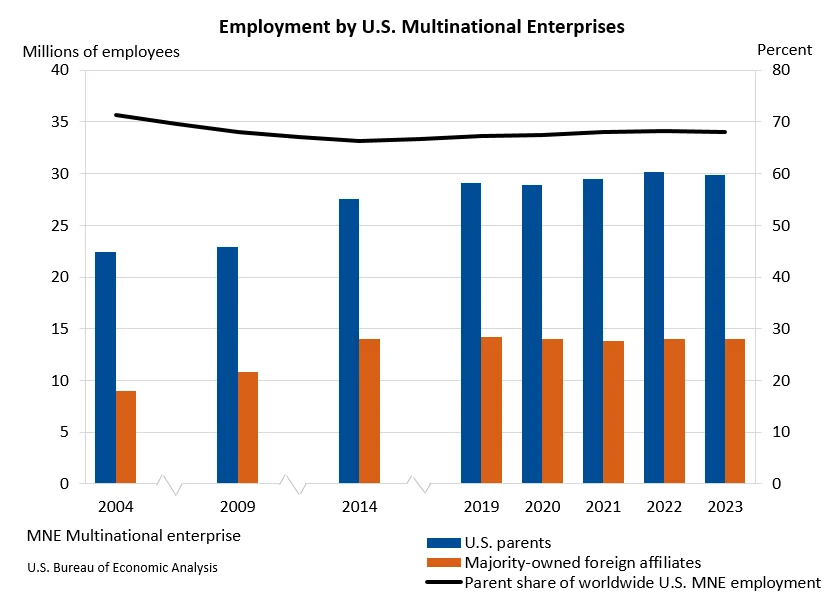

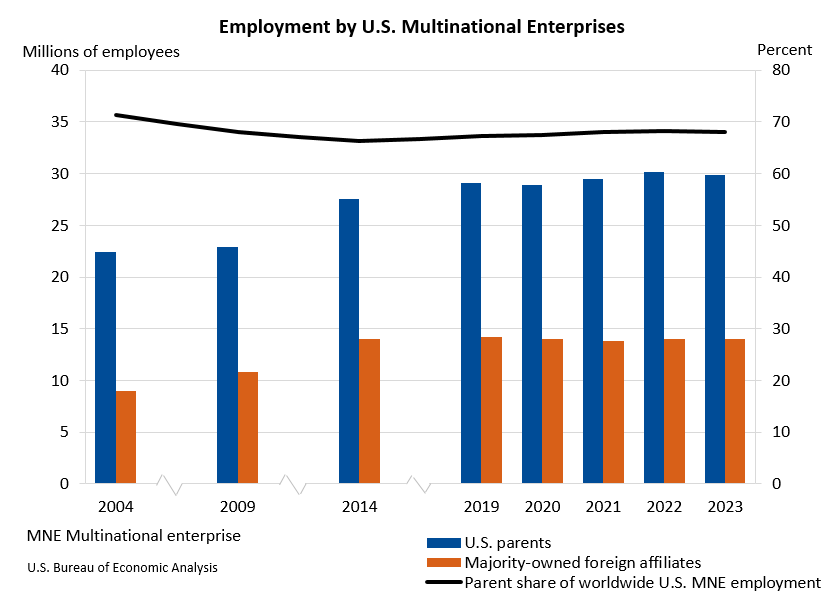

Worldwide employment by U.S. multinational enterprises (MNEs) experienced a marginal decrease of 0.4 percent in 2023, reaching an estimated 43.9 million workers. This represents a slight contraction from the revised figure of 44.1 million workers recorded in 2022, according to the latest statistics released by the U.S. Bureau of Economic Analysis (BEA). The data, which offers a comprehensive look at the operational and financial activities of U.S. parent companies and their foreign affiliates, highlights a subtle but significant shift in the global employment landscape for American corporations.

Domestic Employment Contraction Outpaces Global Slight Decline

A closer examination of the BEA data reveals that the overall dip in global employment was primarily driven by a more pronounced decrease in employment within the United States. U.S. parent companies saw their domestic workforce shrink by 0.8 percent in 2023, bringing the total to 29.9 million workers. Despite this decline, U.S. parents continue to represent the vast majority of employment generated by U.S. MNEs worldwide, accounting for 68.1 percent of the total workforce. This share, however, is a fractional decrease from 68.3 percent in the preceding year, underscoring the ongoing trend of U.S. companies looking beyond domestic borders for expansion and talent.

In contrast, employment abroad by foreign affiliates of U.S. MNEs showed a modest increase of 0.2 percent, reaching 14.0 million workers. This growth, though small, signifies a growing reliance on international labor pools, with foreign affiliates now constituting 31.9 percent of the total global employment footprint of U.S. MNEs. This dynamic suggests a strategic reallocation of resources and a growing emphasis on global operational efficiency by American multinational corporations.

U.S. Parent Companies’ Share of Private Industry Employment Declines

The impact of the domestic employment contraction is further illustrated by the shrinking proportion of total private industry employment in the United States attributed to U.S. parent companies. In 2023, these entities accounted for 21.9 percent of all private sector jobs, a decrease from 22.5 percent in 2022. This trend indicates that while U.S. MNEs remain significant employers domestically, their relative contribution to the overall U.S. job market is gradually diminishing.

The primary sectors for U.S. parent company employment remain consistent, with manufacturing leading the pack. Following manufacturing, significant employment is found in "other industries," notably transportation and warehousing, and in the retail trade sector. These sectors have historically been pillars of employment for U.S. multinational corporations, reflecting their broad operational reach across the American economy.

Geographically, employment abroad by majority-owned foreign affiliates of U.S. MNEs was concentrated in key international markets. India, Mexico, and the United Kingdom emerged as the top destinations for employment by these foreign arms of U.S. companies. This concentration highlights strategic investment and operational hubs established by U.S. businesses in these regions, likely driven by factors such as market access, labor costs, and established supply chains.

Economic Value Added Reflects Global Economic Performance

Beyond employment figures, the BEA report also sheds light on the economic contribution of U.S. MNEs through their value added, a measure closely aligned with their impact on Gross Domestic Product (GDP). Worldwide current-dollar value added by U.S. MNEs saw a slight decrease of 0.6 percent, totaling $6.9 trillion. This overall decline mirrors the subtle contraction in global employment.

The contribution of U.S. parents to the U.S. economy, measured by their direct value added to the nation’s GDP, experienced a more significant dip of 1.0 percent, amounting to $5.3 trillion. Consequently, the share of total U.S. private-industry value added attributable to U.S. parents fell from 23.1 percent in 2022 to 21.4 percent in 2023. This indicates a reduced direct economic output from U.S.-based operations of these multinational giants relative to the broader U.S. private sector.

Conversely, the value added by majority-owned foreign affiliates experienced a modest increase of 0.8 percent, reaching $1.6 trillion. This growth in foreign affiliate value added suggests that while the U.S. parent companies’ direct economic contribution may have softened, their international operations continued to generate economic value. The top countries contributing to this foreign affiliate value added were the United Kingdom, Canada, and Ireland, indicating these regions’ significant role in the global economic performance of U.S. MNEs.

Investment in Capital and Innovation Remains Robust

Despite the slight contractions in employment and overall value added, U.S. MNEs demonstrated a strong commitment to investment in both physical assets and research and development. Worldwide expenditures for property, plant, and equipment by U.S. MNEs surged by a notable 7.5 percent, reaching $1.1 trillion. This substantial increase signals a continued focus on expanding operational capacity and modernizing infrastructure globally.

Of this total, U.S. parents accounted for $886.1 billion in capital expenditures, while majority-owned foreign affiliates invested $216.2 billion. The significant investment by U.S. parents underscores a domestic commitment to capital projects, even as overall employment numbers saw a slight decline. This could indicate investments in automation, efficiency improvements, or expansion in specific high-growth domestic sectors.

Furthermore, worldwide research and development (R&D) expenditures by U.S. MNEs also saw a robust increase of 7.5 percent, reaching $558.3 billion. This parallel growth in capital expenditures and R&D spending highlights a strategic prioritization of innovation and future growth. U.S. parents were the primary drivers of this R&D investment, accounting for $476.6 billion, while foreign affiliates contributed $81.7 billion. The substantial R&D outlay by U.S. parent companies suggests a continued emphasis on developing new technologies, products, and services, which is crucial for maintaining competitive advantage in the global marketplace.

Historical Context and Revisions

The statistics released by the BEA are part of a recurring annual survey that tracks the activities of U.S. multinational enterprises. The data for 2023 is preliminary, meaning it is subject to revision as more comprehensive source data becomes available. The BEA also released revised statistics for 2022, incorporating newly available and revised source data. These revisions are crucial for ensuring the accuracy and reliability of the long-term trends observed in the data.

The preliminary statistics for 2022, which were initially released in August 2024, were further detailed in the September 2024 issue of the Survey of Current Business. The revisions to the 2022 data, as detailed in a comparison table provided by the BEA, show minor adjustments across key metrics. For instance, the number of employees for U.S. parents was revised from a preliminary estimate of 30,240.8 thousand to 30,120.1 thousand. Similarly, value added figures and expenditures for property, plant, and equipment, and research and development saw minor adjustments for both U.S. parents and their majority-owned foreign affiliates. These revisions are a standard part of the statistical process, ensuring that the most accurate picture of economic activity is presented.

Broader Implications and Future Outlook

The slight decrease in worldwide employment by U.S. MNEs in 2023, coupled with the declining share of domestic employment, suggests a continuing trend of globalization in corporate operations. While U.S. parent companies remain the bedrock of these enterprises, their foreign affiliates are playing an increasingly vital role in both employment and value creation. This dynamic can be attributed to several factors, including the pursuit of new markets, access to diverse talent pools, strategic cost management, and the optimization of global supply chains.

The robust increases in capital expenditures and R&D spending, particularly by U.S. parent companies, indicate a forward-looking strategy focused on innovation and long-term growth. This suggests that despite the modest employment contraction, U.S. MNEs are investing in the future, potentially through automation, technological advancements, and the development of new intellectual property. These investments are crucial for maintaining competitiveness in an increasingly interconnected and rapidly evolving global economy.

The data also highlights the economic significance of key international markets for U.S. businesses. Countries like India, Mexico, and the United Kingdom are not only destinations for employment but also significant contributors to the value generated by U.S. MNEs. This underscores the importance of international trade relations and the interconnectedness of global economies.

Looking ahead, the BEA will release its next set of statistics on the activities of U.S. Multinational Enterprises in November 2026, focusing on the 2024 data. This upcoming release will provide further insights into the ongoing trends and shifts in the global operational landscape of U.S. multinational corporations. Analysts and policymakers will be keenly observing these future releases to gauge the sustained impact of global economic conditions, geopolitical developments, and technological advancements on the employment, investment, and economic output of these influential global entities. The BEA’s comprehensive data collection and dissemination efforts remain essential for understanding the complex and dynamic nature of U.S. multinational enterprise activity and its impact on both domestic and international economies.