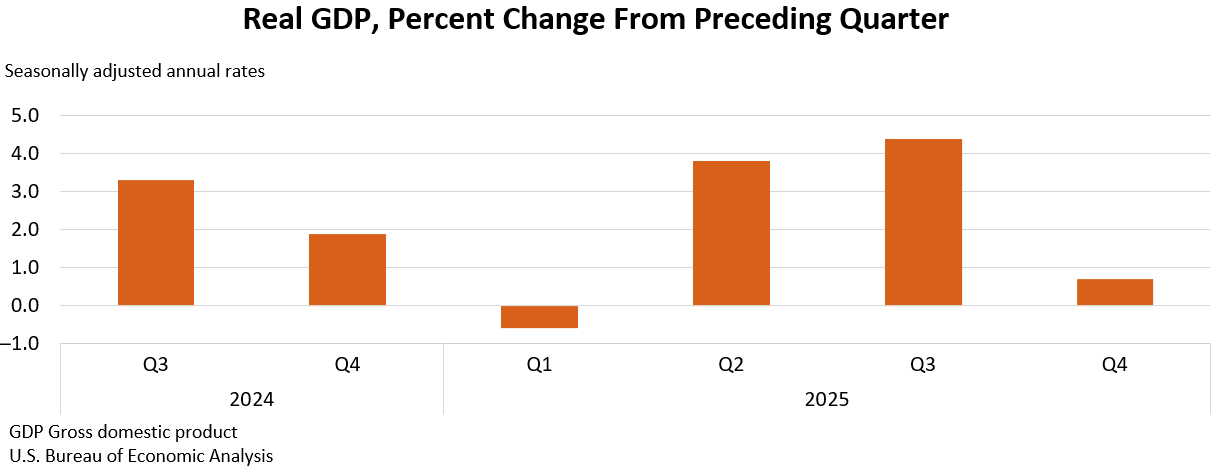

The U.S. economy experienced a significant slowdown in the fourth quarter of 2025, with real gross domestic product (GDP) expanding at an annualized rate of just 0.7 percent. This revised figure, released by the U.S. Bureau of Economic Analysis (BEA), represents a substantial deceleration from the robust 4.4 percent growth recorded in the third quarter. The report’s release itself was delayed, originally slated for February 26, 2026, but rescheduled due to the disruptive October-November 2025 government shutdown.

The downward revision from the advance estimate, which had projected a 1.4 percent growth rate, underscores the economic headwinds encountered in the final months of 2025. This recalibration reflects updated data indicating weaker performance in key economic drivers, including consumer spending, government expenditures, and investment. While imports decreased less than initially anticipated, this did little to offset the broader contractionary forces.

Key Drivers of the Q4 Slowdown

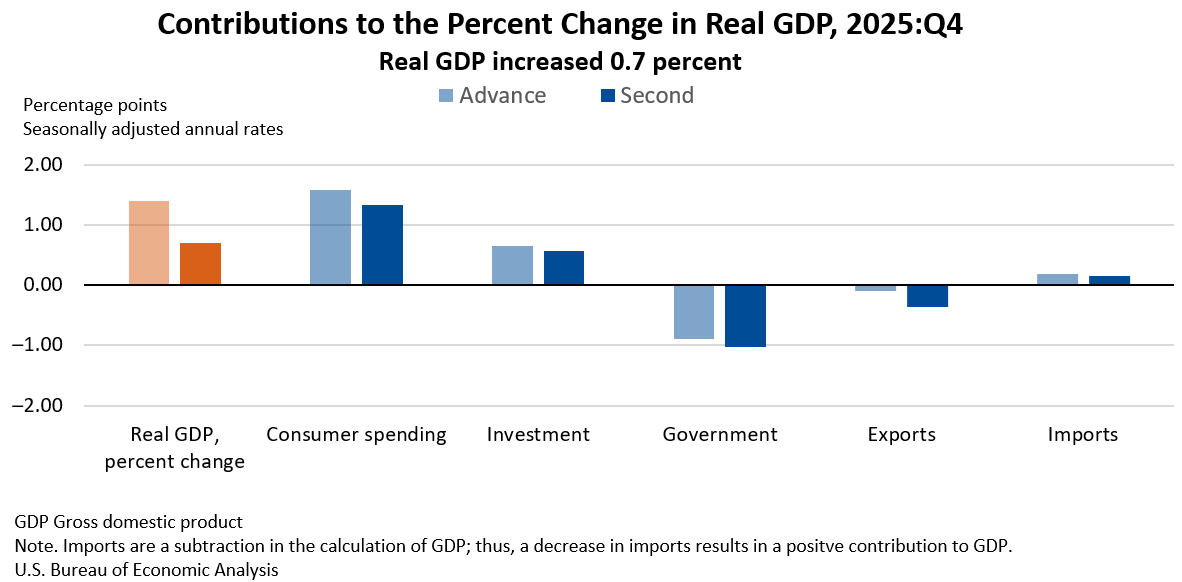

Analysis of the BEA’s second estimate reveals a complex interplay of factors contributing to the tempered growth. Increases in consumer spending and investment, which are typically engines of economic expansion, were present but insufficient to counter significant declines in government spending and exports. Consumer spending, a cornerstone of the U.S. economy, was revised downward, indicating a less robust purchasing appetite than previously assessed. Similarly, government outlays contracted, a stark contrast to the stimulus measures often seen during periods of economic uncertainty. Exports also experienced a decline, suggesting a weakening global demand or increased competitiveness challenges for American goods and services abroad.

The BEA’s data highlights that real final sales to private domestic purchasers—a measure encompassing consumer spending and gross private fixed investment—grew by 1.9 percent in the fourth quarter. This figure was also revised downward by 0.5 percentage points from the advance estimate, reinforcing the narrative of a more subdued domestic demand environment.

Inflationary Pressures Persist

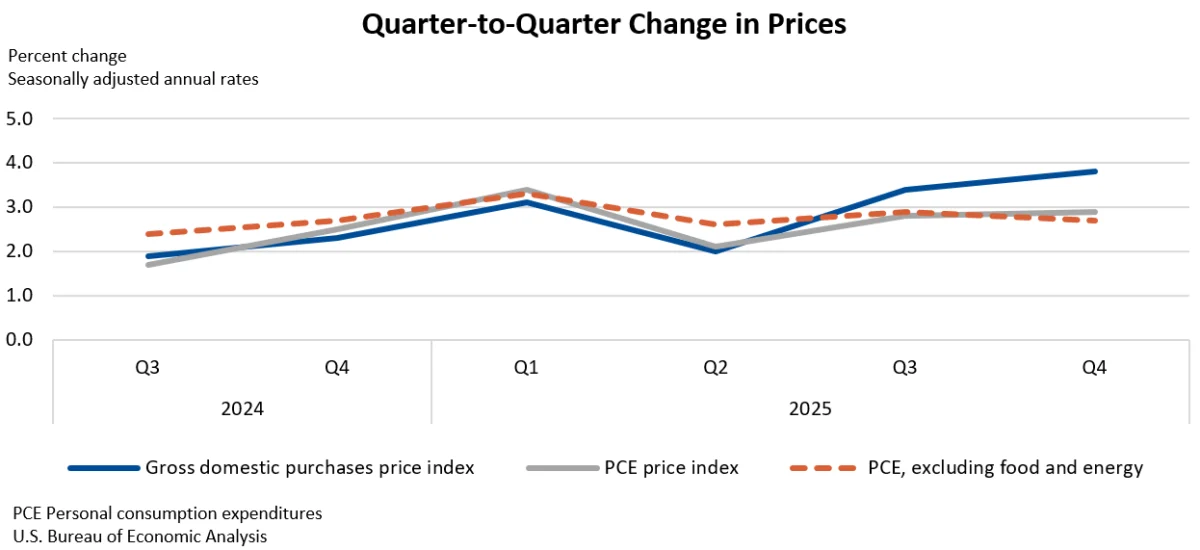

Despite the cooling GDP growth, inflationary pressures remained a concern. The price index for gross domestic purchases, a broad measure of inflation for goods and services bought by consumers, businesses, and government, rose by 3.8 percent in the fourth quarter. This represents a slight upward revision of 0.1 percentage point from the initial estimate. The personal consumption expenditures (PCE) price index, the Federal Reserve’s preferred inflation gauge, held steady at a 2.9 percent increase. Crucially, the core PCE price index, which excludes volatile food and energy prices, also remained unchanged at 2.7 percent, indicating persistent underlying inflationary trends.

The Shadow of the Government Shutdown

The October-November 2025 federal government shutdown cast a significant shadow over the economic data for the fourth quarter. The prolonged lapse in appropriations led to the closure of numerous federal agencies and the furloughing of many employees. While the full economic ramifications are difficult to precisely quantify, the BEA estimates that the reduction in labor services provided by federal employees subtracted approximately 1.0 percentage point from real GDP growth during the quarter. This disruption not only impacted government operations but also created uncertainty that likely permeated business and consumer confidence.

The BEA has detailed its methodology for accounting for the shutdown’s effects. To address the absence of October 2025 consumer price index (CPI) data, the Bureau of Labor Statistics (BLS) was unable to collect this crucial information. In response, the BEA derived seasonally adjusted price indexes for October by utilizing the geometric mean of the September and November CPIs. Non-seasonally adjusted price indexes were then created by applying the seasonal adjustment factors from October 2024 to these imputed October 2025 values. This imputation process, while necessary, introduces a degree of approximation into the inflation data.

Furthermore, the shutdown’s impact on federal compensation was managed through back pay for furloughed employees. This ensured that the shutdown had no direct impact on current-dollar federal compensation. However, it resulted in a temporary increase in the prices paid for federal employee compensation, a nuance reflected in the inflationary data. The BEA has provided further clarification on how such events are integrated into their GDP estimation methodologies via an FAQ on their website.

A Look at the Full Year 2025

For the entirety of 2025, real GDP growth was revised downward to 2.1 percent when comparing the annual level of 2025 to that of 2024. This represents a 0.1 percentage point decrease from the previous annual estimate. The primary drivers of this full-year growth were sustained increases in consumer spending and investment.

Inflation for the full year also remained consistent with previous estimates. The price index for gross domestic purchases increased by 2.6 percent, mirroring the earlier projection. Similarly, the PCE price index also saw a 2.6 percent increase, and the core PCE price index (excluding food and energy) rose by 2.8 percent, indicating a year of relatively stable, albeit elevated, price pressures.

Chronology of Key Events

The economic narrative of the fourth quarter of 2025 is intrinsically linked to the disruption caused by the federal government shutdown. The period from October 1 to November 12, 2025, marked the duration of the shutdown, a significant interruption that directly impacted government operations and created widespread economic uncertainty. This disruption led to the delayed release of the BEA’s second estimate for Q4 GDP, which was originally scheduled for February 26, 2026, but was rescheduled to a later date. The BEA’s release of the second estimate, incorporating the latest data and revised calculations, occurred on March 27, 2026 (as indicated by the original article’s context of a "today" release). The subsequent release, the third estimate for the fourth quarter of 2025, along with GDP by Industry and Corporate Profits for the full year, is slated for April 9, 2026.

Broader Economic Implications and Expert Reactions

The revised GDP figures paint a picture of an economy grappling with a confluence of challenges. The slowdown in growth, coupled with persistent inflation, presents a complex environment for policymakers. While the BEA’s report provides a factual account of economic activity, economists and market analysts are likely to interpret these figures with a focus on future economic trajectory.

"The downward revision to Q4 GDP growth is a clear signal that the economy is losing momentum," commented Dr. Eleanor Vance, a senior economist at the Sterling Institute. "The impact of the government shutdown, while difficult to isolate entirely, undoubtedly contributed to this deceleration by disrupting economic activity and injecting uncertainty. The fact that consumer spending and investment were also revised lower is particularly concerning, as these are typically the most resilient components of GDP."

The persistent core inflation also remains a significant concern. "While headline inflation might fluctuate, the stickiness of core inflation suggests that underlying price pressures are still present," Dr. Vance added. "This complicates the Federal Reserve’s task, as they must balance the need to curb inflation with the risk of exacerbating an economic slowdown."

The decline in exports also warrants attention. In a globalized economy, weakening international demand or a loss of competitiveness can have cascading effects. "We need to monitor the trade balance closely," noted financial analyst Mark Jenkins of Global Financial Insights. "A sustained drop in exports could signal broader issues with global economic health or challenges within specific U.S. industries. This could also put further pressure on domestic producers."

BEA’s Modernization Efforts

In parallel with the economic data release, the BEA announced significant improvements to its news release packages. These changes are part of the agency’s ongoing modernization efforts aimed at streamlining and enhancing the accessibility of economic data. Notably, news release tables in PDF and Excel formats will be discontinued beginning with the third estimate for the fourth quarter of 2025, scheduled for April 9, 2026. This transition will direct users to BEA’s online Interactive Data Tables, which are intended to provide more comprehensive and up-to-date information, reducing redundancy and improving efficiency. This move reflects a broader trend towards digital-first data dissemination and aims to provide users with direct access to the most current and detailed economic statistics.

The next release from the BEA, scheduled for April 9, 2026, will provide the third estimate for Q4 2025 GDP, along with GDP by Industry and Corporate Profits for the full year 2025. This upcoming release will supersede the data presented in the current report, with earlier data archived for historical reference.

The revised economic picture for the fourth quarter of 2025 underscores a period of considerable economic flux, shaped by both underlying domestic trends and significant exogenous shocks like the federal government shutdown. The coming months will be critical in determining whether the U.S. economy can regain its footing and navigate the persistent inflationary environment without succumbing to a more pronounced downturn.