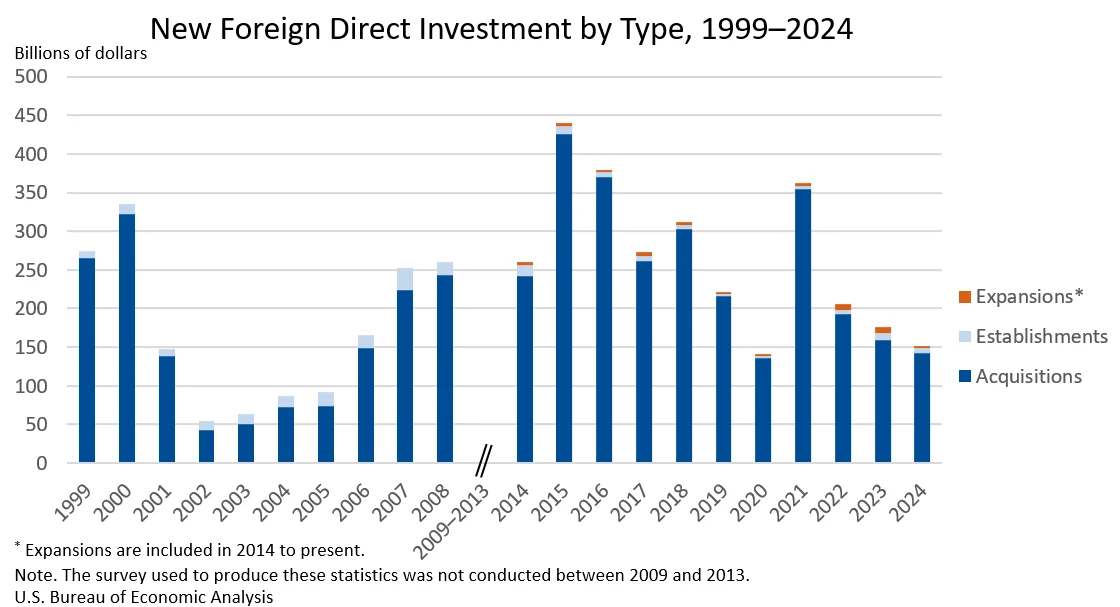

Expenditures by foreign direct investors to acquire, establish, or expand U.S. businesses totaled $151.0 billion in 2024, a notable decrease from the previous year, according to preliminary statistics released by the U.S. Bureau of Economic Analysis (BEA). This figure represents a $24.9 billion, or 14.2 percent, drop from the revised $176.0 billion recorded in 2023. The 2024 total also falls significantly below the annual average of $277.2 billion observed between 2014 and 2023, indicating a recalibration in international investment flows into the United States. As has been the trend in prior years, the acquisition of existing U.S. businesses constituted the predominant form of investment activity.

Key Investment Trends and Figures for 2024

The breakdown of foreign direct investment (FDI) expenditures in 2024 reveals that acquisitions of established U.S. companies accounted for the lion’s share, totaling $143.0 billion. Establishing new U.S. businesses attracted $6.3 billion, while expansions of existing foreign-owned businesses drew $1.8 billion. These figures represent the initial year’s investment. When considering planned future expenditures, the total anticipated investment for 2024 rose to $157.0 billion, suggesting that while the initial outlay was lower, a significant portion of these investments are expected to grow over time.

This investment activity directly impacted employment, with newly acquired, established, or expanded foreign-owned businesses in the United States providing jobs for an estimated 204,200 employees in 2024. This figure underscores the tangible economic contribution of FDI to the U.S. labor market.

Sectoral Distribution of Investment

The manufacturing sector emerged as the leading recipient of FDI in 2024, attracting $67.7 billion, which represented a substantial 44.9 percent of all expenditures. Within manufacturing, the chemical manufacturing subsector saw particularly strong investment, with $23.7 billion. Other significant sectors drawing foreign capital included finance and insurance ($23.2 billion) and utilities ($16.0 billion). These figures highlight the continued attractiveness of U.S. industrial and financial assets to international investors.

Geographic Origins of Investment

Examining the source of these investments, Ireland emerged as the top investing country in 2024, contributing $30.1 billion. Canada followed closely with $23.9 billion in expenditures. Regionally, Europe was the most significant source of new FDI, accounting for $96.7 billion, or a commanding 64.0 percent of the total. The Asia and Pacific region was the second-largest investing bloc, with expenditures totaling $23.2 billion. This dominance of European investment suggests strong transatlantic economic ties and a continued confidence in the U.S. market from European entities.

State-Level Investment Hotspots

At the state level, Texas attracted the largest share of FDI in 2024, with investment expenditures amounting to $22.8 billion. Georgia also saw significant inflows, receiving $16.3 billion, and California attracted $12.9 billion. These states, known for their diverse economies and business-friendly environments, continue to be prime destinations for foreign direct investment.

Greenfield Investments: Building the Future

Greenfield investments, which involve establishing new businesses or expanding existing foreign-owned ones, totaled $8.1 billion in 2024. This category of investment is crucial for job creation and the development of new industries. The professional, scientific, and technical services sector led greenfield expenditures with $2.8 billion, driven particularly by management, scientific, and technical consulting services, which accounted for $1.6 billion.

By region, Europe again demonstrated strong engagement in greenfield projects, contributing $3.8 billion. Latin America and the Other Western Hemisphere followed with $1.4 billion, and Asia and the Pacific contributed $1.2 billion. At the state level, Wyoming received the highest greenfield investment at $2.0 billion, followed by New Mexico with $1.4 billion. Planned total expenditures for greenfield investment initiated in 2024, encompassing both initial and future outlays, reached $14.1 billion, indicating a commitment to long-term growth in these new ventures.

Employment Dynamics in Foreign-Owned Enterprises

The employment landscape within foreign-owned businesses in the U.S. saw varied trends. In 2024, the current employment in acquired enterprises stood at 203,600. When factoring in planned employment for newly established businesses and expansions, the total projected employment reached 213,200.

The manufacturing sector continued to be a significant employer of individuals working in foreign-owned entities, accounting for 73,600 current employees. By country of origin, Ireland and Canada were responsible for the largest numbers of current employees, with 43,100 and 37,500 respectively. Florida led U.S. states in current employment resulting from new FDI, with 32,700 jobs, followed by Texas (18,200) and New York (14,200).

Revisions to 2023 Data Highlight Evolving Economic Picture

The BEA’s release also included significant revisions to the 2023 FDI data. Previously published first-year expenditures for 2023 were $148.8 billion, but the revised figure now stands at $176.0 billion. This upward revision of $27.2 billion, or 18.3 percent, reflects a more robust FDI picture for the previous year than initially reported. The revisions impacted all categories of investment: U.S. businesses acquired saw an increase from $136.5 billion to $158.7 billion; newly established businesses rose from $7.4 billion to $9.0 billion; and expanded businesses increased from $5.0 billion to $8.3 billion.

Similarly, planned total expenditures for 2023 were substantially revised upwards from $175.9 billion to $218.8 billion. This indicates that the initial estimates may not have fully captured the long-term commitments and future investment plans of foreign investors. These revisions underscore the dynamic nature of economic data and the importance of updated statistics for accurate analysis.

Context and Analysis: A Shifting Global Investment Climate

The decline in FDI expenditures in 2024, when viewed against the backdrop of global economic uncertainties, can be attributed to a confluence of factors. Persistent inflation, rising interest rates in key economies, geopolitical tensions, and ongoing supply chain adjustments have collectively created a more cautious investment environment worldwide. While the U.S. remains a highly attractive destination for foreign capital due to its large market, technological innovation, and stable legal framework, these global headwinds appear to have tempered the pace of new investment.

The BEA’s data on planned total expenditures, however, offers a more optimistic outlook. The fact that planned expenditures exceed initial first-year outlays suggests that investors, while perhaps adopting a more measured approach in the short term, remain committed to expanding their presence and operations in the United States. The substantial revisions to 2023 data also indicate that initial reporting may sometimes underestimate the full scope of investment activity.

The continued dominance of acquisitions over the establishment of new businesses is a long-standing trend. This suggests that foreign investors often prefer to leverage existing infrastructure, market share, and operational expertise of established U.S. companies rather than undertaking the potentially higher risks and longer gestation periods associated with greenfield projects. However, the consistent investment in greenfield projects, particularly in sectors like professional services, signals a commitment to fostering innovation and long-term growth within the U.S. economy.

The concentration of investment in manufacturing, finance, and utilities points to the enduring appeal of these foundational sectors for foreign capital. These industries are critical to economic infrastructure and growth, and foreign investment can bring not only capital but also technological advancements and global best practices.

The strong showing from European investors highlights the deep integration of transatlantic economies. The U.S. continues to be a preferred investment destination for European companies seeking access to its vast consumer market and technological ecosystem. The significant contribution from Ireland, in particular, reflects its role as a strategic hub for many multinational corporations.

Broader Implications for the U.S. Economy

The trends observed in the 2024 FDI data have several implications for the U.S. economy. A slowdown in FDI could potentially impact job creation, capital formation, and technological diffusion, particularly if the trend persists. However, the overall level of investment remains substantial, and the U.S. economy’s inherent strengths continue to attract significant foreign capital.

The BEA’s detailed data, broken down by industry, country, and state, provides crucial insights for policymakers, businesses, and economic development agencies. Understanding where and how foreign investment is flowing allows for more targeted strategies to attract and retain capital, foster innovation, and create high-quality jobs. For states like Texas, Georgia, and California, which consistently attract significant FDI, this data reinforces the importance of maintaining competitive business environments.

The emphasis on acquisitions underscores the need for policies that support both domestic business growth and the smooth integration of foreign-owned enterprises. While acquisitions can bring immediate economic benefits, fostering an environment that also encourages the creation of new businesses is crucial for long-term economic dynamism and diversification.

The BEA’s ongoing commitment to refining its data collection and reporting, as evidenced by the revisions to the 2023 figures, is vital for providing an accurate and up-to-date picture of the U.S. economy. As global economic conditions continue to evolve, consistent and reliable data on foreign direct investment will be indispensable for navigating future economic challenges and opportunities.

Future Outlook and Data Availability

The BEA will release its next update on new foreign direct investment in the United States in July 2026, which will supersede the 2024 preliminary statistics with more comprehensive data. The agency provides extensive data tables through its Interactive Data Application and Supplemental Data Tables, allowing for in-depth analysis of FDI trends across various dimensions. Discontinued tables, such as those on sales, net income, and balance sheets of new affiliates, have been archived, reflecting the evolving needs and methodologies in economic data reporting. These archived datasets remain valuable resources for historical research and trend analysis.

The data on planned total expenditures for both overall FDI and greenfield investments offer a forward-looking perspective, suggesting that while the pace of new investment may have slowed in 2024, the underlying appetite for engaging with the U.S. market remains robust, albeit with a potentially more cautious and strategic approach.