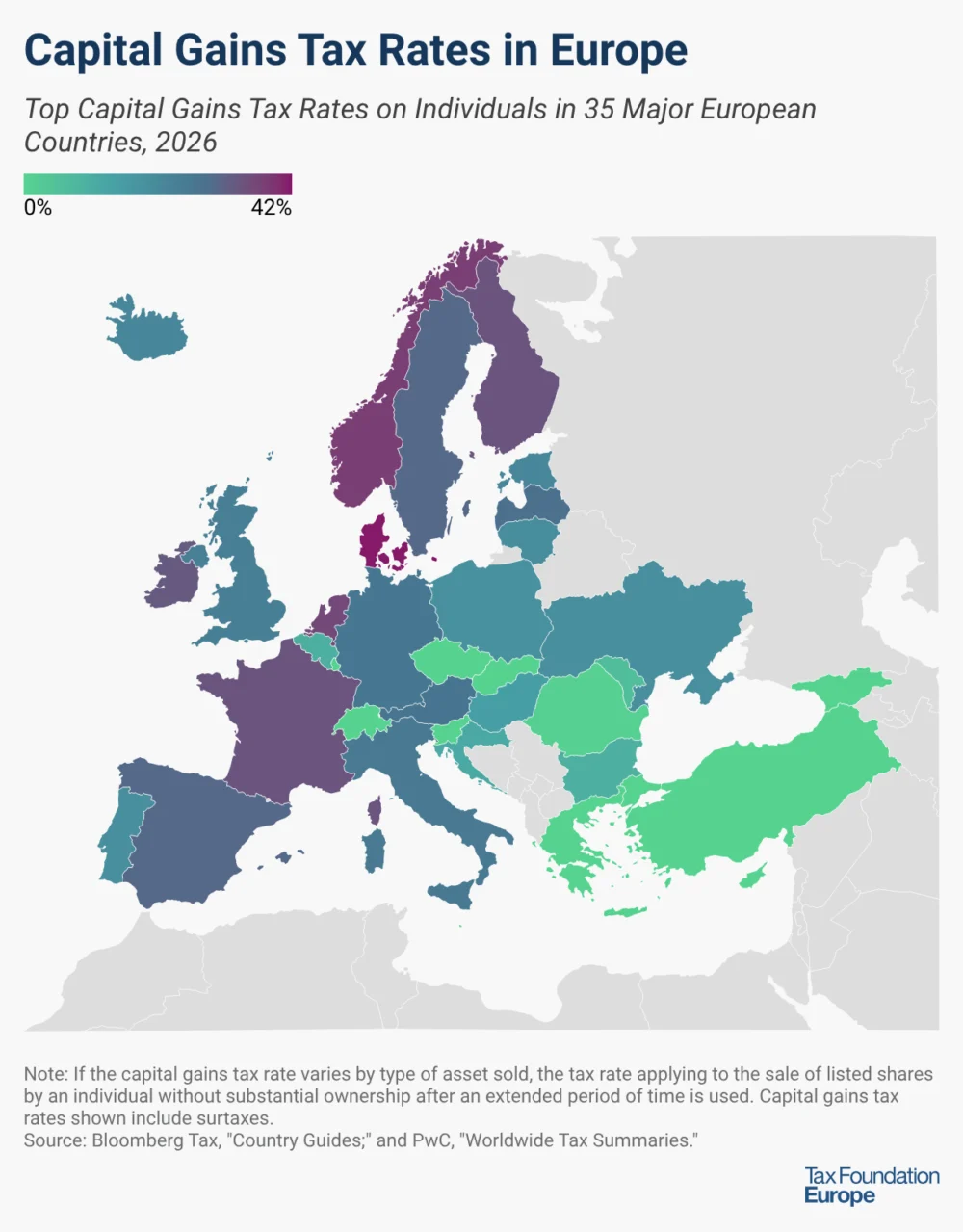

Europe presents a highly diverse landscape for capital gains taxation in 2026, with top marginal rates on individuals owning long-held listed shares without substantial ownership ranging dramatically from a full exemption in several nations to a high of 42 percent in Denmark. This intricate tapestry of tax regimes reflects varying economic philosophies, fiscal priorities, and approaches to wealth accumulation across the continent, significantly influencing investment decisions, capital mobility, and national competitiveness. The data, encompassing both European Union member states and other key European economies, reveals a complex environment shaped by exemptions, holding periods, surtaxes, and specific thresholds designed to balance revenue generation with investment incentives.

A Broad Spectrum: From Zero to Over Forty Percent

An analysis of the projected 2026 capital gains tax (CGT) rates for individuals holding long-term listed shares without substantial ownership highlights the considerable divergence in European fiscal policy. On one end of the spectrum, eleven countries — Cyprus, Czech Republic, Georgia, Greece, Luxembourg, Malta, Slovakia, Slovenia, Switzerland, Turkey, and partially Moldova — effectively impose a zero percent top marginal CGT under specific conditions. These conditions typically revolve around holding periods, the nature of the asset, or its listing status, signaling a strategic choice to attract investment and foster capital market activity. For instance, Cyprus exempts shares listed on any recognised stock exchange, while the Czech Republic and Slovakia offer exemptions for shares held for at least three and one year respectively, provided they are not part of business assets. Slovenia extends this exemption to assets held for over 15 years, demonstrating a clear incentive for long-term investment.

Conversely, a substantial number of nations levy significant taxes on capital gains. Denmark leads with the highest top marginal rate at 42 percent for share income exceeding DKK 79,400, followed closely by Norway at 37.8 percent, which applies a 1.72 multiplier to gains before a 22 percent tax rate. The Netherlands imposes a 36 percent flat rate on a deemed annual return from net asset value, rather than on actual gains, reflecting a unique approach to taxing wealth. Finland and France both stand at 34 percent, with France adding a 4 percent surcharge for high-income earners on top of its 30 percent flat tax. Ireland’s rate is 33 percent, while Spain and Sweden both apply a 30 percent rate. These higher rates often reflect a policy preference for greater wealth redistribution or a broader tax base, aiming to fund public services and reduce income inequality.

The average top marginal capital gains tax rate across the 35 European countries surveyed is approximately 18.24 percent, illustrating that while high rates exist, a significant portion of the continent falls within a moderate range. This average, however, masks the extreme variations and the specific conditions that often dictate the actual tax burden on investors.

Detailed Examination of Key Tax Regimes

Zero or Near-Zero Tax Jurisdictions:

The strategic use of exemptions is a defining characteristic of countries offering zero or minimal capital gains tax.

- Cyprus, Malta, Switzerland, Turkey: These countries generally exempt capital gains from shares listed on recognised stock exchanges, aiming to position themselves as attractive financial hubs. Turkey’s exemption is contingent on a minimum holding period of one year for exchange-traded shares, extending to two years for joint-stock companies.

- Czech Republic, Georgia, Slovakia, Slovenia: These nations utilize holding periods as a primary criterion for exemption. The Czech Republic requires a three-year holding period for joint stock company shares (five years for limited liability companies), while Slovakia exempts shares held for over one year if not considered business assets. Georgia offers a general exemption for shares held over two years, and Slovenia’s rate drops to 0 percent after 15 years, gradually decreasing from a maximum of 25 percent for shorter holding periods.

- Luxembourg: Capital gains are tax-exempt if movable assets like shares are held for at least six months by a non-large shareholder, though a dependency contribution of 1.4 percent applies to taxable gains.

- Greece: While generally exempt, a 15 percent rate applies if an individual holds at least 0.5 percent of the listed entity’s share capital, suggesting a focus on smaller, less influential shareholdings.

- Moldova: Capital gains are taxed at 50 percent of the Personal Income Tax (PIT) rate, resulting in a low 6 percent top marginal rate.

These policies are often designed to stimulate domestic investment, attract foreign capital, and enhance the liquidity and depth of local stock exchanges.

Moderate Tax Environments (10% – 20%):

A substantial number of European countries opt for a moderate approach, with rates typically ranging from 10 percent to 20 percent.

- Belgium and Bulgaria (10%): Bulgaria applies a flat 10 percent PIT rate to capital gains. Belgium’s system is more nuanced; capital gains from financial assets exceeding an annual exemption of EUR 10,000 are taxed at 10 percent, with a carry-forward mechanism for the exemption. Speculative gains, however, can be taxed at 33 percent, indicating a distinction between regular investment and short-term trading.

- Croatia (12%), Hungary (15%), Poland (19%), Portugal (19.6%), Ukraine (19.5%), Lithuania (20%): These countries largely employ flat rates, making the tax burden predictable for investors. Portugal’s system includes an interesting incentive for long-term holdings, with capital gains becoming progressively tax-free for holding periods exceeding two years (10% tax-free for 2-5 years, 20% for 5-8 years, and 30% after 8 years), although a 28 percent flat rate applies if assets were held for less than a year.

- Iceland (22%), Estonia (22%): These rates are slightly higher but still fall within the moderate band. Iceland offers an exemption for capital income up to ISK 300,000 per year. Estonia’s rate is noted to be up from 20 percent in 2024, indicating a recent policy shift.

- Romania (1% or 3%): Romania offers one of the lowest effective rates for capital gains, with a 1 percent tax for holding periods longer than 356 days and 3 percent for shorter periods, primarily through intermediaries. This policy clearly aims to foster robust capital market activity.

Higher Tax Jurisdictions (Above 20%):

Countries with higher capital gains tax rates often feature more complex structures, including surtaxes or specific calculations.

- Austria (27.5%), Germany (26.4%), Italy (26%): These countries apply relatively straightforward flat rates, with Germany including a 5.5 percent solidarity surcharge on its 25 percent flat tax.

- Latvia (28.5%): Latvia’s 25.5 percent flat rate is augmented by an additional 3 percent for high-income earners, pushing the top marginal rate higher.

- United Kingdom (24%): The UK maintains a 24 percent rate, with an annual exemption of EUR 1,270 for individuals.

- Netherlands (36%): As noted, the Netherlands taxes a "deemed annual return" on net asset value rather than actual gains, with the deemed return varying by the total value of assets owned, and the tax applied above an annual exemption of EUR 59,357 per person. This system, distinct from direct capital gains taxation, aims to tax the potential yield from wealth.

- Norway (37.8%): The 22 percent general capital gains rate is significantly amplified by a 1.72 multiplier applied to gains from the sale of shares, resulting in one of Europe’s highest effective rates.

- Denmark (42%): With a progressive structure, Denmark taxes share income up to DKK 79,400 at 27 percent, with any excess taxed at 42 percent, making it the highest rate among the surveyed nations.

Economic Rationale and Policy Implications

The variations in capital gains tax rates across Europe stem from a blend of economic, social, and political considerations. Governments typically aim to:

- Generate Revenue: CGT provides a source of income for public services, though its contribution to overall tax revenue can fluctuate significantly with market performance.

- Promote Fairness and Redistribution: Higher CGT rates can be seen as a tool to address wealth inequality, ensuring that those who benefit most from capital appreciation contribute a larger share to society.

- Influence Investment Behavior: Lower rates and generous exemptions are often intended to encourage long-term investment, foster entrepreneurship, and attract foreign direct investment (FDI). Conversely, higher rates might disincentivize certain types of capital deployment.

- Enhance Capital Market Efficiency: Policies like exemptions for listed shares or longer holding periods aim to stimulate trading activity and improve the liquidity of stock exchanges.

- Maintain Competitiveness: Countries frequently adjust their tax policies to remain competitive within the global and European economic landscape, trying to prevent capital flight to lower-tax jurisdictions.

Implications for Investors and Capital Mobility

For individual investors and wealth managers, these disparate tax rates present both challenges and opportunities. The varying thresholds, holding periods, and surtaxes necessitate careful planning and an understanding of each jurisdiction’s specific rules. For instance, an investor in a high-tax country might consider structuring investments through vehicles or jurisdictions with more favourable CGT regimes, though anti-avoidance rules and residency requirements often complicate such strategies.

The existence of numerous zero-tax or low-tax jurisdictions within Europe creates a degree of tax competition, influencing where businesses choose to list and where high-net-worth individuals choose to reside or invest. This competition can put pressure on higher-tax countries to reconsider their rates, particularly if they perceive a significant outflow of capital or a slowdown in domestic investment. However, the political will to reduce CGT often clashes with public demands for greater wealth taxation and social equity.

Recent Trends and Future Outlook

While the data specifically pertains to 2026, the "Additional Comments" column reveals ongoing dynamism in capital gains tax policy. Estonia’s rate increase from 20 percent in 2024 to 22 percent in 2026, for example, signals a trend towards slightly higher taxation in some areas. Conversely, the continued prevalence of exemptions based on holding periods or listing status in countries like the Czech Republic, Slovakia, and Slovenia underscores a sustained commitment to incentivizing long-term capital formation.

The broader international discussion on wealth taxation, including proposals for global minimum taxes on certain capital gains, could also influence future European policies. While direct taxation remains largely within national sovereignty, increasing calls for greater tax harmonisation or cooperation could lead to shifts in the long term, potentially reducing the extreme disparities observed today. However, for 2026, the landscape remains one of significant national diversity, presenting a complex but navigable environment for investors and policymakers alike.

Conclusion

The 2026 outlook for capital gains tax rates in Europe paints a picture of profound diversity, marked by a wide range of top marginal rates and intricate exemption mechanisms. From the zero percent rates offered by several nations under specific conditions to Denmark’s leading 42 percent, Europe continues to be a patchwork of fiscal approaches. These variations are not arbitrary; they are the result of deliberate policy choices aimed at balancing revenue generation, wealth redistribution, and the attraction of capital. For investors, understanding this complex landscape is paramount to making informed decisions, while for governments, the challenge remains to craft tax policies that foster economic growth, maintain competitiveness, and meet societal expectations in an ever-evolving global financial environment. The detailed insights into specific country regimes underscore that capital gains taxation in Europe is far from a monolithic entity, demanding nuanced attention to both the rates and the conditions under which they apply.