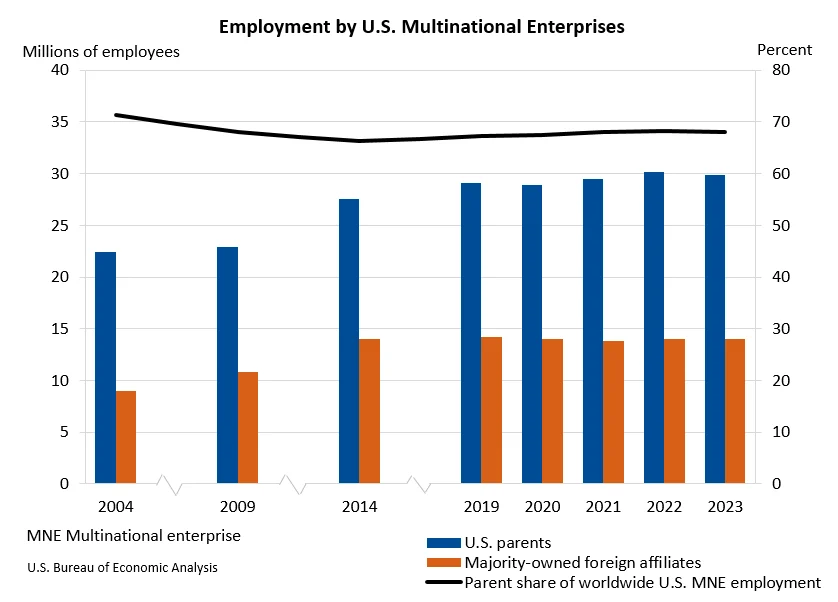

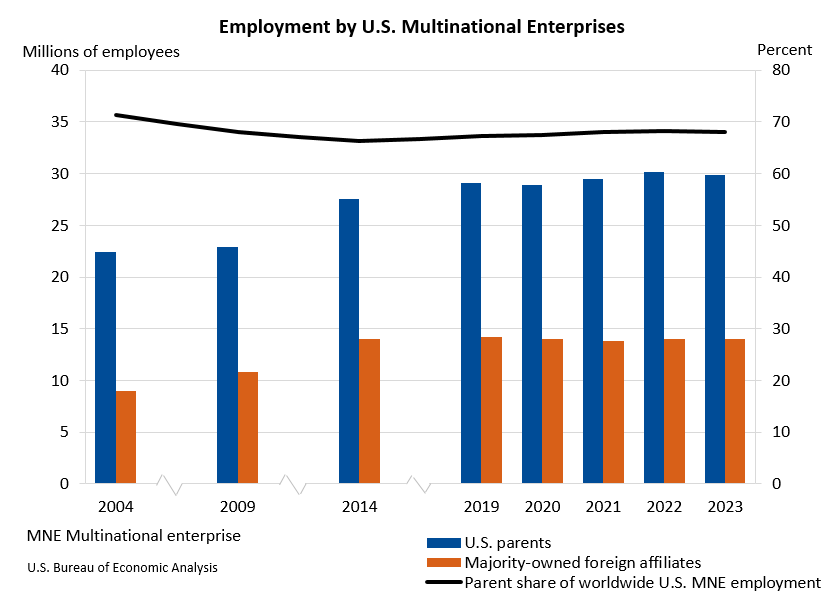

The worldwide employment figures for U.S. multinational enterprises (MNEs) experienced a marginal decrease of 0.4 percent in 2023, settling at 43.9 million workers. This represents a reduction from the revised figure of 44.1 million workers in 2022, according to the latest statistics released by the U.S. Bureau of Economic Analysis (BEA). These preliminary findings offer a snapshot of the operational and financial landscape of American parent companies and their global affiliates.

The data reveals a nuanced picture of U.S. MNE operations, with a slight contraction in overall workforce size contrasting with significant increases in capital expenditures and research and development (R&D) investments. This suggests a strategic recalibration by these global giants, potentially focusing on efficiency and innovation despite a minor dip in direct employment numbers.

U.S. Domestic Employment Trends Mirror Global Shift

Within the United States, employment by U.S. parent companies saw a more pronounced decrease of 0.8 percent, falling to 29.9 million workers in 2023. This domestic decline contributed to a slight reduction in the proportion of U.S. parents’ worldwide employment, which accounted for 68.1 percent of the total in 2023, down from 68.3 percent in the preceding year.

Conversely, employment abroad by majority-owned foreign affiliates of U.S. MNEs exhibited a modest growth of 0.2 percent, reaching 14.0 million workers. This international expansion indicates a growing reliance on overseas labor, with foreign affiliates now comprising 31.9 percent of the total global workforce managed by U.S. MNEs.

The BEA data also highlighted the significant contribution of U.S. parent companies to the domestic private industry employment landscape. In 2023, these companies accounted for 21.9 percent of all private sector jobs in the U.S., a slight decrease from 22.5 percent in 2022. Key sectors for U.S. parent employment included manufacturing, a broad category labeled "other industries" (significantly influenced by transportation and warehousing), and retail trade.

Geographic Distribution of Foreign Affiliate Employment

The global footprint of U.S. MNEs is further illustrated by the geographic distribution of employment within their majority-owned foreign affiliates. The data indicates that India, Mexico, and the United Kingdom were the primary destinations for this overseas employment. This concentration suggests strategic hubs for production, service delivery, or market access in these regions.

Economic Contribution and Investment Trends

Beyond employment, the BEA report sheds light on the economic output and investment activities of U.S. MNEs. The worldwide current-dollar value added by these enterprises, a measure of their direct contribution to economic output, declined by 0.6 percent to $6.9 trillion in 2023.

The contribution of U.S. parents to the national Gross Domestic Product (GDP) also saw a dip, decreasing by 1.0 percent to $5.3 trillion. This resulted in U.S. parents accounting for 21.4 percent of the total U.S. private-industry value added, down from 23.1 percent in 2022. This shift may reflect a broader economic recalibration or a greater emphasis on international market contributions.

In contrast, the value added by majority-owned foreign affiliates experienced a growth of 0.8 percent, reaching $1.6 trillion. The leading contributors to this international value added were affiliates located in the United Kingdom, Canada, and Ireland, underscoring the economic significance of these nations within the U.S. MNE network.

Robust Growth in Capital Expenditures and R&D

A particularly striking trend observed in the 2023 data is the significant increase in expenditures for property, plant, and equipment (capital expenditures) by U.S. MNEs. These worldwide expenditures surged by 7.5 percent, reaching a substantial $1.1 trillion. U.S. parents were the primary drivers of this investment, accounting for $886.1 billion, while majority-owned foreign affiliates contributed $216.2 billion. This robust growth in capital investment suggests a forward-looking strategy, with companies investing in infrastructure and operational capacity.

Simultaneously, worldwide research and development (R&D) expenditures by U.S. MNEs also saw a robust increase of 7.5 percent, totaling $558.3 billion. U.S. parents were the largest investors in R&D, with expenditures amounting to $476.6 billion, while their foreign affiliates invested $81.7 billion. This parallel surge in both capital expenditure and R&D investment points towards a strategic focus on innovation, technological advancement, and future growth initiatives by U.S. multinational corporations.

Context and Background: Understanding MNE Operations

The Bureau of Economic Analysis regularly collects and disseminates data on the activities of U.S. multinational enterprises. This data is crucial for understanding the global economic engagement of American businesses, their impact on international labor markets, and their contributions to both domestic and foreign economies. The statistics cover a wide range of activities, including employment, value added (a measure of economic contribution), sales, financial operations, compensation of employees, and trade in goods and services.

The distinction between "U.S. parents" and "majority-owned foreign affiliates" is fundamental to this reporting. U.S. parents refer to the U.S.-based companies that own and control foreign enterprises. Majority-owned foreign affiliates are foreign business enterprises in which a U.S. parent owns more than 50 percent of the voting stock or an equivalent interest. This ownership structure allows for the tracking of direct U.S. investment and its subsequent economic impact abroad.

Timeline and Revisions of Data

The statistics released for 2023 are preliminary, meaning they are based on initial data and are subject to revision as more comprehensive information becomes available. The BEA typically releases preliminary data for a given year and then revises it in subsequent releases. This iterative process ensures the accuracy and reliability of the reported figures.

For instance, the BEA also provided updated statistics for 2022, which were revised to incorporate newly available and revised source data. These revisions are essential for understanding trends over time and for making informed economic analyses. The table provided in the original release detailing these revisions offers a clear comparison of preliminary versus revised estimates for key metrics such as the number of employees, value added, and expenditures for property, plant, and equipment, and R&D. For example, the revised 2022 employment figure for U.S. parents was 30,120.1 thousand, slightly down from the preliminary estimate of 30,240.8 thousand. Similarly, value added by U.S. parents was revised to $5,321.2 billion from a preliminary $5,308.0 billion. These adjustments, while often minor, underscore the dynamic nature of economic data collection.

Broader Impact and Implications

The slight decline in global employment by U.S. MNEs, coupled with a significant increase in capital and R&D expenditures, suggests a potential shift in operational strategies. Companies may be prioritizing technological advancements and efficiency gains over direct workforce expansion, or they might be redeploying resources towards automation and other productivity-enhancing measures. This trend could have implications for labor markets globally, particularly in regions heavily reliant on manufacturing or service jobs that are susceptible to automation or outsourcing.

The robust growth in capital expenditures signals confidence in future economic conditions and a commitment to expanding operational capacity. This investment could translate into future job creation, albeit potentially in different sectors or with different skill requirements than currently prevalent. The parallel surge in R&D spending is a clear indicator of a focus on innovation, which is crucial for maintaining competitiveness in the global marketplace. Companies are likely investing in new technologies, products, and processes to drive future growth and profitability.

The differing trends in domestic versus international employment also warrant attention. While U.S. parent employment decreased, foreign affiliate employment saw a modest rise. This could reflect a variety of factors, including evolving global supply chains, differing labor costs and regulations, and strategic decisions to localize production or services in key international markets. The BEA’s detailed breakdowns by industry and country will be essential for a more granular understanding of these shifts.

Official Responses and Data Availability

The U.S. Bureau of Economic Analysis, as the primary source of this data, plays a critical role in providing policymakers, businesses, and researchers with essential economic intelligence. The agency emphasizes the availability of comprehensive data tables on its website, allowing for in-depth analysis of various facets of U.S. MNE activities. These tables offer detailed breakdowns by industry for U.S. parents and by both industry and country for foreign affiliates, providing a rich resource for economic research.

BEA also notes that certain data tables previously included in news releases have been discontinued as of August 22, 2025. This includes statistics on foreign affiliates with 50 percent or less U.S. ownership and supplemental industry statistics. While these have been archived, the core data on majority-owned affiliates and U.S. parents remains accessible through BEA’s Interactive Data Application and comprehensive data tables. The next release of statistics on the activities of U.S. Multinational Enterprises, covering 2024 data, is anticipated in November 2026.

In conclusion, the 2023 data from the BEA presents a complex picture of U.S. multinational enterprises. While overall global employment saw a marginal dip, the significant increases in capital investment and R&D spending highlight a strong emphasis on innovation and future growth. The diverging trends between domestic and international employment, along with the sectoral and geographic distribution of these activities, provide valuable insights into the evolving strategies and global footprint of American corporations in an increasingly interconnected world.