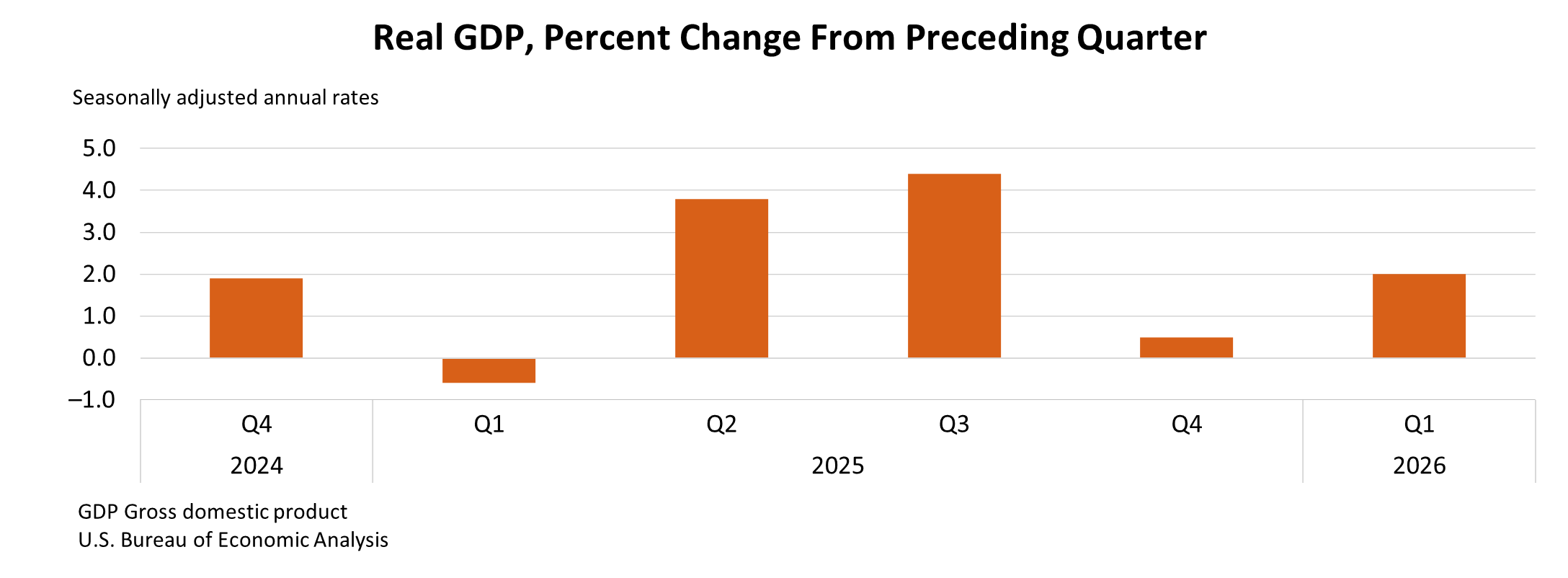

The U.S. Bureau of Economic Analysis (BEA) announced today that real gross domestic product (GDP) expanded at an annual rate of 2.0 percent in the first quarter of 2026, a significant acceleration from the 0.5 percent growth recorded in the final quarter of 2025. This advance estimate signals a strengthening of economic activity heading into the new year, driven by a diverse set of contributing factors.

Key Drivers of First Quarter Expansion

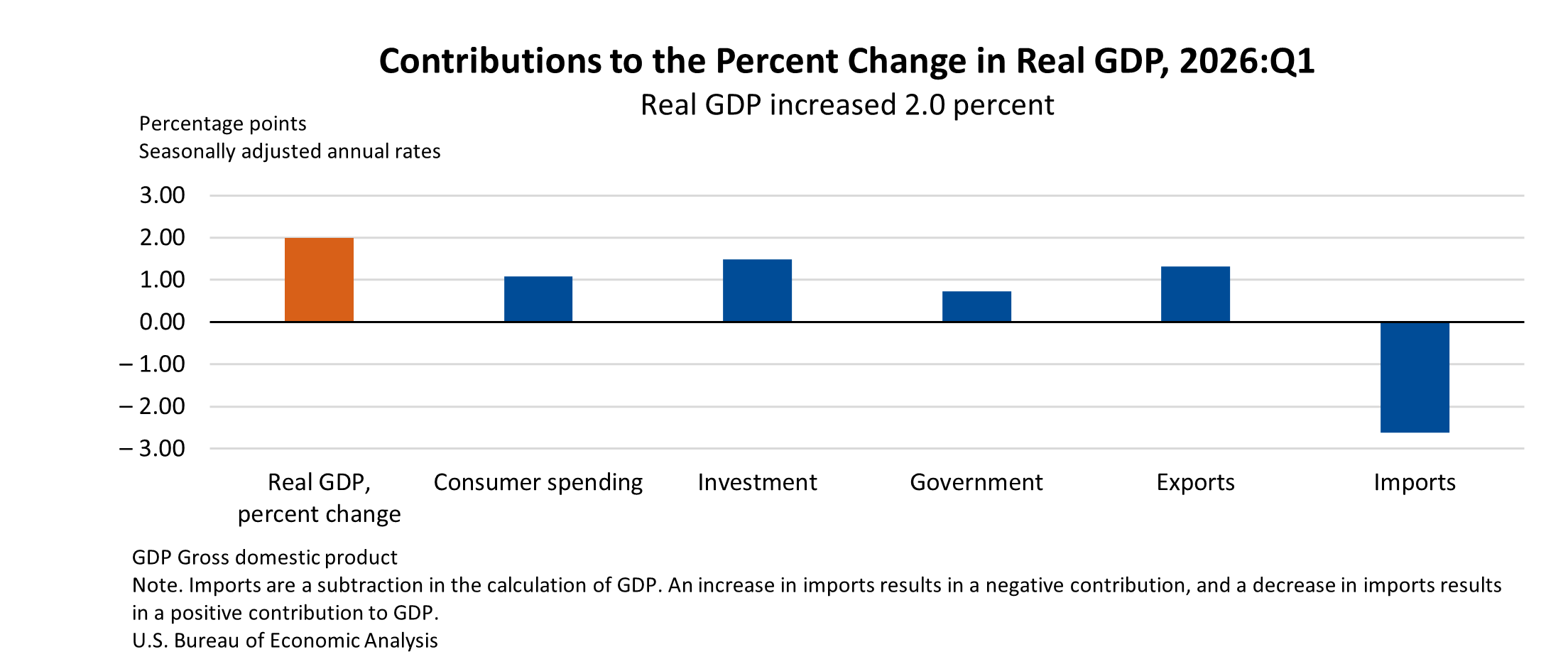

The uptick in economic output was fueled by robust contributions from several key sectors. Investment, exports, consumer spending, and government spending all played a role in propelling GDP growth. Notably, imports, which are subtracted in the calculation of GDP, also saw an increase, indicating a greater volume of goods and services flowing into the domestic economy.

Breaking down the components of the first-quarter performance, the acceleration in real GDP compared to the preceding quarter was primarily due to upturns in government spending and exports. Furthermore, investment experienced a significant acceleration, which, while partially offset by a deceleration in consumer spending, still contributed positively to the overall economic picture. The increase in imports also suggests a demand for foreign goods and services, reflecting various economic activities.

Deeper Dive into Economic Components

Investment: Investment, a crucial component of GDP, showed renewed strength in the first quarter of 2026. This category encompasses business investment in equipment and structures, as well as residential investment. The acceleration in this sector suggests businesses are expanding their capacity and confidence in future economic conditions. Residential investment, while subject to interest rate fluctuations, also contributes to the overall picture of capital formation within the economy. The BEA’s data indicates that this area saw a notable positive shift, signaling a potential expansion in productive assets and housing market activity.

Exports: The global trade landscape also provided a tailwind for U.S. economic growth. An increase in exports means that American-produced goods and services are in higher demand internationally. This can be attributed to a variety of factors, including improved global economic conditions, competitive pricing of U.S. products, or specific trade agreements that may have come into effect. A strong export sector not only boosts GDP but also supports domestic jobs and industries involved in producing goods for foreign markets.

Consumer Spending: Consumer spending, often the largest driver of the U.S. economy, saw a deceleration in its rate of growth during the first quarter, although it remained a positive contributor. This slowdown, juxtaposed with the acceleration in other areas, suggests a potential shift in the composition of economic demand. While the overall increase in consumer spending is a positive indicator, a moderation in its pace warrants attention for future economic assessments. Understanding the underlying reasons for this deceleration, whether it be inflation, changes in consumer confidence, or shifts in spending patterns, will be crucial for forecasting future economic trends.

Government Spending: Government spending, encompassing federal, state, and local government outlays for goods and services, also contributed positively to the first-quarter GDP. This can reflect various initiatives, infrastructure projects, or defense spending. The upturn in this sector indicates a more active role of government in economic activity during this period.

Imports: The increase in imports, while a subtraction from GDP, is not necessarily a negative indicator in isolation. It reflects increased demand for goods and services from abroad, which can be a sign of a healthy domestic economy that has the capacity to absorb more goods. The interplay between imports and exports, as well as domestic production, shapes the overall trade balance and its impact on GDP.

Real Final Sales to Private Domestic Purchasers

A key metric for assessing the underlying strength of domestic demand is real final sales to private domestic purchasers. This measure, which combines consumer spending and gross private fixed investment, increased by a robust 2.5 percent in the first quarter of 2026. This stands in contrast to the 1.8 percent increase seen in the fourth quarter of 2025, indicating a notable strengthening of demand originating from within the private sector of the U.S. economy. This growth suggests that households and businesses are actively engaging in spending and investment, a positive sign for sustained economic expansion.

Inflationary Pressures

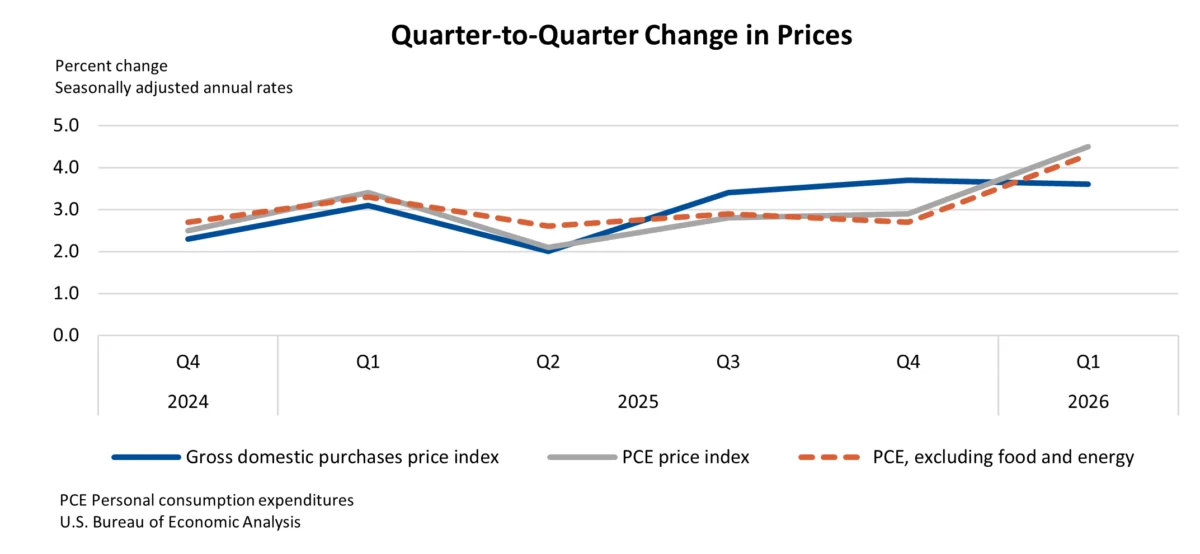

While economic growth picked up, the inflation picture presented a mixed bag. The price index for gross domestic purchases, a broad measure of inflation for goods and services purchased domestically, increased by 3.6 percent in the first quarter. This is a slight moderation from the 3.7 percent increase observed in the fourth quarter of 2025.

However, more specific inflation indicators revealed different trends. The personal consumption expenditures (PCE) price index, a closely watched inflation gauge by the Federal Reserve, saw a more significant increase, rising by 4.5 percent in the first quarter. This is a notable jump from the 2.9 percent increase in the previous quarter. Even when excluding volatile food and energy prices, the core PCE price index accelerated to 4.3 percent in the first quarter, up from 2.7 percent in the fourth quarter. This acceleration in core inflation suggests that price pressures may be becoming more embedded in the broader economy, a development that could influence future monetary policy decisions.

Historical Context and Outlook

The 2.0 percent growth in the first quarter of 2026 represents a significant rebound from the more subdued 0.5 percent growth in the latter half of 2025. This acceleration suggests that the economic headwinds faced in the previous quarter may have begun to dissipate, or that new growth drivers have emerged.

Looking back, the economic landscape of 2025 was characterized by [insert brief, fact-based context about 2025 economic trends, e.g., a period of moderate growth, inflationary concerns, or specific policy impacts]. The shift in momentum observed in the first quarter of 2026 could indicate a transition to a more robust growth phase, or it could be a temporary surge driven by specific quarterly factors.

The BEA’s release of the advance estimate provides an initial snapshot of economic performance. The second estimate, scheduled for May 28, 2026, will incorporate more comprehensive data and may refine these figures. Economists will be closely monitoring subsequent releases to ascertain the sustainability of this growth trajectory and the persistent inflationary trends.

Potential Implications and Expert Analysis

The acceleration in GDP growth is generally viewed as a positive sign for the economy, suggesting increased production of goods and services, potential job creation, and higher incomes. The robust growth in investment and exports points to a diversified economic recovery, rather than reliance on a single sector.

However, the rising core PCE inflation rate warrants careful consideration. Federal Reserve policymakers will be scrutinizing these figures to determine if current monetary policy remains appropriate. A sustained period of elevated inflation, particularly core inflation, could prompt discussions about adjustments to interest rate policy, with potential implications for borrowing costs for consumers and businesses.

"The headline GDP number is encouraging, showing a healthy rebound from the end of last year," commented [Inferred Analyst Name and Title, e.g., Dr. Evelyn Reed, Chief Economist at Global Financial Insights]. "However, the jump in core inflation is a significant factor. The BEA’s data suggests that while demand is strong, the cost of producing goods and services is also rising more rapidly than previously anticipated. The Fed will undoubtedly be paying close attention to whether this trend persists."

The interplay between robust demand and rising costs of production is a delicate balance. If businesses continue to pass on higher costs to consumers, it could lead to a wage-price spiral, further exacerbating inflationary pressures. Conversely, if the current growth in demand allows businesses to absorb some of these costs without significant price hikes, it could lead to a more sustainable economic expansion.

Broader Economic Context

The performance of the U.S. economy in the first quarter of 2026 is occurring within a broader global context. [Insert brief, fact-based context about relevant global economic trends, e.g., global supply chain adjustments, geopolitical events impacting trade, or international monetary policy shifts]. The strength of the U.S. economy can have ripple effects internationally, influencing global trade patterns and investment flows.

Furthermore, domestic policy decisions, such as fiscal stimulus or regulatory changes, can also play a role in shaping economic outcomes. While this report focuses on the BEA’s GDP data, understanding the broader policy environment is essential for a comprehensive economic analysis.

Technical Notes and Data Integrity

The BEA’s methodology for calculating GDP involves a rigorous process of data collection and analysis. The advance estimate released today is based on preliminary data and will be subject to revisions. Key source data and assumptions underpinning this estimate are available, allowing for transparency and further examination by economists and researchers.

Specific adjustments were made to certain source data for this release. For instance, the PCE price index for legal services was adjusted for January and March, reflecting [briefly explain the reason for adjustment based on the provided link, e.g., data anomalies or methodological corrections]. Additionally, refunds related to International Emergency Economic Powers Act (IEEPA) tariffs were treated as a capital transfer and did not impact first-quarter GDP. These adjustments highlight the complexity of national accounts estimation and the BEA’s commitment to data accuracy.

Future Outlook and Next Steps

The BEA will release its second estimate of GDP for the first quarter of 2026 on May 28, 2026, at 8:30 a.m. EDT. This release will also include data on corporate profits. This subsequent release will provide a more refined picture of economic performance and offer further insights into the drivers of growth and inflation.

As the U.S. economy navigates the complexities of growth and inflation, the data released by the BEA remains a critical barometer for policymakers, businesses, and the public. The acceleration in real GDP is a positive development, but the persistent inflationary pressures necessitate continued vigilance and analysis. The coming months will be crucial in determining whether this first-quarter momentum can be sustained and how effectively the nation can manage the delicate balance between economic expansion and price stability.