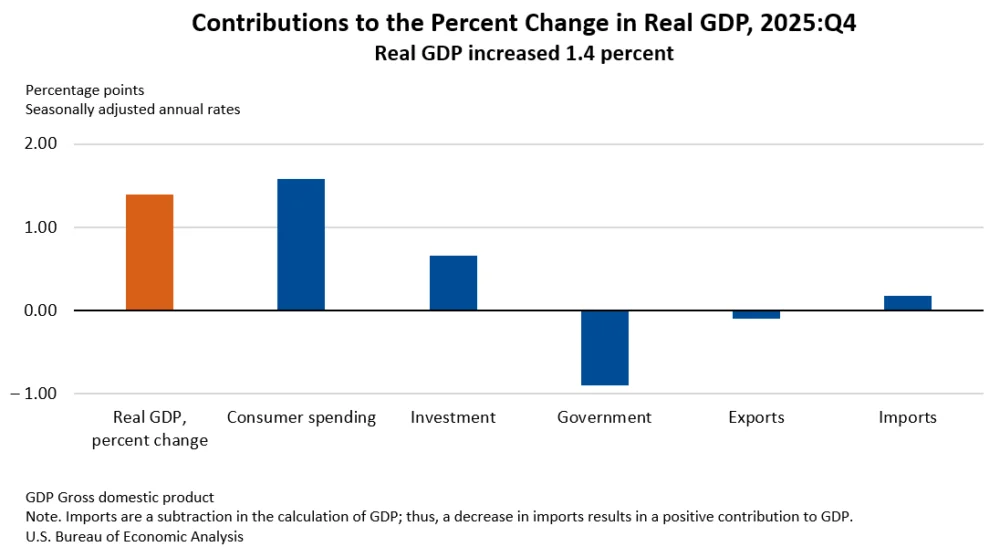

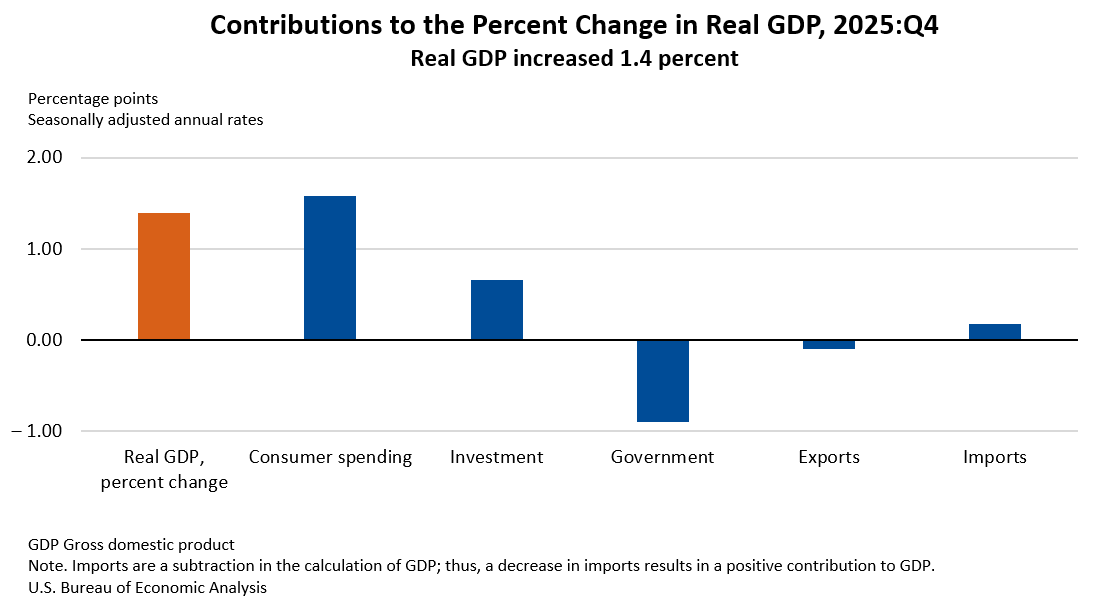

The United States economy experienced a notable slowdown in its growth trajectory during the fourth quarter of 2025, with real gross domestic product (GDP) expanding at an annualized rate of 1.4 percent. This figure, as revealed by the advance estimate from the U.S. Bureau of Economic Analysis (BEA), represents a significant deceleration from the robust 4.4 percent growth recorded in the third quarter of the same year. The release of this crucial economic indicator was notably delayed, having been rescheduled from its original January 29, 2026, publication date due to the extensive October-November 2025 government shutdown.

The fourth quarter’s economic performance was shaped by a complex interplay of factors. Growth was primarily propelled by upticks in consumer spending and investment. However, these positive contributions were substantially tempered by contractions in government spending and exports. Imports, which are a deduction in the calculation of GDP, also decreased, further influencing the net growth figure. This dynamic presents a picture of an economy grappling with both internal momentum and external headwinds, exacerbated by the recent federal shutdown.

Economic Landscape: Q4 2025 Performance and Contributing Factors

The 1.4 percent annual growth rate in real GDP for the fourth quarter of 2025 signifies a cooling of the economic engine compared to the vigorous expansion seen in the preceding quarter. While consumer spending and investment provided a foundational boost, their upward momentum was insufficient to fully offset declines in other key areas. Government spending experienced a downturn, a factor that can often be linked to shifts in fiscal policy or the lingering effects of budgetary impasses. Similarly, exports faced headwinds, potentially influenced by global economic conditions or trade dynamics.

A closer examination of the BEA’s data reveals that real final sales to private domestic purchasers, a metric that encapsulates consumer spending and gross private fixed investment, saw a more moderate increase of 2.4 percent in the fourth quarter, down from 2.9 percent in the third quarter. This suggests that while private domestic demand remained a positive force, its pace of expansion also softened.

Inflationary Pressures and Consumer Price Dynamics

Alongside the GDP figures, the BEA also reported on inflationary trends. The price index for gross domestic purchases, a broad measure of inflation for goods and services purchased domestically, rose by 3.7 percent in the fourth quarter. This marks an acceleration from the 3.4 percent increase observed in the third quarter, indicating a general upward trend in the cost of goods and services.

The personal consumption expenditures (PCE) price index, a key inflation gauge closely watched by the Federal Reserve, increased by 2.9 percent in the fourth quarter, a slight uptick from the 2.8 percent rise in the third quarter. However, when excluding the volatile categories of food and energy, the core PCE price index saw a deceleration, increasing by 2.7 percent compared to 2.9 percent in the previous quarter. This divergence highlights that while overall price pressures may be mounting, the underlying inflation excluding food and energy showed signs of moderation.

The BEA noted that for the October 2025 data, which was impacted by the government shutdown, imputed price indexes were derived using the geometric mean of September and November Consumer Price Index (CPI) data from the Bureau of Labor Statistics (BLS). This imputation was necessary due to the BLS’s inability to collect October CPI data during the shutdown.

Impact of the October-November 2025 Government Shutdown

The prolonged government shutdown from October to November 2025 cast a discernible shadow over the economic data for the fourth quarter. While the full extent of its impact is difficult to precisely quantify, the BEA estimated that the reduction in labor services provided by federal employees alone subtracted approximately 1.0 percentage point from real GDP growth during the quarter. This highlights the significant disruption that federal government operations can have on broader economic activity, even when back pay is eventually disbursed. The shutdown also created a temporary anomaly in federal employee compensation, with furloughed employees receiving back pay, which was reflected as an increase in the prices paid for federal employee compensation rather than an impact on current-dollar federal compensation.

Full-Year 2025 Economic Performance

Looking at the entirety of 2025, real GDP increased by 2.2 percent compared to the 2024 annual level. This represents a moderation from the 2.8 percent growth recorded in 2024. The primary drivers of growth for the full year were again consumer spending and investment.

Inflationary trends for the full year also saw some shifts. The price index for gross domestic purchases increased by 2.6 percent in 2025, an acceleration from the 2.4 percent increase in 2024. The PCE price index also rose by 2.6 percent in 2025, mirroring the increase from the previous year. However, the core PCE price index, excluding food and energy, showed a slight deceleration, increasing by 2.8 percent in 2025 compared to 2.9 percent in 2024. This suggests that while headline inflation picked up, the more persistent underlying inflation pressures may have begun to ease slightly by the end of the year.

Key Data Points and Revisions

The advance estimate released by the BEA provides the initial assessment of economic performance. This will be followed by a second estimate on March 13, 2026, and a third and final estimate on April 9, 2026. These subsequent estimates will incorporate more comprehensive data and may lead to revisions of the initial figures.

The BEA also announced ongoing improvements to its news release packages, including enhanced links to its online Interactive Data Tables. This move aims to reduce duplication and direct users to the most current and complete data available, with PDF and Excel versions of news release tables being phased out beginning with the third estimate for the fourth quarter of 2025.

Broader Economic Context and Implications

The 1.4 percent GDP growth in the fourth quarter of 2025, while positive, signals a significant shift in the economic landscape. The deceleration from 4.4 percent in the third quarter suggests that the economy is entering a phase of more modest expansion. This slowdown could be attributed to a confluence of factors, including the lagged effects of monetary policy tightening by the Federal Reserve, persistent inflationary pressures impacting consumer purchasing power, and the direct and indirect consequences of the government shutdown.

For policymakers, the data presents a complex picture. The moderation in growth may alleviate some concerns about overheating, but the uptick in headline inflation, particularly the gross domestic purchases price index, warrants continued attention. The Federal Reserve will likely weigh these conflicting signals carefully as it calibrates its future monetary policy decisions. A sustained period of lower growth coupled with elevated inflation could present a challenging scenario, potentially necessitating difficult trade-offs between economic expansion and price stability.

The decrease in government spending and exports also points to potential vulnerabilities. A decline in government expenditure can have ripple effects across various sectors, particularly those reliant on public contracts or funding. Furthermore, a slowdown in export growth could indicate weakening global demand or increased competition for U.S. goods and services abroad.

Consumer Spending and Investment: Pillars of Growth

Despite the overall deceleration, the continued growth in consumer spending and investment remains a critical positive for the U.S. economy. Consumer spending, which accounts for a significant portion of GDP, is often driven by factors such as employment levels, wage growth, and consumer confidence. The sustained increase in this category, even if at a slower pace, suggests underlying resilience in household demand.

Investment, encompassing business spending on equipment, structures, and intellectual property, is a key indicator of future economic potential. An increase in investment suggests that businesses remain optimistic about long-term prospects and are willing to commit resources to expansion and innovation. However, the deceleration in the growth of real final sales to private domestic purchasers suggests that the pace of this private sector dynamism may also be tempering.

Looking Ahead: Challenges and Opportunities

The economic outlook for 2026 will be shaped by how effectively the nation navigates the lingering effects of the government shutdown, the trajectory of inflation, and the evolving global economic environment. The BEA’s revised estimates for the fourth quarter and the upcoming data for the first quarter of 2026 will be crucial in discerning whether the slowdown represents a temporary pause or the beginning of a more sustained period of lower growth.

The BEA’s commitment to modernizing its data dissemination methods, including the move towards online interactive tables, signals a proactive approach to making economic data more accessible and user-friendly. This transparency is vital for researchers, businesses, and the public to understand and interpret the complex economic signals emanating from the U.S. economy.

As the nation moves forward, the interplay between domestic demand, inflationary pressures, and external economic forces will continue to define the economic narrative. The 1.4 percent growth in the fourth quarter of 2025 serves as a critical data point, underscoring the need for careful analysis and strategic policy responses to foster sustainable and stable economic growth.

Technical Notes on Data Imputation and Shutdown Effects

The Bureau of Economic Analysis has provided detailed technical notes to clarify the methodologies used in compiling the GDP estimates, particularly in light of the challenges posed by the government shutdown. The imputation of missing October 2025 price data, a direct consequence of the shutdown, involved a specific statistical approach. For consumer price indexes (CPI), the BEA employed the geometric mean of the September and November CPI data to derive seasonally adjusted figures for October. Non-seasonally adjusted figures were then generated by applying the previous year’s seasonal adjustment factors. This method aims to provide the best possible approximation in the absence of direct data collection.

The impact of the federal government shutdown on federal government spending and labor services was also a significant consideration. While the BEA could not isolate the exact financial implications of every aspect of the shutdown, it did quantify the estimated reduction in labor services. The subtraction of approximately 1.0 percentage point from real GDP growth due to this factor is a substantial figure that underscores the economic disruption caused by the lapse in appropriations. The BEA’s FAQ on the shutdown’s impact provides further context on how these effects were estimated and incorporated into the GDP calculations.

The release schedule for future GDP estimates also highlights the iterative nature of economic data. The advance estimate provides an early snapshot, which is then refined through subsequent releases. This phased approach allows for the incorporation of more comprehensive and finalized data, leading to a more accurate representation of economic activity over time. The BEA’s commitment to timely yet accurate reporting is a cornerstone of its role in providing essential economic intelligence.